Question: Carry trade: Country A interest rate =2% Country B interest rate Chris manages a hedge fund doing a carry trade. He will long currency

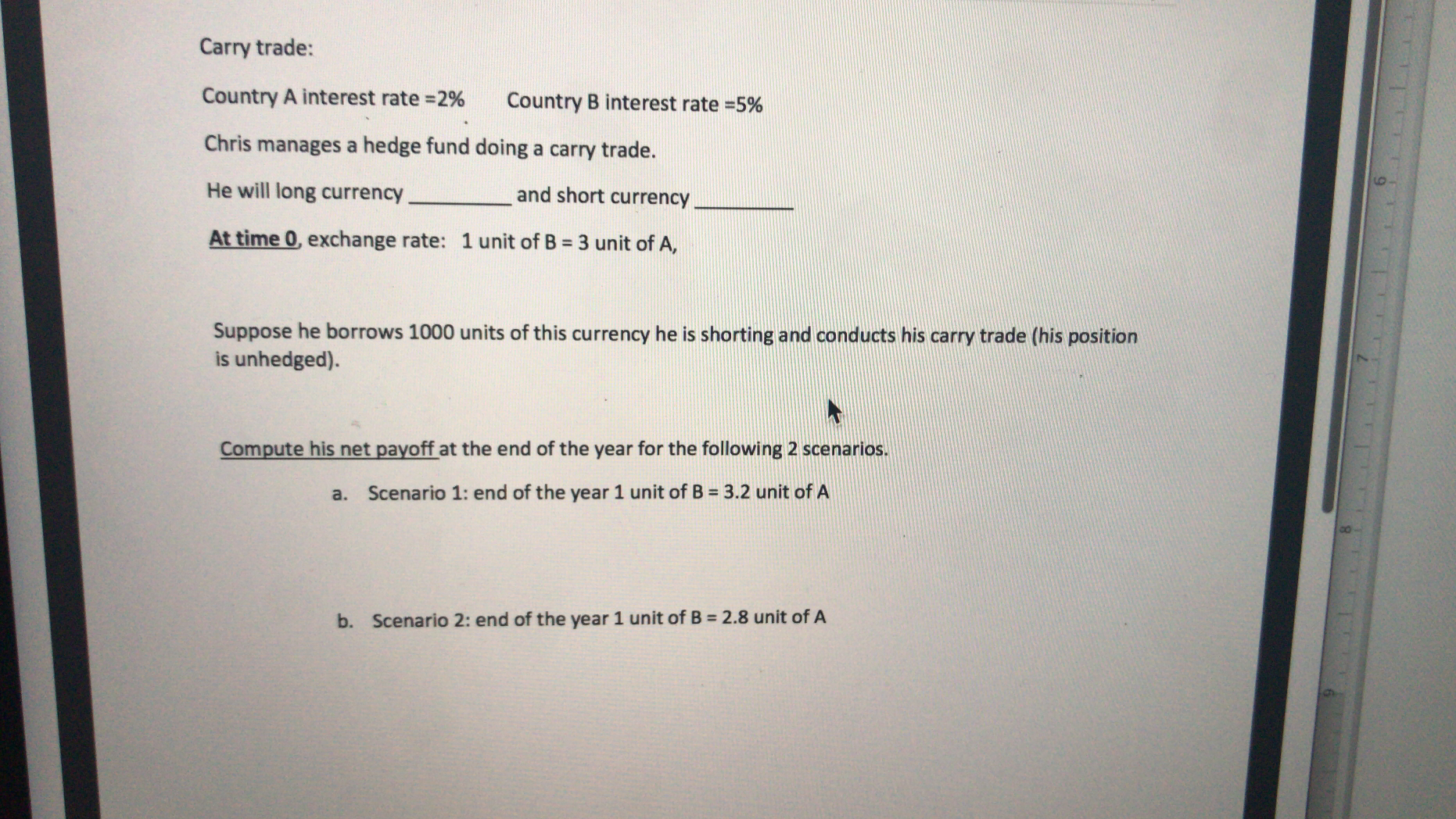

Carry trade: Country A interest rate =2% Country B interest rate Chris manages a hedge fund doing a carry trade. He will long currency and short currency At time Q, exchange rate: 1 unit of B = 3 unit of A, Suppose he borrows 1000 units of this currency he is shorting and conducts his carry trade (his position is unhedged). Compute his net payoff at the end of the year for the following 2 scenarios. a. b. Scenario 1: end of the year 1 unit of B = 3.2 unit of A Scenario 2: end of the year 1 unit of B = 2.8 unit of A

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock