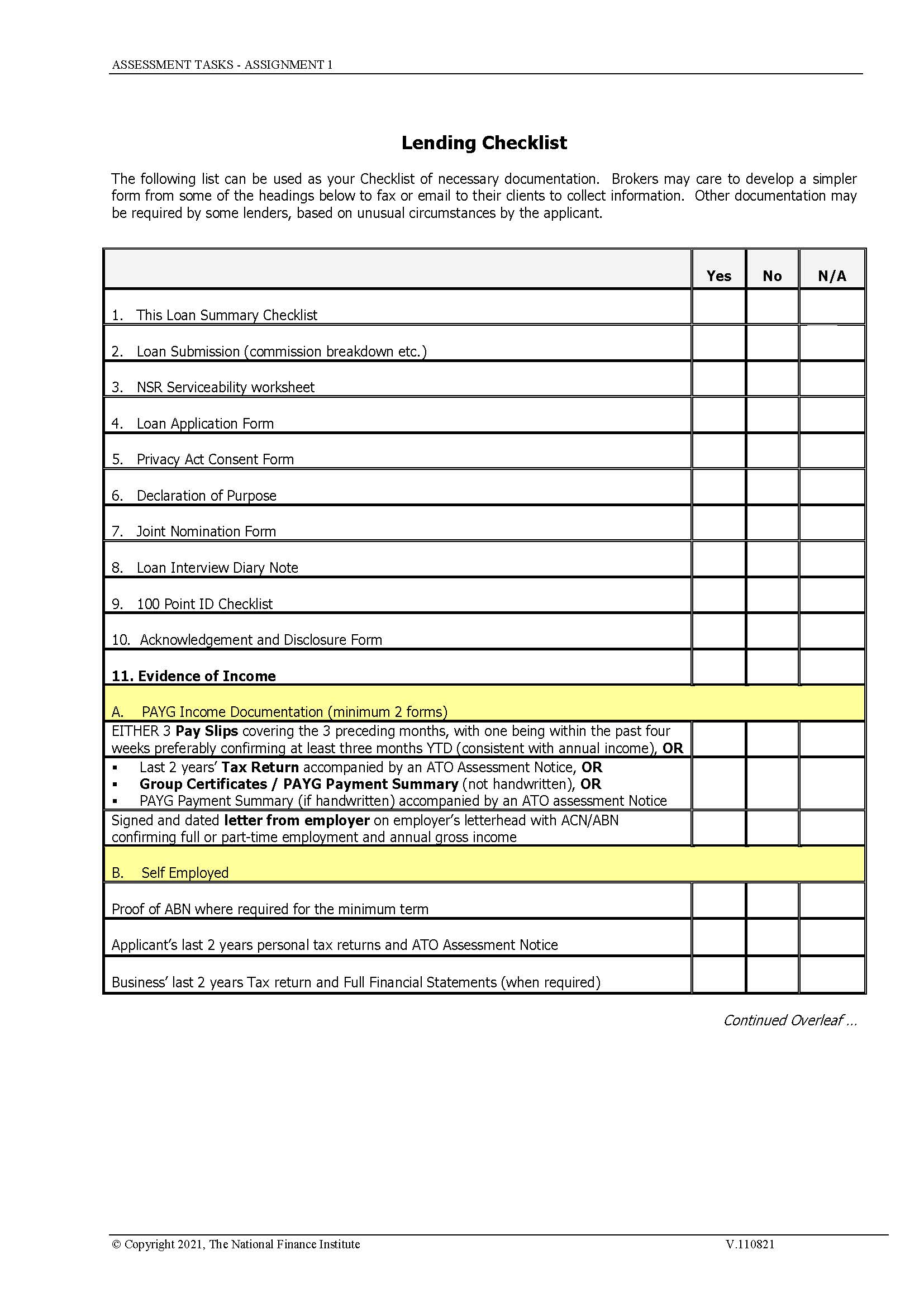

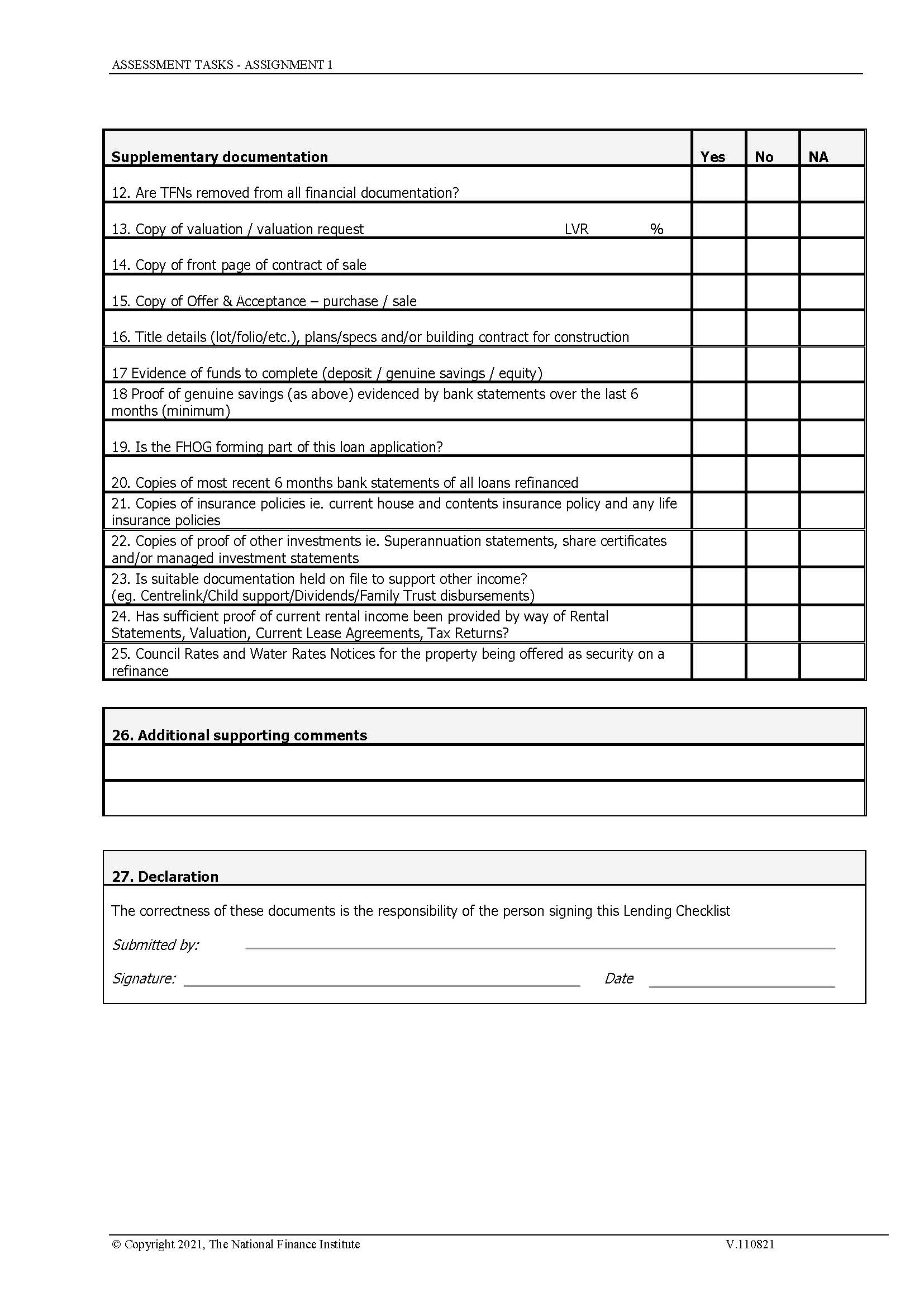

Question: Fact Find Initial Interview: Time Date Location Referred by: A. Personal Details Applicant 1 Applicant 2 Full Name of Applicant Full Name of Applicant Mr

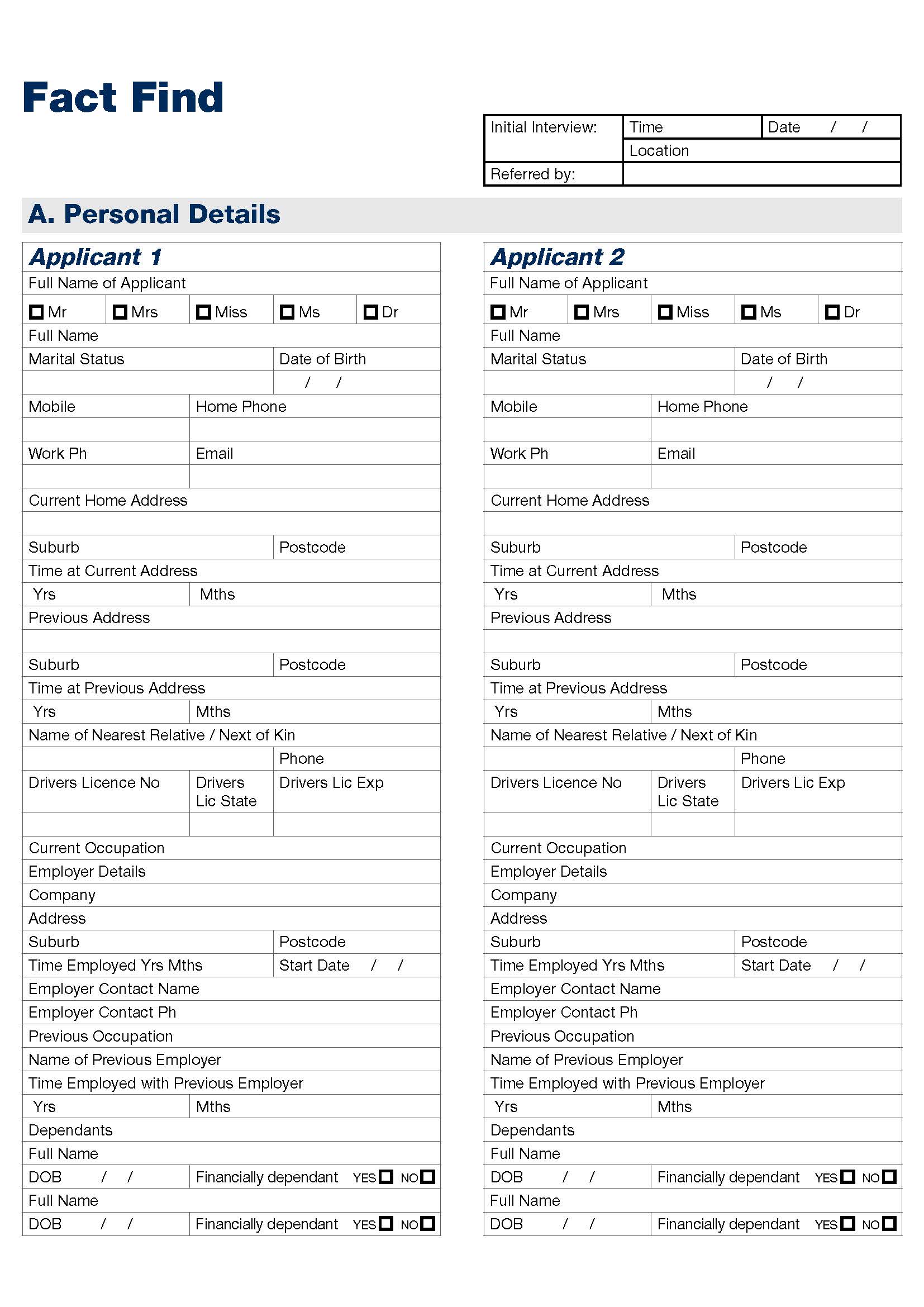

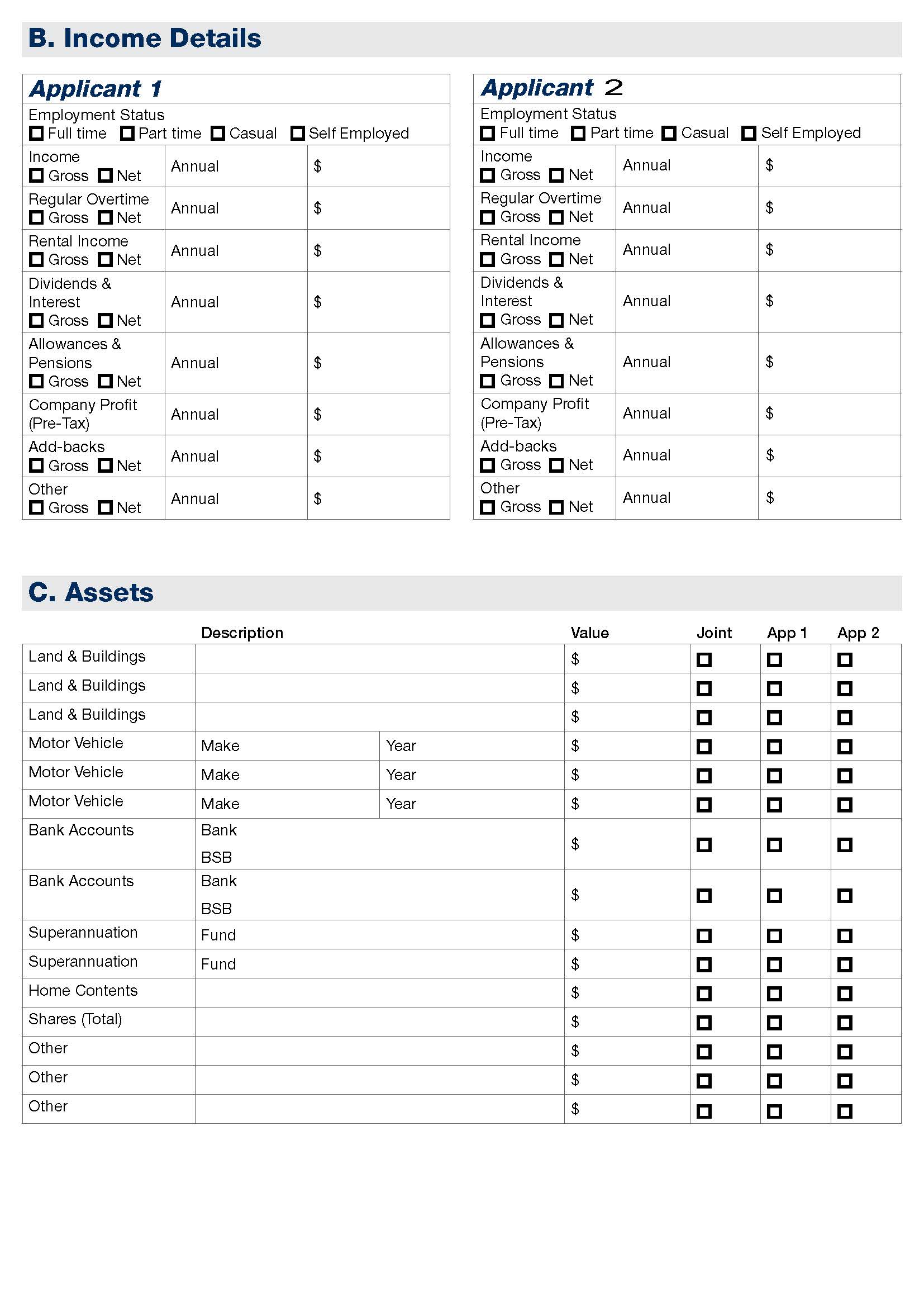

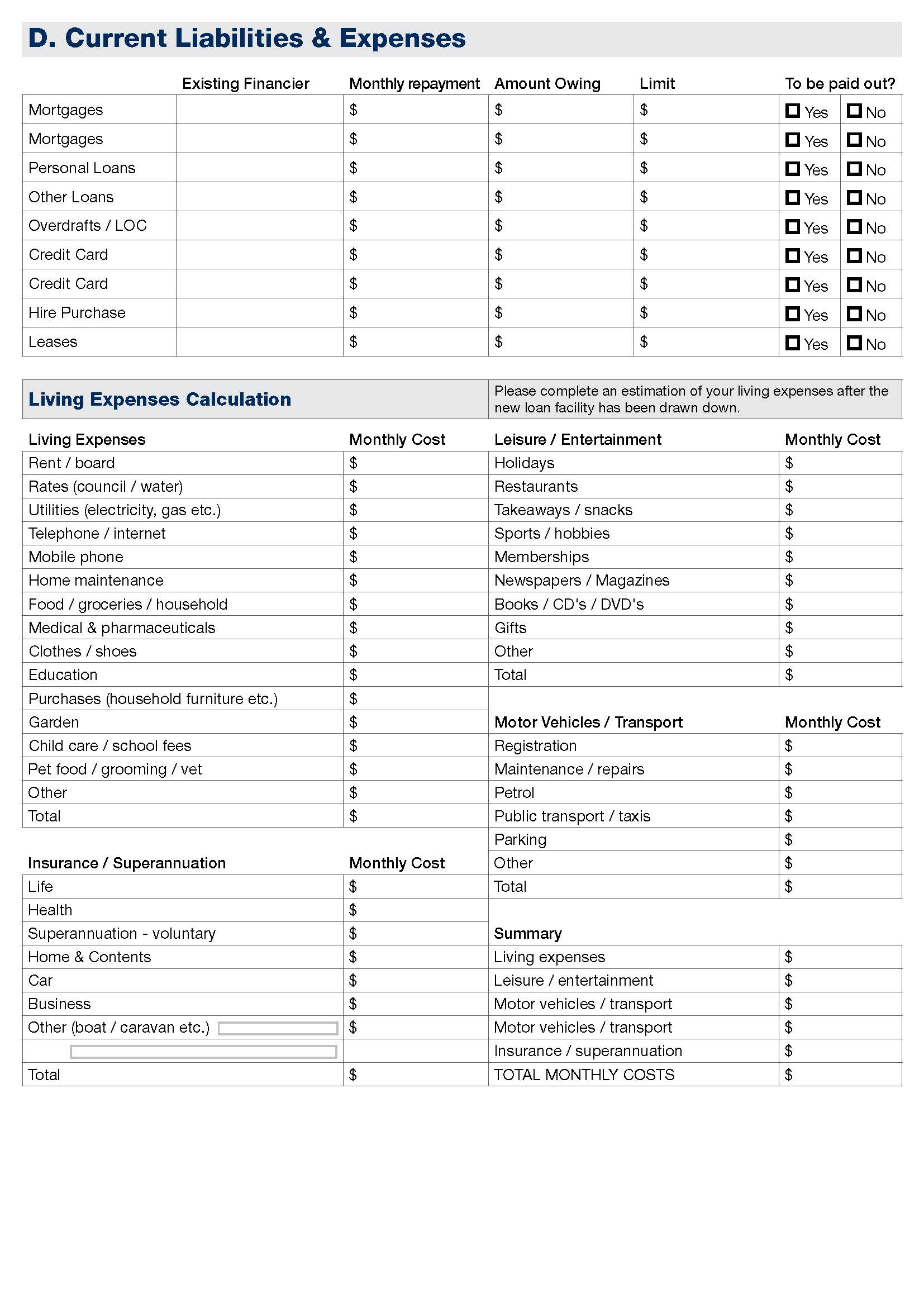

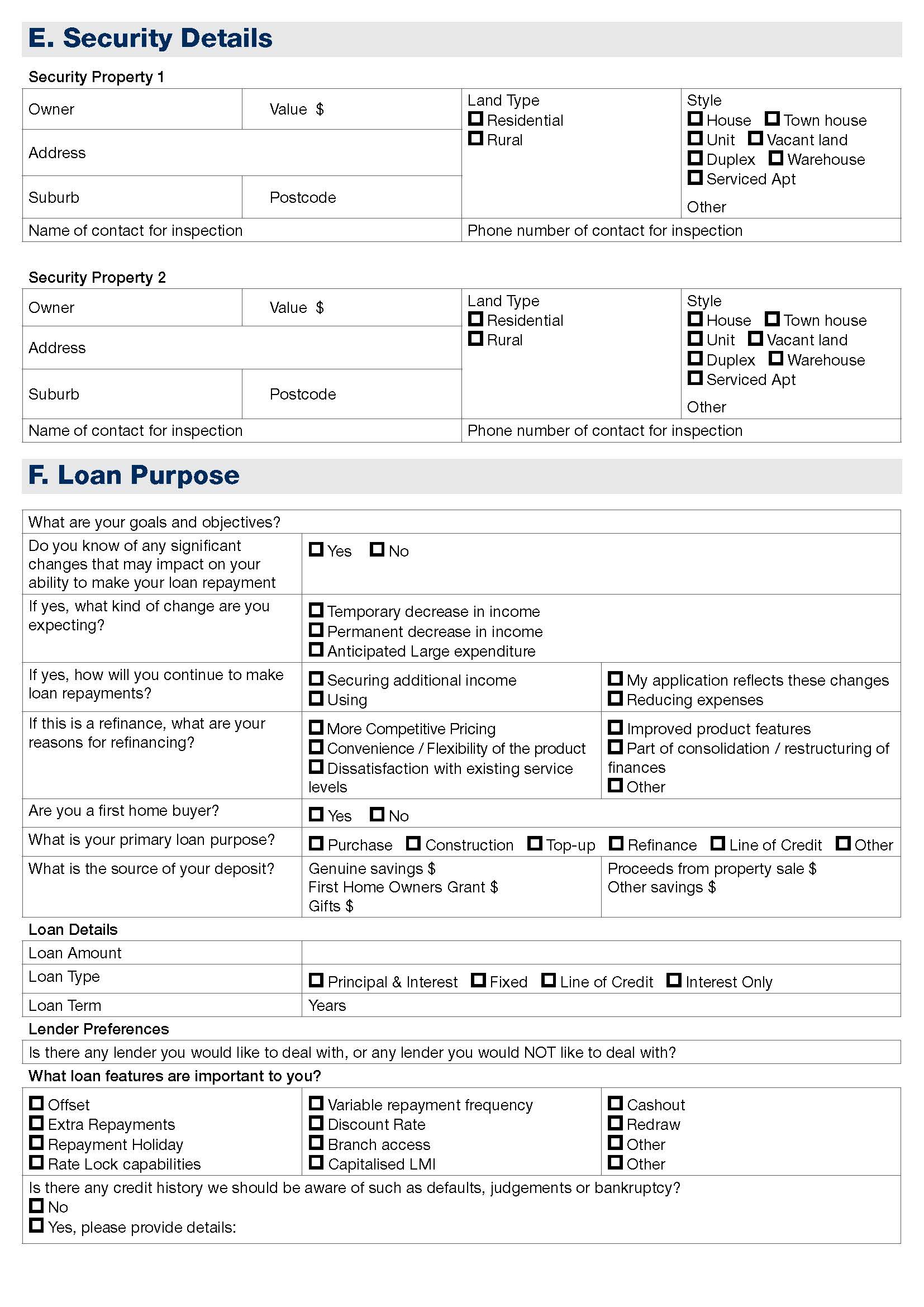

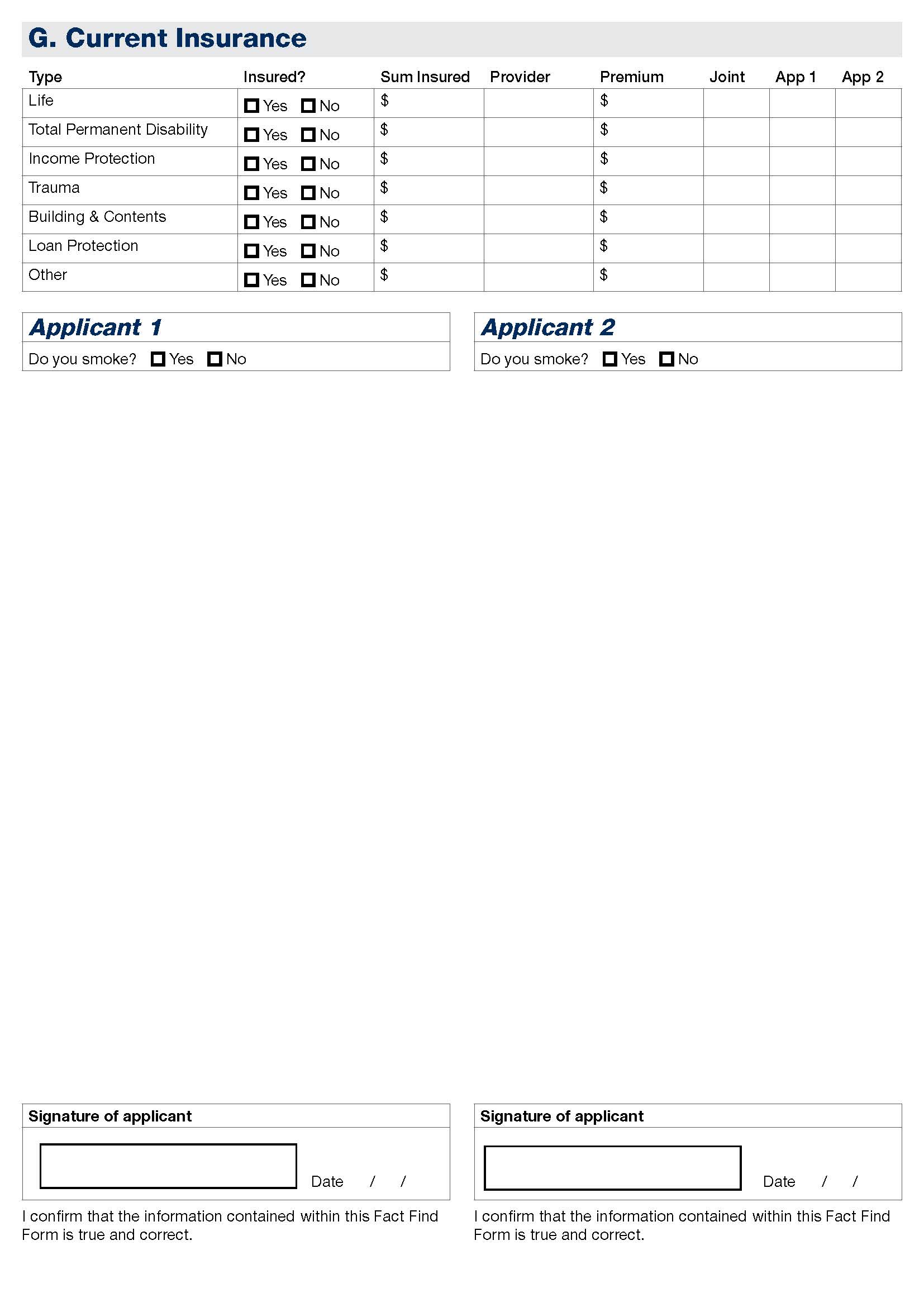

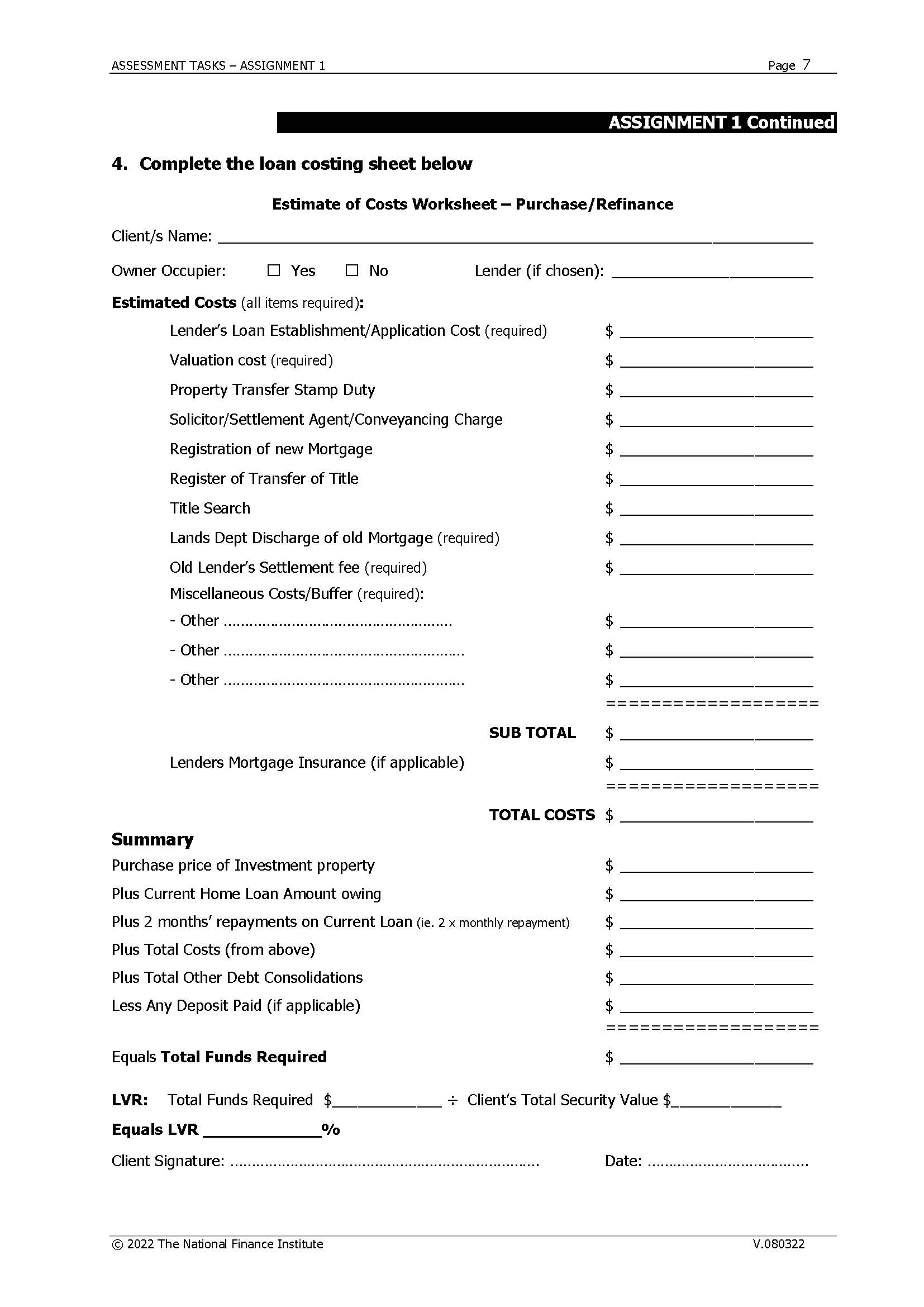

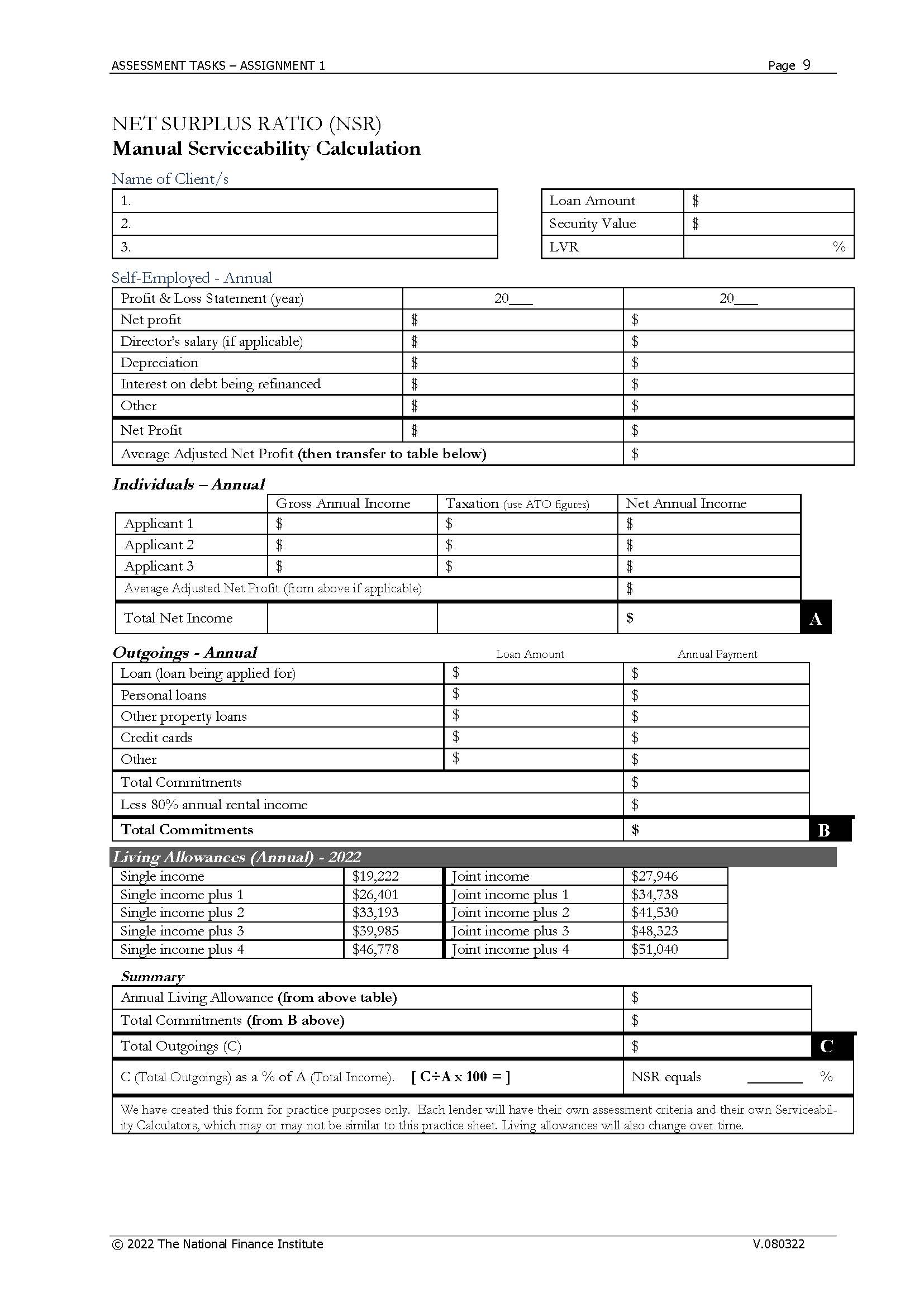

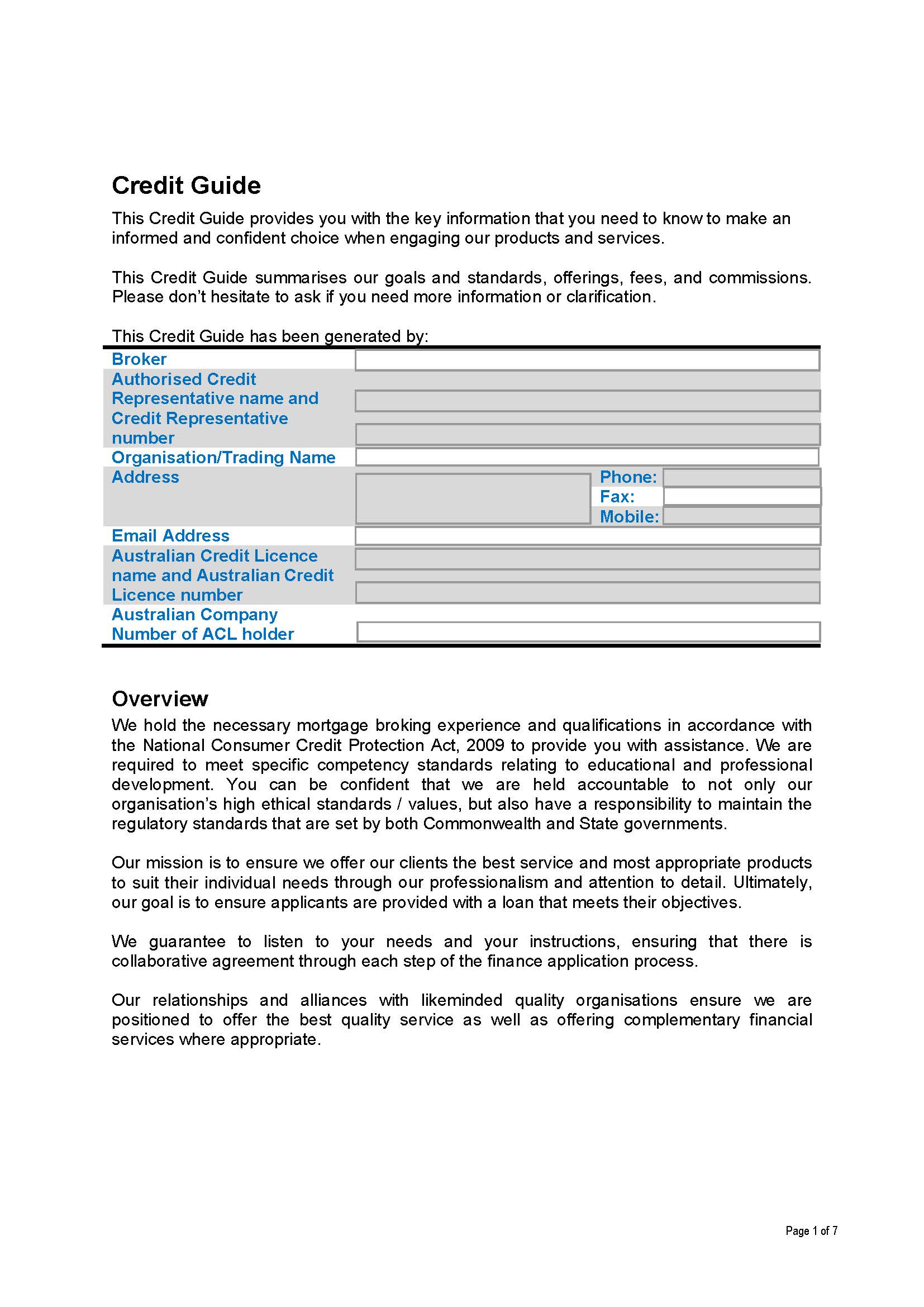

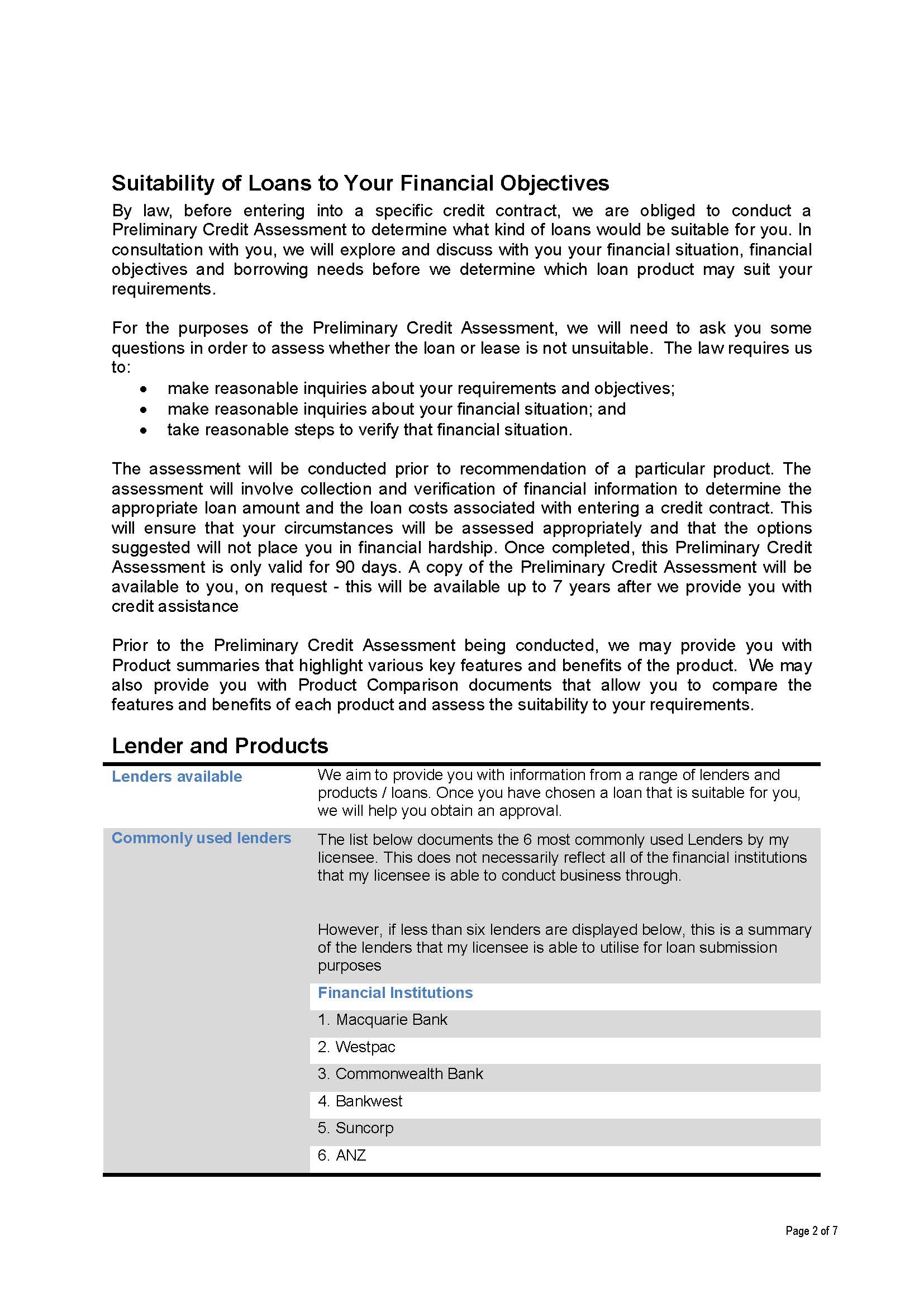

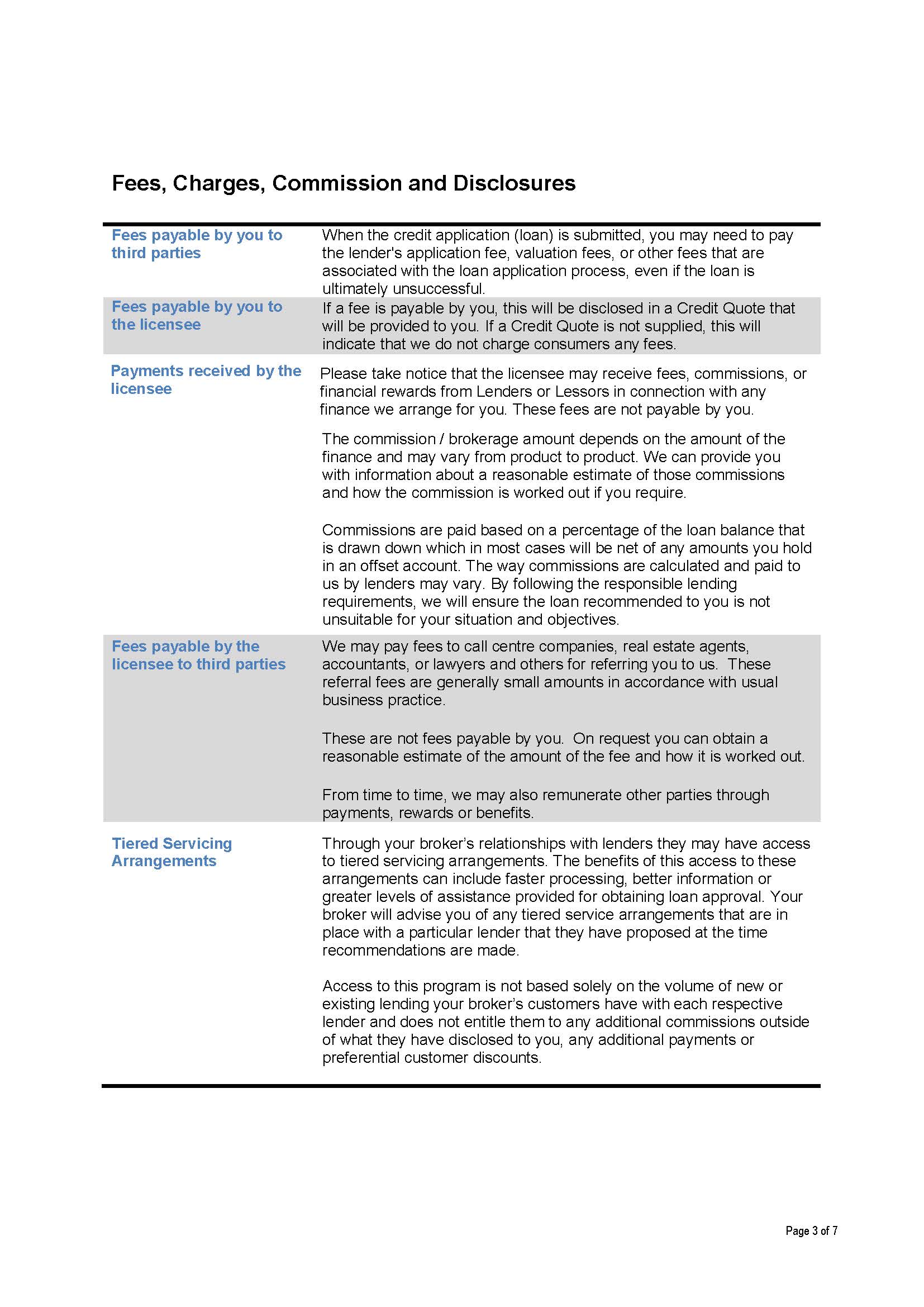

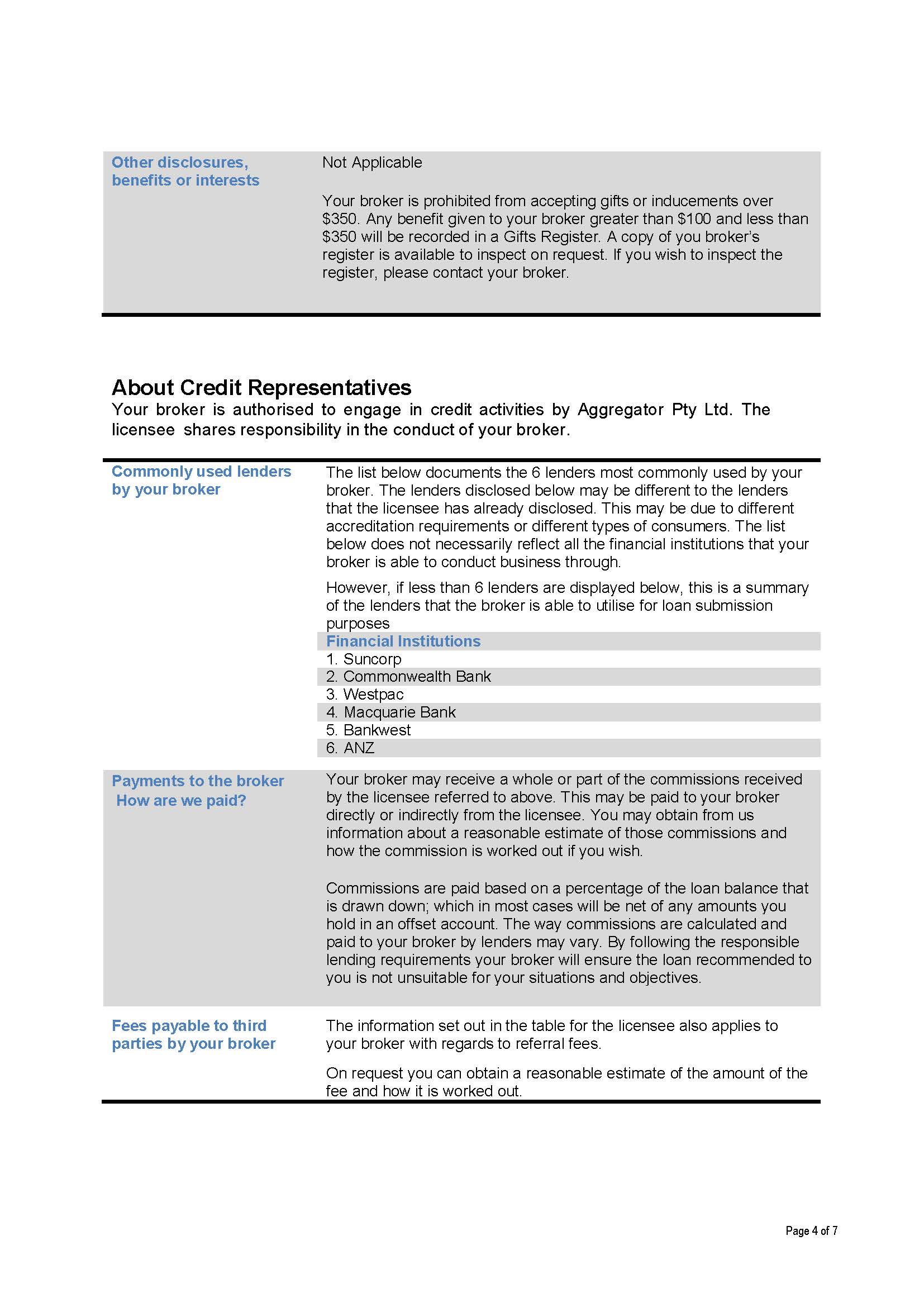

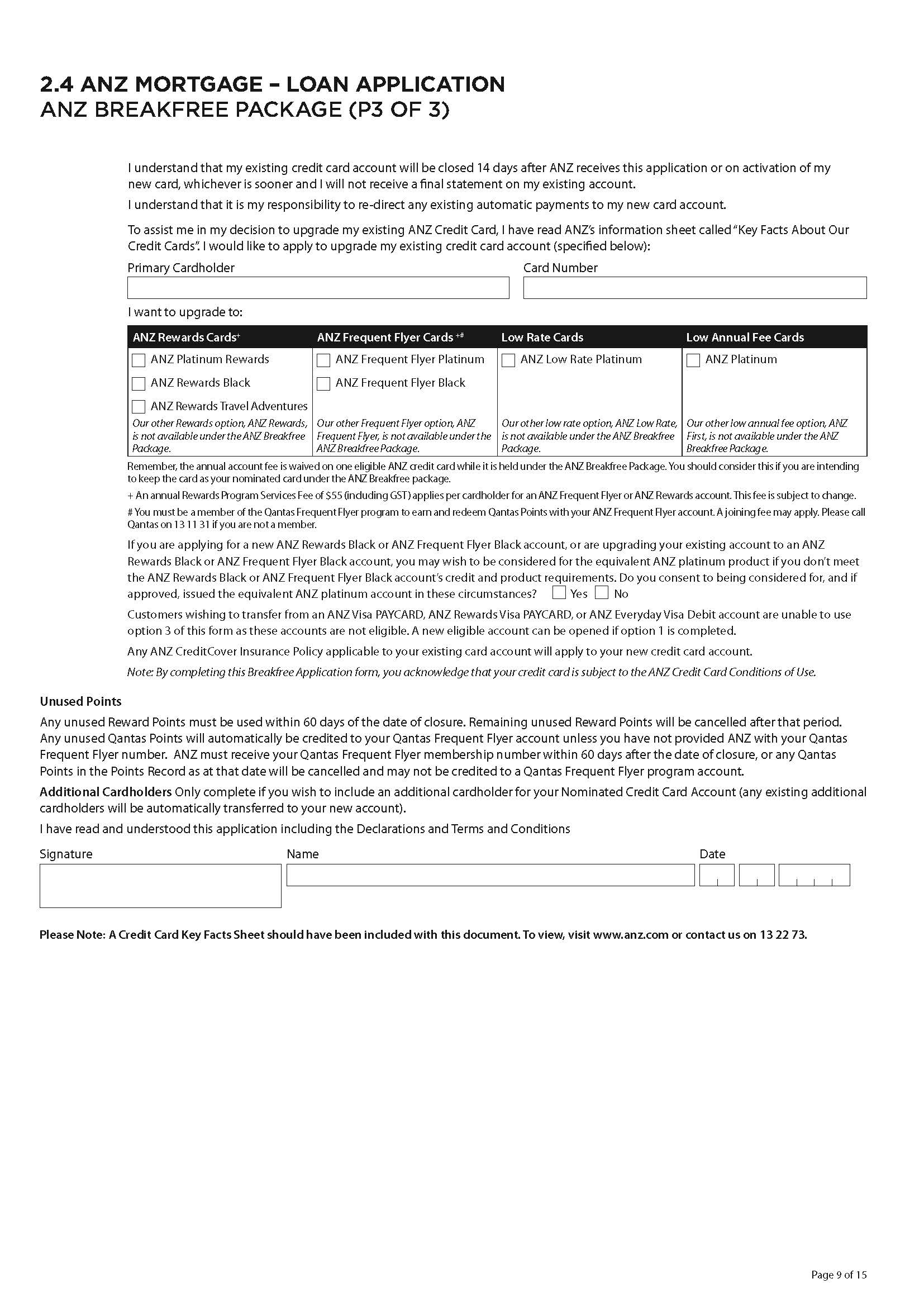

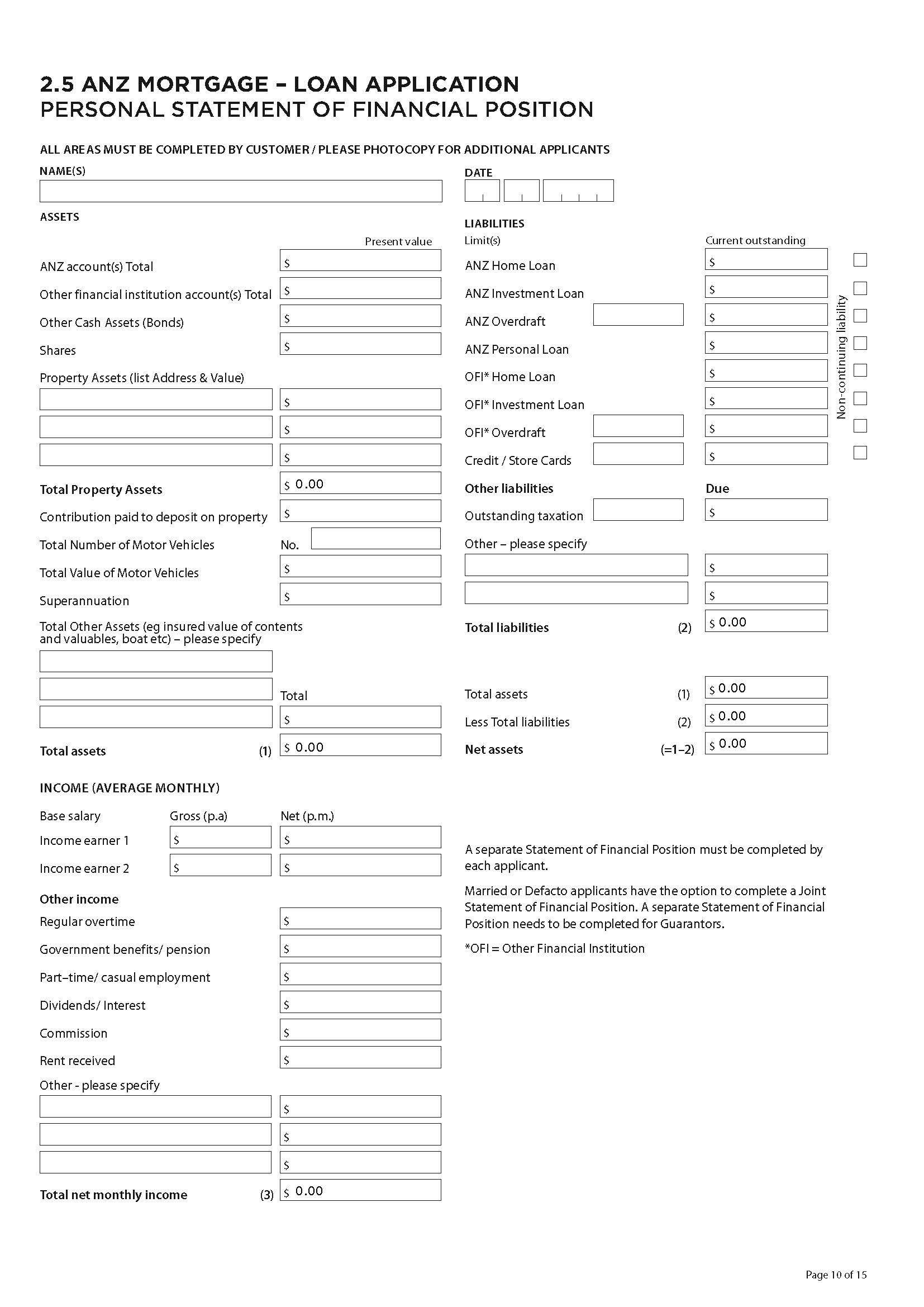

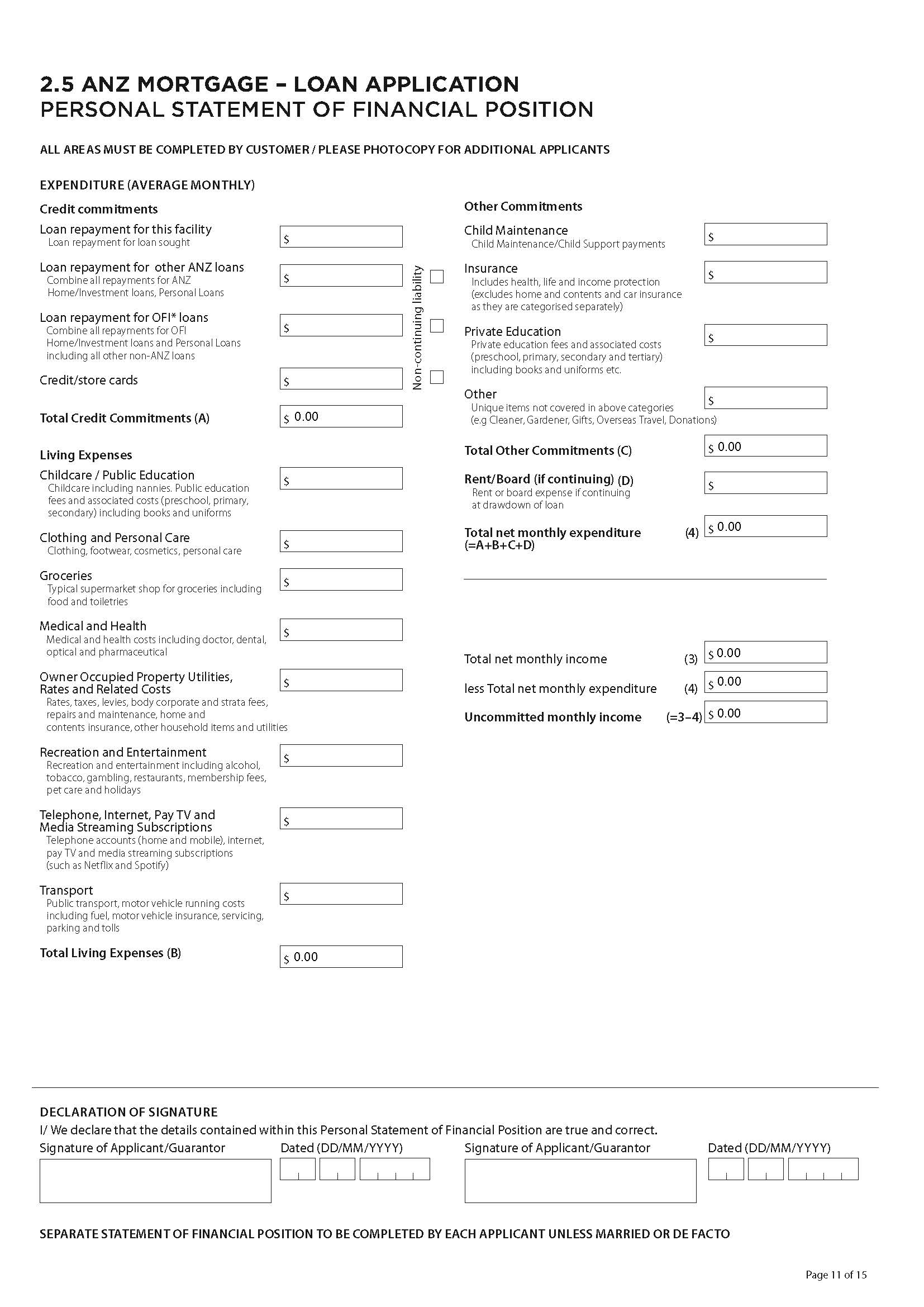

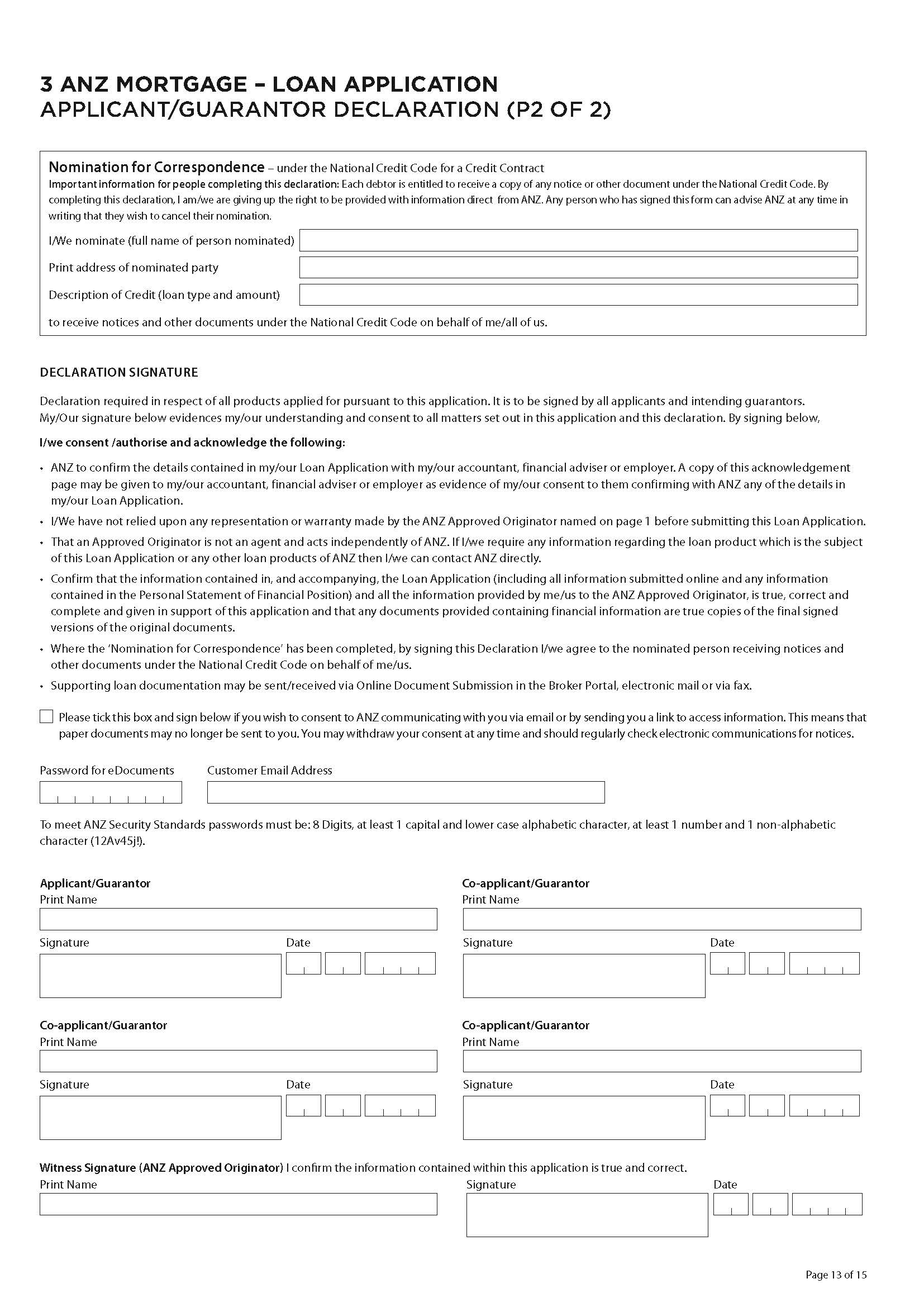

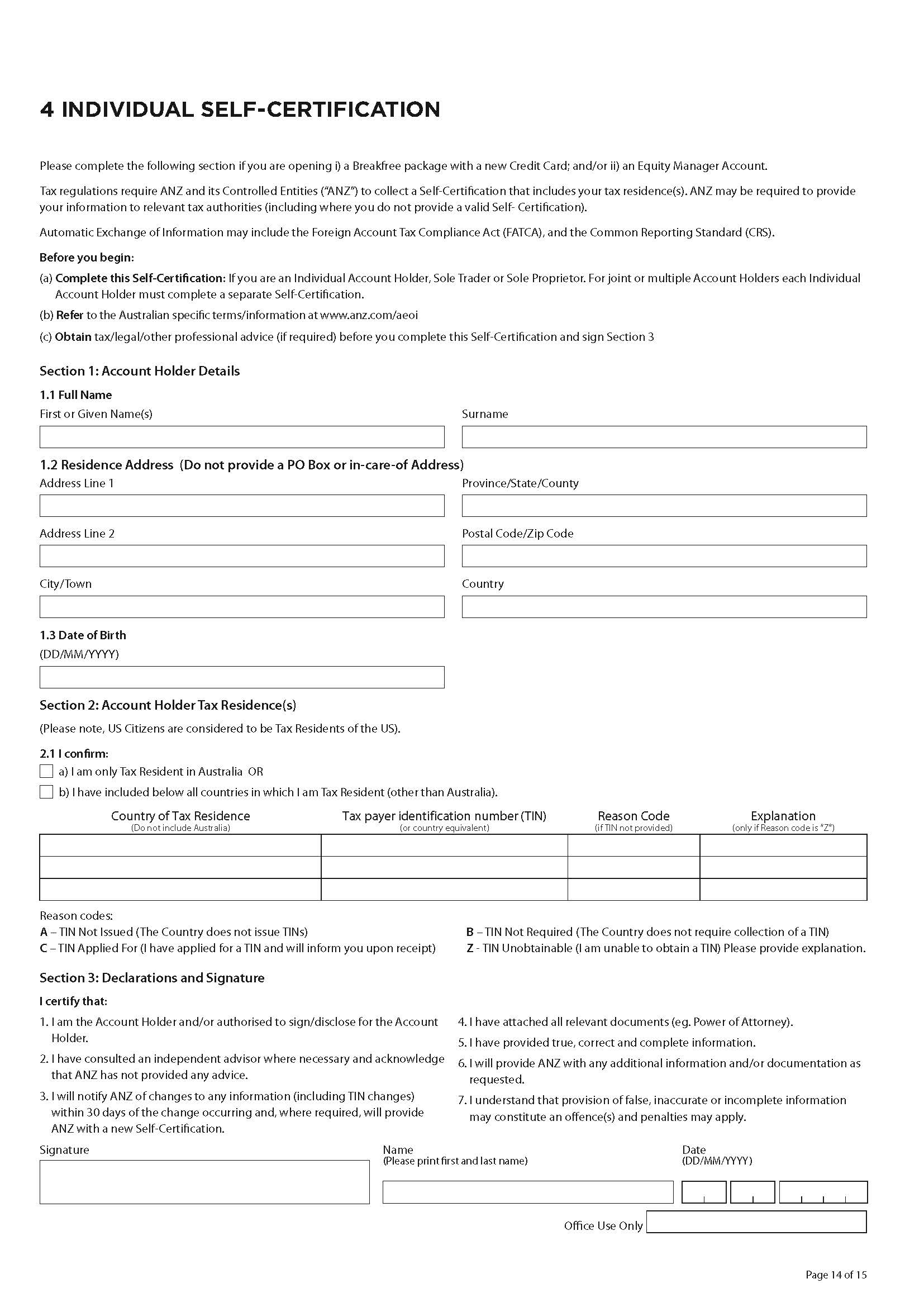

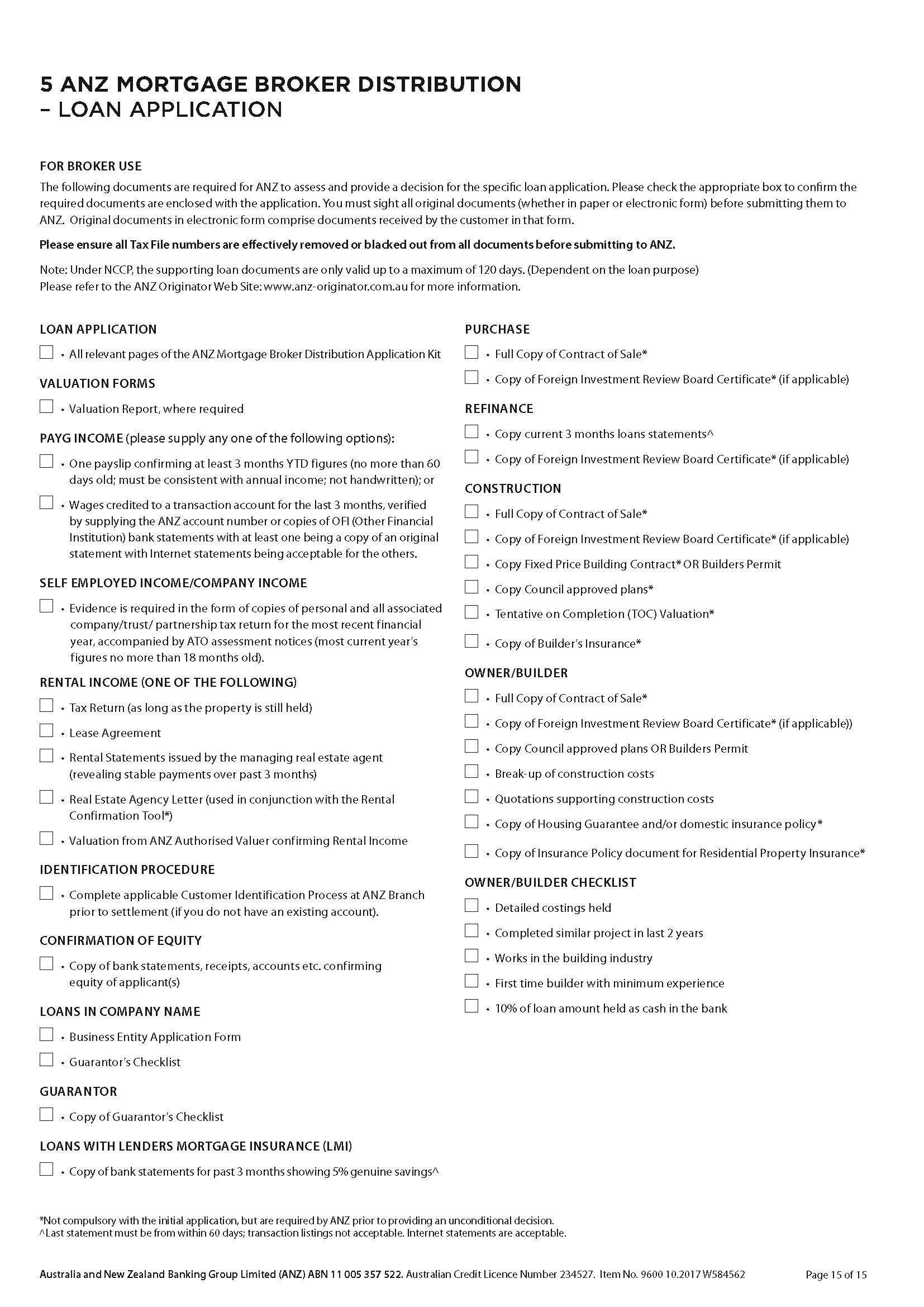

Fact Find Initial Interview: Time Date Location Referred by: A. Personal Details Applicant 1 Applicant 2 Full Name of Applicant Full Name of Applicant Mr Mrs Miss OMS Dr Mr Mrs Miss OMs Dr Full Name Full Name Marital Status Date of Birth Marital Status Date of Birth 1 Mobile Home Phone Mobile Home Phone Work Ph Email Work Ph Email Current Home Address Current Home Address Suburb Postcode Suburb Postcode Time at Current Address Time at Current Address Yrs Mths Yrs Mths vious Ac Previous Address Suburb Postcode Suburb Postcode Time at Previous Address Time at Previous Address Yrs Mths Yrs Mths Name of Nearest Relative / Next of Kin Name of Nearest Relative / Next of Kin Phone Phone Drivers Licence No Drivers Drivers Lic Exp Drivers Licence No Drivers Drivers Lic Exp Lic State Lic State Current Occupation Current Occupation Employer Details Employer Details Company Company Address Address Suburb Postcode Suburb Postcode Time Employed Yrs Mths Start Date 1 1 Time Employed Yrs Mths Start Date 1 1 Employer Contact Name Employer Contact Name Employer Contact Ph Employer Contact Ph Previous Occupation Previous Occupation Name of Previous Employer Name of Previous Employer Time Employed with Previous Employer Time Employed with Previous Employer Yrs Mths Yrs Mths Dependants Dependants Full Name Full Name DOB 1 Financially dependant YES NOO DOB 1 Financially dependant YES NOO Full Name Full Name DOE 1 Financially dependant YES NOD DOE 1 Financially dependant YES NOOB. Income Details Applicant 1 Applicant 2 Employment Status Employment Status Full time ) Part time ) Casual ) Self Employed Full time ) Part time ) Casual ) Self Employed Income Income Annual $ Annual Gross _ Net Gross _ Net Regular Overtime Regular Overtime $ Gross _ Net Annual Gross _) Net Annual Rental Income Rental Income Annual [ Gross _ Net Annual f Gross _ Net Dividends & Dividends & Interest Annual $ Interest Annual Gross _ Net [ Gross _ Net Allowances & Allowances & Pensions Annual Pensions Annual Gross ) Net O Gross _ Net Company Profit Company Profit Annual Annual (Pre-Tax) (Pre-Tax) Add-backs Add-backs Annual Gross _ Net Annual Gross _ Net Other Other Annual $ Annual $ Gross _ Net [ Gross _ Net C. Assets Description Value Joint App App 2 Land & Buildings $ Land & Buildings $ Land & Buildings $ Motor Vehicle Make Year $ O 0 OOOOOO Motor Vehicle Make Year $ Vehicle Make Year Bank Accounts Bank BSE Bank Accounts Bank BSB Superannuateon Fund Superannuateon Fund Home Contents OOOOOOOO Shares (Total) Other Other OtherD. Current Liabilities & Expenses Existing Financier Monthly repayment Amount Owing Limit To be paid out? Mortgages $ $ $ D Yes D \\lo Mortgages $ $ $ El Yes D \\lo Personal Loans $ $ $ D Yes D \\lo Other Loans $ $ $ D Yes D \\lo Overdrafts / LOC $ $ $ El Yes El \\lo Credit Card $ $ $ D Yes B \\IO Credit Card $ $ $ D Yes D \\lo Hire Purchase $ $ $ El Yes I: \\lo Leases $ $ $ D Yes D \\lo Living Expenses Calculation Please complete an estimation of your living expenses after the new loan facility has been drawn Clown. Living Expenses Monthly Cost Leisure / Entertainment Monthly Cost Rent / board 33 Holidays $ Rates (council / water) 33 Restaurants $ Utilities (electricity, gas etc.) 33 Takeaways / snacks $ Telephone / internet 33 Sports / hobbies 55 Mobile phone 33 Memberships 55 Home maintenance 33 Newspapers / Magazines 55 Food / groceries / household $ Books / CD's / DVD's $ Medical & pharmaceuticals $ Gifts $ Clothes / shoes $ Other $ Education $ Total $ Purchases (household furniture etc.) $ Garden $ Motor Vehicles / Transport Monthly Cost Child care / school fees $ Registration $ Pet food / grooming / vet $ Maintenance / repairs $ Other $ Petrol $ Total $ Public transport / taxis $ Parking $ Insurance / Superannuation Monthly Cost Other $ Life $ Total $ Health $ Superannuation voluntary $ Summary Home & Contents $ Living expenses $ Car $ Leisure / entertainment $ Business $ Motor vehicles / transport $ Other (boat / caravan etc.) _ $ Motor vehicles / transport $ [: _ Insurance / superannuation $ Total $ TOTAL MONTHLY COSTS $ E. Security Details Security Property 1 Value $ Land Type Style Owner Residential House _ Town house O Rural O Unit Vacant land Address Duplex Warehouse Serviced Apt Suburb Postcode Other Name of contact for inspection Phone number of contact for inspection Security Property 2 Owner Value $ Land Type Style Residential House _ Town house Rural Unit Vacant land Address O Duplex Warehouse serviced Apt Suburb Postcode Other Name of contact for inspection Phone number of contact for inspection F. Loan Purpose What are your goals and objectives? Do you know of any significant Yes No changes that may impact on your ability to make your loan repayment If yes, what kind of change are you Temporary decrease in income expecting? Permanent decrease in income Anticipated Large expenditure If yes, how will you continue to make Securing additional income O My application reflects these changes oan repayments? Using Reducing expenses f this is a refinance, what are your More Competitive Pricing Improved product features reasons for refinancing? Convenience / Flexibility of the product Part of consolidation / restructuring of Dissatisfaction with existing service finances levels Other Are you a first home buyer? Yes No What is your primary loan purpose? Purchase Construction Top-up Refinance Line of Credit Other What is the source of your deposit? Genuine savings $ Proceeds from property sale $ First Home Owners Grant $ Other savings $ Gifts $ Loan Details Loan Amount Loan Type Principal & Interest Fixed Line of Credit Interest Only Loan Term Years Lender Preferences Is there any lender you would like to deal with, or any lender you would NOT like to deal with? What loan features are important to you? O Offset Variable repayment frequency Cashout Extra Repayments Discount Rate Redraw Repayment Holiday Branch access Other Rate Lock capabilities Capitalised LMI Other Is there any credit history we should be aware of such as defaults, judgements or bankruptcy? No Yes, please provide details:G. Current Insurance Type Insured? Sum Insured Provider Premium Joint App 1 App 2 Life a Yes a No $ $ Total Permanent Disability D Yes D No 33 33 Income Protection D Yes a No 33 $ Trauma D Yes a No $ 55 Building & Contents D Yes a No $ $ Loan Protection D Yes a No $ $ Other D Yes a No $ $ Applicant 1 Applicant 2 Do you smoke? D Yes D No Do you smoke? D Yes D No Signature of applicant Signature of applicant Date / / Date / / confirm that the information contained within this Fact Find Form is true and correct. I confirm that the information contained within this Fact Find Form is true and correct. ASSESSMENT TASKS - ASSIGNMENT 1 Page 1 ASSIGNMENT 1 To be completed by the Trainee You must include this page with your Assignment 1 submission Alternatively, you can retype the full details on this page, including the declaration that this submission is your own work, and use as a front page to your Assignment Trainee name: Trainee postal address: Trainee daytime phone numbers: Trainee email address: By your submission you are stating that this Assignment contains no answers which have been copied from or completed by another person. You acknowledge that you make this statement with the understanding that your assessment may be compromised and marking delayed, if found to be otherwise. The consequences for cheating, plagiarism, unauthorized collaboration, and other forms of academic dis- honesty can include suspension from the course and/or additional assessments with additional fees. Our trainers and assessors decide how to handle violations of such academic integrity on a case-by-case basis. You acknowledge the above. Type or sign your name: Date: Submissions can be mailed to NFI, P.O. Box 1354, Capalaba B.C. Qld 4157 OR upload into the portal OR email to assessments@financeinstitute.com.au (please consider your le sizes if emailing) OFFICE USE ONLY BELOW HERE Date received by NFI: Date received by Assessor: Name of Assessor: Date assessed: Outcome: Further action (if applicable): 2022 The National Finance Institute V.080322 ASSESSMENT TASKS - ASSIGNMENT 1 Page 2 ASSIGNMENT 1 Task Using the information contained in the Scenario below, please complete the following 6 tasks. You must complete each task for your submission to be assessed. Omission of any of these 6 tasks will be regarded as 'Working Towards Competency' and you will then be required to resubmit in full. 1. 9'5"pr Complete the Fact Find document on these clients using the form in Appendix 14. 0 We have not included all supplementary information on these clients in which case you will need to create your own \"improvised\" answers for inclusion in the Fact Find docu- ment. Trainees who already have access to their own version of a Fact Find template may use their own form as an alternative to that provided in Appendix 14. Recommend a product for the clients and explain your reasons for recommendation List the supporting documents that would be needed to support the loan Complete loan costing sheet * Complete a loan servicing calculation (NSR) * Complete a loan application form (an ANZ loan application form has been provided for you, which you must use) and complete all of the accompanying documents as pro- vided for you. Your answer to this task should be prepared as if you were submitting a real loan application to the lender. Please note: If there is information required on the ANZ application form that is not supplied, please improvise. The application should be completed as neatly as possible to ensure ease of review. It is to be submitted to NFI as if NFI is the lender and you were an accredited broker (but you do not need to make up \"dummy" supporting documents eg. rates notice, etc.). If you do not submit in a professional manner, your assessment will not be marked. * Important: The fees and costs required in order to complete this assignment correctly (ie. Esti- mate of Costs worksheet) can be found in Unit 6 and the instructions for how to complete the NSR form are in Unit 7. A Lenders Mortgage Insurance Chart (if you determine LMI is applicable) is found in Unit 6. Trainees should ensure Units 6 and 7 are used to source correct gures for this assignment. Scenao Clients: Jennifer Ann Stern DL No.: 527491 DOB: 07/07/89 Australian Passport No.: L94325880 Scott Milo Stern DL No.: 5489701 DOB: 04/06/88 Australian Passport No.: L9189081 Contact Phone No: Phone 0401 101 111 Current Address: 33 Willow St, Lane Cove, NSW 2066 Time there, 3.7 years Previous Address: 44 Roberts Street, Putney NSW 2112 Time there, 5 years. Children: 2 children aged 6 and 8 Scenario Continued overleaf 2022 The National Finance Institute V.080322 ASSESSMENT TASKS - ASSIGNMENT 1 Page 3 ASSIGNMENT 1 Continued Existing Property: Own Home valued at $1,500,000 Current outstanding loan balance $375,000 (with CBA) Loan Repayments $2,273 per month, remaining loan term 20 years Cash: The clients have $12,000 cash in the bank. Credit Cards: ANZ Visa - $6,000 limit (balance $4,000) NAB MasterCard $6,000 limit (balance $2,500) Other: Mr and Mrs Stern each have $85,000 in superannuation and they estimate their current home and contents to be worth $63,000 Mr Stern works at OfceWorks as a Marketing Manager and earns $125,000 p.a. He has worked there for 8 years. Mrs Stern is a Project Officer with SMEC Australia and earns $76,000 p.a. She has worked there for the past 3 years after having several years of home duties. The Stems own two cars a 2016 Honda Civic worth $18,000 unencumbered and a 2018 Mazda SUV $30,000 subject to Mazda Finance of $20,000 ($450 per month). A few days ago, the Sterns signed up for a 20 month Interest Free loan from Latitude for a sound/movie system for $3,000. They paid a $50 establishment fee to avoid the monthly ad min fee and their minimum monthly payment is 5%. You interviewed Mr and Mrs Stern at your office after some initial telephone conversations previously. They both spoke good English, they are Australian citizens of more than 20 years and they expressed their excitement at buying their second property. Following your evaluation, you suggested 3 different loan products to the Sterns and their decision was to choose the ANZ product. You will now proceed to assist them with their loan application. They are aware that, they will need to complete a Customer Identication Procedure prior to finance approval from the lender. The clients wish to refinance their current home loan and purchase an investment property. The investment property is an established 2 bedroom unit in a residential tower block of 48 at 56 (Lot 6) Victoria Ave, Rhodes and is valued at $900,000. Gross rental Income of $700 per week is expected and the body corporate expense will be just $35 per week. They have made an offer on the unit at the asking price, have put down a $1000 cash deposit with the real estate agent, and the offer has been accepted with settlement in 60 days. Title particulars: Lot 6, Folio 4981, Vol. 2931. The solicitors they will be using are Bader & Partners, ph 0400 111 222 Scenario Continued overleaf 2022 The National Finance Institute V.080322 ASSESSMENT TASKS - ASSIGNMENT 1 Page 4 Assumptions: ASSIGNMENT 1 Continued Assume this is a cross collateralised loan Due to the client's request below, assume this structure will be a Split facility Your clients have told you: that they want to keep the repayments on their home separate from their investment property. They would like to keep the repayments on their home as principal and interest but want to pay interest only on their investment property. Lenders will calculate servicing using the entire loan amount calculated at P&I, even if the loan or part of the loan is provided as Interest only. Assume the clients seek a 25 year term for the loan and the lender will assess servicing at P&I over the 25 year term. The clients wish to pay out their personal loan on the car, as a debt consolidation, to rationalise their loan repayments. They have agreed that ANZ will be a suitable lender for their circumstances. Although addresses show NSW, for the purpose of your duty and other cost calculations, assume that the clients live in the same state as you (the broker). You should assume a Standard Variable Rate of 3% applies to this loan application and a Qualifying rate of 3% is added to the Standard Variable Rate (for your NSR form). Assume the current car loan will be paid out by the refinance of the home. Assume the clients will be \"fulldoc\". Assume that the body corporate cost is included in living expenses and therefore does not need to be included as a se arate out oin . Please note: The table called Living Allowances on the NSR sheet is based loosely on the Henderson Poverty Index and should be used in these assignments, including in the Fact Find form, as we are not using a real client. However, in real life ASIC has ruled that a budget must be completed for each client to assess living expenses (we provide a sample budget form at the back of Appendix 320 for interest). 2022 The National Finance Institute V.080322 ASSESSMENT TASKS - ASSIGNMENT 1 Page 5 ASSIGNMENT 1 Continued 1. Complete the Fact Find provided in Appendix 14 or your own company's Fact Find document (and improvise any information that has not been provided in the scenario). 2. Detail the features of the ANZ product chosen for your clients and explain your reasons for your initial suggestion Write or type your answer in this box 2022 The National Finance Institute V.080322 ASSESSMENT TASKS - ASSIGNMENT 1 Page 6 ASSIGNMENT 1 Continued 3. List the supporting documents that would be needed to support this loan application. Even though there is a checklist in the lender's application form, you must list the documents separately below. Write or type your answer in this box 2022 The National Finance Institute V.080322 ASSESSMENT TASKS - ASSIGNMENT 1 Page 7 ASSIGNMENT 1 Continued 4. Complete the loan costing sheet below Estimate of Costs Worksheet - Purchase/Refinance Client/s Name: Owner Occupier: O Yes No Lender (if chosen): Estimated Costs (all items required): Lender's Loan Establishment/Application Cost (required) Valuation cost (required) Property Transfer Stamp Duty Solicitor/Settlement Agent/Conveyancing Charge Registration of new Mortgage Register of Transfer of Title Title Search Lands Dept Discharge of old Mortgage (required) Old Lender's Settlement fee (required) Miscellaneous Costs/Buffer (required): - Other ..... - Other ..... LA - Other ........ SUB TOTAL Lenders Mortgage Insurance (if applicable) TOTAL COSTS $ Summary Purchase price of Investment property Plus Current Home Loan Amount owing Plus 2 months' repayments on Current Loan (ie. 2 x monthly repayment) Plus Total Costs (from above) Plus Total Other Debt Consolidations Less Any Deposit Paid (if applicable) Equals Total Funds Required $ LVR: Total Funds Required $ + Client's Total Security Value $. Equals LVR Client Signature: ....... Date: ............. 2022 The National Finance Institute V.080322ASSESSMENT TASKS - ASSIGNMENT 1 Page 8 ASSIGNMENT 1 Continued 5. Complete a loan servicing calculation (NSR) by completing the form overleaf. TIPS: - Remember this NSR calculation is based on 2 security properties, but you use only one NSR form. You should calculate your loan repayments based on the qualifying rate we have provided. - Even though the clients have requested Interest Only for their investment property, your loan repayment calculations in this NSR form should be calculated at Principal and Interest over 25 years. - Your NSR final result should not be over 85% 2022 The National Finance Institute V.080322 ASSESSMENT TASKS - ASSIGNMENT 1 Page 9 NET SURPLUS RATIO (NSR) Manual Serviceability Calculation Name of Client/s 1. Loan Amount $ 2 . Security Value $ 3 . LVR % Self-Employed - Annual Profit & Loss Statement (year) 20 20 Net profi $ $ Director's salary (if applicable) $ $ Depreciation $ $ Interest on debt being refinanced $ $ Other $ Net Profit $ Average Adjusted Net Profit (then transfer to table below Individuals - Annual Gross Annual Income Taxation (use ATO figures) Net Annual Income Applicant 1 $ $ Applicant 2 $ $ Applicant 3 $ Average Adjusted Net Profit (from above if applicable) $ Total Net Income $ A Outgoings - Annual Loan Amount Annual Payment Loan (loan being applied for) $ Personal loans Other property loans Credit card Other Total Commitments $ Less 80% annual rental income $ Total Commitments $ B Living Allowances (Annual) - 2022 Single income $19,222 Joint income $27,946 Single income plus 1 $26,401 Joint income plus 1 $34,738 Single income plus 2 $33,193 Joint income plus 2 $41,530 Single income plus 3 $39,985 Joint income plus 3 $48,323 Single income plus 4 $46,778 Joint income plus 4 $51,040 Summary Annual Living Allowance (from above table) Total Commitments (from B above) $ Total Outgoings (C) C C (Total Outgoings) as a % of A (Total Income). [ C+A x 100 = ] NSR equals We have created this form for practice purposes only. Each lender will have their own assessment criteria and their own Serviceabil- ity Calculators, which may or may not be similar to this practice sheet. Living allowances will also change over time. 2022 The National Finance Institute V.080322ASSESSMENT TASKS - ASSIGNMENT 1 Page 10 ASSIGNMENT 1 Continued 6. Complete the lender's application form (a blank ANZ loan application form has been provided for you) and the other documents as provided for you. Your answer to this Activity should be prepared as if you were submitting a real full loan application to the lender. Remember you must treat this as a cross-collateralised split loan structure. Please note: If there is information required on the application that is not supplied, please improvise. The application should be completed as neatly as possible to ensure ease of review. Tax charts, an LMI table (if required) and sundry forms can be found in your course content. You do not need to create any \"dummy\" supporting documents (eg. documents that your client would typically provide to you in a real submission, eg. rates notices), just ensure you list them where required. For this question you must include the following 5 completed forms (all have been provided for you): - Lending Checklist - Credit guide/ Disclosures - Privacy statement and Consent - Loan Application Cover Sheet - ANZ Application form TIPS: > Page 6 of the ANZ form is where you show your split facility structure > You may find that some fields in the ANZ form do not allow editing. This is because there may be formulas in some cells in the form which will, for example, automatically calculate a total. > On page 10-11 of the ANZ form Assets and Liabilities should be shown as what is current ie. pre-settlement but Income and Expenses are to be shown as proposed ie. post settlement. You should estimate all expenses so that they total the same Living Expenses gure used in the NSR sheet. > IMPORTANT: When determining loan splits avoid mixing borrowings for personal use, on which interest is not tax deductible, and borrowings for investment purposes (income producing), on which interest is tax deductible. This requires consideration of the purpose for which the funds are being borrowed (to purchase property or refinance an existing loan) and the individual costs associated with the purchase or renance (the purpose test will determine which costs should be added to which loan split). 2022 The National Finance Institute v.080322 ASSESSMENT TASKS - ASSIGNMENT 1 The following forms should be used for Assignment 1 Question 6. When completing the Loan Application Cover Sheet, trainees with an existing company/employer are permitted to follow the Cover Sheet format specified by their company/employer. For trainees who do not have an existing company/employer cover sheet template available, please use the Loan Application Cover Sheet provided in this group of forms. Copyright 2021) The National Finance Institute V.110821 ASSESSMENT TASKS - ASSIGNMENT 1 Lending Checklist The following list can be used as your Checklist of necessary documentation. Brokers may care to develop a simpler form from some of the headings below to fax or email to their clients to collect information. Other documentation may be required by some lenders, based on unusual circumstances by the applicant. Yes No N/A 1. This Loan Summary Checklist 2. Loan Submission (commission breakdown etc.) 3. NSR Serviceability worksheet 4. Loan Application Form 5. Privacy Act Consent Form 6. Declaration of Purpose 7. Joint Nomination Form 8. Loan Interview Diary Note 9. 100 Point ID Checklist 10. Acknowledgement and Disclosure Form 11. Evidence of Income A. PAYG Income Documentation (minimum 2 forms) EITHER 3 Pay Slips covering the 3 preceding months, with one being within the past four weeks preferably confirming at least three months YTD (consistent with annual income), OR Last 2 years' Tax Return accompanied by an ATO Assessment Notice, OR Group Certificates / PAYG Payment Summary (not handwritten), OR PAYG Payment Summary (if handwritten) accompanied by an ATO assessment Notice Signed and dated letter from employer on employer's letterhead with ACN/ABN confirming full or part-time employment and annual gross income B. Self Employed Proof of ABN where required for the minimum term Applicant's last 2 years personal tax returns and ATO Assessment Notice Business' last 2 years Tax return and Full Financial Statements (when required) Continued Overleaf ... Copyright 2021, The National Finance Institute V.110821ASSESSMENT TASKS - ASSIGNMENT 1 Supplementary documentation Yes No NA 12. Are TENs removed from all financial documentation? 13. Copy of valuation / valuation request LVR % 14. Copy of front page of contract of sale 15. Copy of Offer & Acceptance - purchase / sale 16. Title details (lot/folio/etc. ), plans/specs and/or building contract for construction 17 Evidence of funds to complete (deposit / genuine savings / equity) 18 Proof of genuine savings (as above) evidenced by bank statements over the last 6 months (minimum) 19. Is the FHOG forming part of this loan application? 20. Copies of most recent 6 months bank statements of all loans refinanced 21. Copies of insurance policies ie. current house and contents insurance policy and any life insurance policies 22. Copies of proof of other investments le. Superannuaten statements, share certificates and/or managed investment statements 23. Is suitable documentation held on file to support other income? (eg. Centrelink/Child support/Dividends/Family Trust disbursements) 24. Has sufficient proof of current rental income been provided by way of Rental Statements, Valuation, Current Lease Agreements, Tax Returns? 25. Council Rates and Water Rates Notices for the property being offered as security on a refinance 26. Additional supporting comments 27. Declaration The correctness of these documents is the responsibility of the person signing this Lending Checklist Submitted by: Signature: Date Copyright 2021, The National Finance Institute V.110821Credit Guide This Credit Guide provides you with the key information that you need to know to make an informed and confident choice when engaging our products and services. This Credit Guide summarises our goals and standards, offerings, fees, and commissions. Please don't hesitate to ask if you need more information or clarification. This Credit Guide has been uenerated b : Authorised Credit Representative-nameand Credit Representative number OrganisationITrading Name I:| Address Ph-o ne: Mo bi'l e:' |:I Email Address Australian credit Licence name and Australian Credit License number Australian Company Number of AOL holder Overview We hold the necessary mortgage broking experience and qualifications in accordance with the National Consumer Credit Protection Act, 2009 to provide you with assistance. We are required to meet specific competency standards relating to educational and professional development. You can be confident that we are held accountable to not only our organisation's high ethical standards / values, but also have a responsibility to maintain the regulatory standards that are set by both Commonwealth and State governments. Our mission is to ensure we offer our clients the best service and most appropriate products to suit their individual needs through our professionalism and attention to detail. Ultimately, our goal is to ensure applicants are provided with a loan that meets their objectives. We guarantee to listen to your needs and your instructions, ensuring that there is collaborative agreement through each step of the finance application process. Our relationships and alliances with likeminded quality organisations ensure we are positioned to offer the best quality service as well as offering complementary financial services where appropriate. Page 1 of? Suitability of Loans to Your Financial Objectives By law, before entering into a specific credit contract, we are obliged to conduct a Preliminary Credit Assessment to determine what kind of loans would be suitable for you. In consultation with you, we will explore and discuss with you your financial situation, financial objectives and borrowing needs before we determine which loan product may suit your requirements. For the purposes of the Preliminary Credit Assessment, we will need to ask you some questions in order to assess whether the loan or lease is not unsuitable. The law requires us to: 0 make reasonable inquiries about your requirements and objectives; 0 make reasonable inquiries about your financial situation; and 0 take reasonable steps to verify that financial situation. The assessment will be conducted prior to recommendation of a particular product. The assessment will involve collection and verification of financial information to determine the appropriate loan amount and the loan costs associated with entering a credit contract. This will ensure that your circumstances will be assessed appropriately and that the options suggested will not place you in financial hardship. Once completed, this Preliminary Credit Assessment is only valid for 90 days. A copy of the Preliminary Credit Assessment will be available to you, on request - this will be available up to 7 years after we provide you with credit assistance Prior to the Preliminary Credit Assessment being conducted, we may provide you with Product summaries that highlight various key features and benefits of the product. We may also provide you with Product Comparison documents that allow you to compare the features and benefits of each product and assess the suitability to your requirements. Lender and Products Lenders available We aim to provide you with information from a range of lenders and products I loans. Once you have chosen a loan that is suitable for you, we will help you obtain an approval. Commonly used lenders The list below documents the 6 most commonly'used Lenders by my licensee. This does not necessarily reflect all of the financial institutions that my licensee is able to conduct business through. However, if less than six lenders are displayed below, this is a summary of the lenders that my licensee is able to utilise for loan submission purposes Financial Institutions '1. Macquarie Bank 2. Westpac 3. Commonwealth Bank 4. Bankwest 5. Sunc'orp 6. ANZ Page 2 of? Fees, Charges, Commission and Disclosures Fees payable by you to third parties Fees payable by you to the licensee When the credit application (loan) is submitted, you may need to pay the lender's application fee, valuation fees, or other fees that are associated with the loan application process, even if the loan is ultimately unsuccessful. If a fee is payable by you, this will be disclosed in-a Credit Quote that will be provided to you. If a Credit Quote is not supplied, this will indicate that we do not charge consumers any fees. Payments TBCBiVF-'d by the Please take notice that the licensee may receive fees, commissions, or licensee Fees payable by the licensee to third parties Tiered Servicing Arrangements financial rewards from Lenders or Lessors in connection with any finance we arrange for you. These fees are not payable by you. The commission / brokerage amount depends on the amount of the finance and may vary from product to product. We can provide you with information about a reasonable estimate of those commissions and how the commission is worked out if you require. Commissions are paid based on a percentage of the loan balance that is drawn down which in most cases will be net of any amounts you hold in an offset account. The way commissions are calculated and paid to us by lenders may vary. By following the responsible lending requirements, we will ensure the loan recommended to you is not unsuitable for your situation and objectives. We may pay fees to call centre companies, real estate agents, accountants, or lawyers-and others for referring you to us. These referral fees are generally small amounts in accordance with usual business practice. These are not fees payable by you. On request you can obtain .a reaSonable estimate of the amount ofthe fee and how it is worked out. From time to time, we may also remunerate other parties through payments, rewards or benefits. Through your broker's relationships with lenders they may have access to tiered servicing arrangements. The benefits of this access to these arrangements can include faster processing, better information or greater levels of assistance provided for obtaining loan approval. Your broker will advise you of any tiered service arrangements that are in place with a particular lender that they have proposed at the time recommendations are made. Access to this program is not based solely on the volume of new or existing lending your broker's customers have with each respective lender and does not entitle them to any additional commissions outside of what they have disclosed to you, any additional payments or preferential customer discounts. Page 3 of? Other disclosures, Not Applicable benefits or interests Your broker is prohibited from accepting gifts or inducements over $350. Any benefit given to your broker greater than $100 and less than $350 will be recorded in a Gifts Register. A copy of you broker's register is available to inspect on request. If you wish to inspect the register, please contact your broker. About Credit Representatives Your broker is authorised to engage in credit activities by Aggregator Pty Ltd. The licensee shares responsibility in the conduct of your broker. Commonly used lenders The list below documents the 6 lenders most commonly used by your by your broker broker. The lenders disclosed below may be different to the lenders that the licensee has already disclosed. This may be due to different accreditation requirements or different types of consumers. The list below does not necessarily reflect all the financial institutions that your broker is able to conduct business through. However, if less than 6 lenders are displayed below, this is a summary of the lenders that the broker is able to utilise for loan submission purposes Financial Institutions 1. Suncorp 2. Commonwealth Bank 3. Westpac 4. Macquarie Bank 5. Bankwest 6. ANZ Payments to the broker Your broker may receive a whole or part of the commissions received How are we paid? by the licensee referred to above. This may be paid to your broker directly or indirectly from the licensee. You may obtain from us information about a reasonable estimate of those commissions and how the commission is worked out if you wish. Commissions are paid based on a percentage of the loan balance that s drawn down; which in most cases will be net of any amounts you hold in an offset account. The way commissions are calculated and paid to your broker by lenders may vary. By following the responsible lending requirements your broker will ensure the loan recommended to you is not unsuitable for your situations and objectives. Fees payable to third The information set out in the table for the licensee also applies to parties by your broker your broker with regards to referral fees. On request you can obtain a reasonable estimate of the amount of the fee and how it is worked out. Page 4 of 7Complaints Irrespective of our status as a licensee, representative or credit representative, our reputation is built on matching the appropriate product(s) to the individual's requirements. We go to great lengths to ensure satisfaction with our services and offerings. However, there may be instances from time to time, where applicants may be dissatisfied with the outcomes of our consultation process. If you have a complaint about the service that we provide, the following steps or avenues for resolution are available to you. Step 1 Most complaints arise from miscommunication and can usually be fixed quickly. So, please contact your broker first and express your concerns. Step 2 If the issue is not satisfactorily resolved within 5 working days by talking with your broker we will apply our internal complaints process to manage your complaint appropriately. In this instance, the complaint will be internally escalated to our Complaints Officer. You may also contact the Complaints Officer directly. Complaints Officer Name Steve Nickenoffski Phone 02- 5-555 6666 Email steve@mortgagebroker.netau Address 181 Regent Road Penrith 2750 Note: In some instances your broker may also be fulfilling the role of the Complaints Officer. This will not affect the capacity to have your complaint dealt with appropriately. By using our internal complaints process we hope to assist you to resolve your complaint quickly and fairly. The maximum timeframe in which to provide a written response to you is 45 days, although in pursuit of best practice and the reputation of our organisation, we aim to resolve these issues in a much shorter time frame. Step 3 Although we try hard to resolve a customer's concern in the most considerate and direct manner, if you are not completely satisfied after the above steps have been attempted, you still have other avenues available to resolve the dispute. This is then managed externally and independently. This external dispute resolution (EDR) process is available to you, at no cost. Two EDR schemes may be listed below. This indicates that the Credit Representative and their authorising Licensee are both required to be members (independently) of an ASIC approved EDR scheme. Where a Credit Representatives EDR is displayed, please contact that EDR scheme in the first instance for complaint escalation. EDR (Licensee) EDR (Credit Representative) Name AFCA AFCA Phone 1800 931 678 1800 931 678 Address Australian Financial Complaints Australian Financial Complaints Authority GPO Box 3 Authority GPO Box 3 Melbourne VIC 3001 Melbourne VIC 3001 Page 5 of? Things you should know We don't make any promises about the value of any property you finance with us or its future prospects. You should always rely on your own enquiries. We don't provide legal or financial advice. It is important you understand your legal obligations under the loan, and the financial consequences. If you have any doubts, you should obtain independent legal and financial advice before you enter any loan oontract. Signature Broker Name 8: Date: Client Name & Date: Client Name & Date: Page 6 of? Privacy Disclosure Statement and Consent Each consent given in this document continues until withdrawn in writing. Privacy Disclosure Statement and Consent I/we consent to you using Personal Information, financial information and Oredit Information about me/us for the purpose of arranging or providing credit, insuring credit, and for direct marketing of products and services offered by you or any organisation you are affiliated with or represent each of which may contact me/us for such a purpose including by telephone and electronically. In this document "you" means each of Aggregator Pty Ltd, the Appointed Oredit Service Provider and their organisation and any assignees or transferees of the commissions relating to any credit provided to me arranged by the Appointed Oredit Service Provider or their organisation. In this document, Personal Information' includes any sensitive information (including health information) and any information I/we tell you about any vulnerability I/we may have. The Personal Information provided by me/us will be held by you. I/We can obtain a copy of Aggregator Pty Ltd's Privacy Policy at www.aggregator.net.au. Your privacy policy contains information about how I may access or seek correction of my Persona Information, how you manage that information and your complaints process. If I/we do not provide the requested Personal Information, I/we acknowledge that you may be unable to assist in arranging finance or providing other services. You may disclose Personal Information about me/us to the following types of entities, some of which may be located overseas (including in USA, Canada, Malaysia, India, Ireland, the United Kingdom and the Philippines): any persons who provide credit or other products or services to us, or to whom an application has been made for those products or services; any financial consultants, accountants, lawyers and advisers; any industry body, tribunal, court or otherwise in connection with any complaint; . any person where you are required by law to do so; any of your associates, related entities or contractors (including printing/publication/mailing houses, IT service providers, cloud storage providers, lawyers/accountants); `our referees, such as our employers, to verify information we have provided; . any person considering acquiring an interest in your business or assets; and . any organisation providing online verification of our identities Credit Information I /we hereby authorise you to receive Credit Information from any lender about our credit affairs, and to provide any relevant real estate agent, lawyer, conveyancer, agent or person authorised by me access to my Credit Information, with details of whether finance has been approved for us, and if it has, the terms of that approval, including providing a copy of any approval letter. I/we appoint you as our agent and authorise you to obtain our Credit Information (including both consumer and commercial credit reporting and eligibility information) from a credit reporting body on our behalf. You are authorised to use that Credit Information to assist you to provide services, including credit assistance, to me/us and to assist me/us to apply for credit. In this document 'Credit Information' includes information such as my/our identity information, the type, terms and maximum amount of credit provided to me/us, repayment history information, default information (including overdue payments), court information, new arrangement information, personal insolvency information, disciplinary proceedings, complaints, delinquency, fraud investigations and details of any serious credit infringements. Receiving Information Electronically I/We consent to receiving credit assistance documentation and loan application information electronically. I/We acknowledge and agree that paper documents may no longer be given, electronic communications must be regularly checked for documents and this consent to receive electronic communications may be withdrawn at any time. Full Name of Applicant 1 Signature of Applicant 1 Date Full Name of Applicant 2 Signature of Applicant 2 Date Full Name of Applicant 3 Signature of Applicant 3 Date Full Name of App Signature of Applicant 4 Date Name of Appointed Credit Service Provider Name and contact details of Appointed Credit Service Provider's Organisation (if applicable) including address/email/phone no. Page 7 of 7ASSESSMENT TASKS - ASSIGNNENT 1 LOAN APPLICATION COVER SHEET Date: ............................................................... No. of Pages: ............................ Broker Name: ............................................................................................................................. Broker contact: ................................................................................................ (phone/fax) ..................................................................................................... (mobile) Borrowers: ................................................................................................................. Loan Type: ........................................................ Loan Amount: .............................. Loan Term: ........................................................ Interest Rate: .............................. Loan Purpose: ................................................................................................................. Deposit: ........................................................ Equity: ......................................... Security Details: ................................................................................................................. Estimated LVR: ................................................................................................................. Names on Title: ................................................................................................................. Valuation Details: ................................................................................................................. Income/Employment Details: ..................................................................................................... Recommendation: ................................................................................................................. Attach ments: ................................................................................................................. ............................................................... (Broker signature) Copyright 2021) The National Finance Institute V.110821 \fANZ MORTGAGE BROKER DISTRIBUTION - LOAN APPLICATION COVER SHEET ANZ Please submit via Online Document Submission in the Broker Portal. APPLICATION NUMBER (Office Use Only) PH: 1800 812 785 Number of pages included Business Development Manager Please complete entire application in BLOCK letters. APPROVED ORIGINATOR DETAILS AND AUTHORISATION LOAN INTERVIEW DIARY NOTE AO SAO Name(s) of customer(s) present Approved Originator Company/ Firm Name Location of interview Date of interview Title and Name Preferred Number Were all applicants interviewed in person? Phone Number Fax Number If not, please indicate who was DY ON VIC/TAS NSW/ACT QLD SA/NT OWA Authorised Officer/Contact Name Date Sent Do all of the customers appear to clearly understand English DY ON If No to above, have the services of an LICANT SUMM interpreter been recommended? JY ON Applicant's Name Do all of the customers clearly benefit from taking out this loan Y ON Nominated ANZ Branch for Loan Account (if unknown, insert suburb) If No to above question, what enquiries have been made to ascertain the BSB: 01 level of benefit to each party to the loan? Has the customer completed the Customer Identification Procedure at an ANZ Branch? (ANZ cannot settle the loan until this requirement is met) Yes No Finance Clause Expiry Date Estimated Settlement Date LO Doc 60 Lock Rate The ANZ Lock Rate Fee Payment Provide details of any other pertinent information obtained during the loan Authorisation Form MUST be interview which may be of interest to ANZ or any unusual circumstances you completed. may wish to record. First Home Buyer Interest in Advance LMI (please indicate if this application or any linked application involve Lenders Viortgage Insurance) COMMERCIAL (please indicate if this application has a linked Commercial application) NEW Resident (please indicate if the customer has recently arrived in Australia and is not yet a citizen or permanent resident) NON Resident (please indicate if the customer is a foreign national and resides overseas) STAFF (please indicate if the customer is an ANZ staff member) Page 1 of 15ANZ MORTGAGE BROKER DISTRIBUTION - LOAN APPLICATION COVER SHEET Section 1. Refinances Is the application a refinance of Other Financial Institution (OFI) Lending? Yes No If No, skip below to Section 2. Significant changes in future financial circumstances Reason for refinancing (please select) Reduce/simplify repayments Convenience and flexibility Dissatisfaction with service at current lender More competitive pricing Specific features and products Other (please specify) Refinancing costs: 1. Has the customer obtained a verbal payout quote from the OFI? Yes No 2. If No, recommend customer obtain quote as costs to refinance may be considerable and may change significantly. Amounts: Current outstanding balance plus accrued interest Plus estimated OFI refinancing cost (costs imposed by other financial institutions): e.g.: early repayment fees, break fees, loan transfer fee Loan Approval Fee and discharge fees etc Total amount to refinance Section 2. Significant changes in future financial circumstances Are there any circumstances that the customer is aware of that could affect their ability to repay this loan? For example: Temporary reduction in income Permanent/Long term change in income - Anticipated large expenditure No If No, skip to Section 3. Further investment in shares or managed funds Yes Please specify: If Yes, how does the customer plan to meet repayments during this reduced income period? Please select: Securing additional income Use of Savings Reducing expenditure Sale of Assets If the customers have no plan to meet changed circumstances: Complete Statement of Financial Position (SP) to reflect changes in customer's circumstances, and Recommend customer seek financial advice Section 3. Further investment in shares or managed funds Is loan for investment in shares or managed funds? Yes No If Yes, will the shares or managed funds purchased be used as a security for a margin loan? Yes No If Yes: Recommend customer seeks independent advice from a Financial Advisor Ensure margin loan liability and repayments are included in the Statement of Financial Position. Section 4. Interest Only Reason for customer preferring Interest Only: Investment or future investment Maximise cash flow Temporary reduction in income, e.g. parental leave Anticipated large expense items Other Please specify: Page 2 of 152.1 ANZ MORTGAGE - LOAN APPLICATION PERSONAL AND EMPLOYMENT DETAILS (P1 OF 2) PERSONAL DETAILS PRIMARY APPLICANT PERSONAL DETAILS CO-APPLICANT Applicant Director/ Partner Guarantor Trustee Applicant Director/ Partner Guarantor Trustee Title Surname Title Surname First name Middle name First name Middle name (Please note: this name appears on the Letter of Offer) (Please note: this name appears on the Letter of Offer) Date of birth Gender Permanent Australian Date of birth Gender Permanent Australian OM OF OM OF DY ON Drivers licence number State Drivers licence number State Current housing situation Current housing situation Boarding Own home Renting With parents Caravan Boarding Own home Renting With parents Caravan Other: other: Marital Status Single Married or De facto Marital Status Single Married or De facto Name of spouse Name of spouse No. of dependants Age (in years) of dependants No. of dependants Age (in years) of Home Phone Number Business Phone Number Home Phone Number Business Phone Number Mobile Phone Number Fax Number Mobile Phone Number Fax Number ADDRESS DETAILS (MINIMUM 2 YEAR HISTORY) ADDRESS DETAILS (MINIMUM 2 YEAR HISTORY) Current Address: Street (No. & Name) Current Address: Street (No. & Name) Suburb State Suburb State Postcode Country Postcode Country Time at current address Years Months Time at current address Years Months (If less than 2 years, previous address must also be included) (If less than 2 years, previous address must also be included) Previous Address Details Previous Address Details Street (No. & Name) Street (No. & Name) Suburb State Suburb State Postcode Country Postcode Country MAILING ADDRESS DETAILS (IF DIFFERENT) MAILING ADDRESS DETAILS (IF DIFFERENT) Street (No. & Name) Street (No. & Name) Suburb State Suburb State Postcode Country Postcode Country Page 3 of 152.1 ANZ MORTGAGE - LOAN APPLICATION PERSONAL AND EMPLOYMENT DETAILS (P2 OF 2) EMPLOYMENT DETAILS (MINIMUM 2 YEAR HISTORY) Employment type Full Time Part Time Casual SeIfEmployed Not Employed Occupation EMPLOYMENT DETAILS (MINIMUM 2 YEAR HISTORY) Employment type Full Time Part Time Casual Self Employed Not Employed Occupation Currently under a probationary period Yes No Length of probationary period Current Employer's Name Currently under a probationary period Yes No Length of probationary period Current Employer's Name ABN ABN Street (No. 8: Name) Street (No. 8: Name) Suburb State Suburb State Postcode Country Postcode Country Phone Number Time at current employer Years Months (lfless than 2 years, previous employer must also be included) Previous Employer Phone Number Time at current employer Years Months (lfless than 2 years, previous employer must also be included) Previous Employer Occupation Occupation Time at current employer i Years Months Time at current employer Years Months Page40fl 2.2 ANZ MORTGAGE - LOAN APPLICATION SECURITY DETAILS PLEASE PHOTOCOPY FOR ADDITIONAL SECURITIES SECURITY DETAILS - ONE SECURITY DETAILS - TWO Security type Security type Registered Mortgage 2nd Mortgage Guarantee Registered Mortgage 2nd Mortgage Guarantee other other Security given by Security given by Current Address: Street (No. & Name) Current Address: Street (No. & Name) Suburb State Suburb State Postcode Country Postcode Country Property Purchase Y ON On Market Transaction Y N Property Purchase DY ON On Market Transaction Y N Off the Plan JY ON Off the Plan JY ON Property Status Property Status Established New To be Built Vacant Land Established New To be Built Vacant Land Property Tenure Property Use Property Tenure Property Use Freehold Leasehold Other Owner Investment Freehold Leasehold Other Downer Investment Property Zoning Property Zoning Commercial Industrial Residential Rural Commercial Industrial Residential Rural Rural Life Rural Residential Other Rural Life Rural Residential Other Property Type Property Type Standard Residential Standard Residential Studio / Warehouse Apartments Studio / Warehouse Apartments Multi-dwellings on One Title Multi-dwellings on One Title 1 Bedroom small sized (50m?) University Apartments/Student Accommodation (>50m?) Rural Residential Housing/Rural Housing (>10 hectares) Rural Residential Housing/Rural Housing (>10 hectares) Vacant Land Vacant Land ACT Leasehold ACT Leasehold Property Development Property Development Company Title Units Company Title Units Title Type Title Details Title Type Title Details Torrens Old Law Torrens Wold Law Security Value Guarantee Amount Security Value Guarantee Amount $ $ $ Contract of Sale Held Y ON Contract of Sale Date Contract of Sale Held DY ON Contract of Sale Date Construction Loan JY ON Construction Loan LY ON SOLICITOR DETAILS Name Address Company Suburb State Phone Number Fax Number Postcode Country Page 5 of 152.3 ANZ MORTGAGE - LOAN APPLICATION LOAN SELECTION PLEASE PHOTOCOPY FOR SEPARATE PURPOSE Portfolio - Please download and complete 2.3.1 ANZ Mortgage Distribution - Loan Application Portfolio Details and Sub-account selection. LOAN DETAILS LOAN TYPE Loan Purpose L owner Occupied Investment Purchase Land Purchase New Dwelling Loans in a company/Trust name Land Home Improvement Bridging PRODUCT Refinance Supplementary Standard Variable Simplicity PLUS Construction Debt Purchase (QLD only) Fixed Rate Equity Manager Purchase Established Dwelling Equity Manager - no cheque Other: ... NOTE: Please specify product for split loan under Loan Details. Description Total Amount Sought Approval in Principle Sought S LOAN DETAILS - ONE LOAN DETAILS - TWO Product and Amount Product and Amount S S Loan term sought (this loan) years Loan term sought (this loan) years Fixed Rate term (if applicable) years Fixed Rate term (if applicable) years Lock Rate Y N Progressive Draw Y ON Lock Rate DY ON Progressive Draw DY ON NOTE: Rate is not locked until payment of the Lock Rate Fee is received by ANZ NOTE: Rate is not locked until payment of the Lock Rate Fee is received by ANZ Interest-Only term (if applicable) years Interest-Only term (if applicable) years Repayments frequency Weekly Fortnightly Monthly Repayments frequency Weekly Fortnightly Monthly Frequency for RIL Interest-in-Advance only Frequency for RIL Interest-in-Advance only Monthly Quarterly Half-yearly Annually Monthly Quarterly Half-yearly Annually Statement cycle Statement cycle Monthly Quarterly Half-yearly Monthly Quarterly Half-yearly Security to Product (address) Security to Product (address) OFFSET OFFSET . Does the customer wish to link a current ANZ One (Offset) Account? . Does the customer wish to link a current ANZ One (Offset) Account? Y N If Yes, insert Account Number (if known) Y N If Yes, insert Account Number (if known) FEE DISBURSEMENT FEE DISBURSEMENT Capitalised Lenders Mortgage Insurance OY ON Capitalised Lenders Mortgage Insurance DY ON If you choose 'Y' the LMI will be automatically If you choose 'Y' the LMI will be automatically added to the loan amount requested) added to the loan amount requested) NOTE: All Bank, Security/Government fees and charges and Lenders Mortgage NOTE: All Bank, Security/Government fees and charges and Lenders Mortgage Insurance (if applicable) will be deducted from the total loan amount requested Insurance (if applicable) will be deducted from the total loan amount requested and and automatically disbursed at Settlement (unless Lock Rate selected). automatically disbursed at Settlement (unless Lock Rate selected). REFINANCE DETAILS (IF APPLICABLE) Other Financial Institution (OFI) Other Financial Institution (OFI) OFI Account Number OFI Amount OFI Account Number OFI Amount $ $ Page 6 of 152.4 ANZ MORTGAGE - LOAN APPLICATION ANZ BREAKFREE PACKAGE (P1 OF 3) TO BE COMPLETED ONLY FOR ANZ BREAKFREE PACKAGE This form must be completed in full to ensure efficient processing Application Number Existing ANZ Breakfree Package Customer? If Yes, add to existing package OR Open a new package (please complete below sections 1A, 1B and 1C) For NEW BREAKFREE CUSTOMERS: NOMINATION OF MANDATORY ACCOUNTS I/We nominate the following Nominated Accounts, as specified in section 1A, 1B and 1C. (Please note that each applicant under the ANZ Breakfree Package must be an account holder (either jointly or alone) for at least one of the Nominated Accounts. Refer to the ANZ Breakfree Terms and Conditions for full details. 1A. NOMINATED LOAN ACCOUNT(S) List all ANZ Home and Investment Loans held by the applicants (either individually or jointly), to be eligible for Total Lending Discounts on the Nominated Loan Accounts being linked to the Package by this request. Account Holder(s Account Number(s) Current Loan Balance(s) Total ANZ Mortgage Lending 1B. NOMINATED TRANSACTION ACCOUNT (PLEASE SELECT ONE) Note: The Annual package fee will be charged to your Nominated transaction account once your loan is drawn. Transaction account must be ANZ Access Advantage account, ANZ One account or ANZ Equity Manager facility. I/We will need to open a new transaction account as part of this Package (please contact an ANZ Branch to organise; transaction account must be opened before Settlement date) OR I/We will nominate the following ANZ Transaction Account as part of this Package. Account Number Account Holder(s) Optional ANZ Assured facility (please select one). Usually we suggest ANZ Assured to provide cover for temporary expenses arising on your ANZ Everyday account. Is this what you are planning to use ANZ Assured for? Yes No 1) I/We do not require an ANZ Assured facility OR already have an ANZ Assured facility. I/We require an ANZ Assured facility with a credit limit of (please select one) |] $500 $1,000 and request that it be linked to the above account If applying for the $1,000 limit and you do not meet the credit product requirements for the $ 1,000 limit you have applied for, do you consent to being considered for, and if approved, issued with a $500 limit? Yes LI No, only consider me for a $ 1,000 limit and if declined, do not consider me for a $500 limit. I/We acknowledge that the ANZ Assured & Personal Overdraft - Terms and Conditions govern any use of an ANZ Assured facility. If ANZ accepts my/our application for ANZ Assured, I/we understand that ANZ will provide me/us with these Terms and Conditions. Page 7 of 152.4 ANZ MORTGAGE - LOAN APPLICATION ANZ BREAKFREE PACKAGE (P2 OF 3) 1C. NOMINATED CREDIT CARD ACCOUNT - Note: To avoid delays in the receipt of credit cards, please ensure Option 1, 2 or 3 is completed IN FULL Note: If you do not select a card account type below for Option 1 or Option 3, the ANZ Platinum account will be selected as your Nominated credit card account. if you do not nominate a Primary Cardholder for Option 1 or Option 3, Applicant 1 will be selected as the Primary Cardholder. New Card Account Required Option 1 I wish to apply for the credit card account selected below, with the understanding that the minimum credit limit for any ANZ platinum (including ANZ Rewards Travel Adventures) account is $6000 and an ANZ Rewards Black or ANZ Frequent Flyer Black account is $ 15,000. My nominated amount for this card is $ but

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

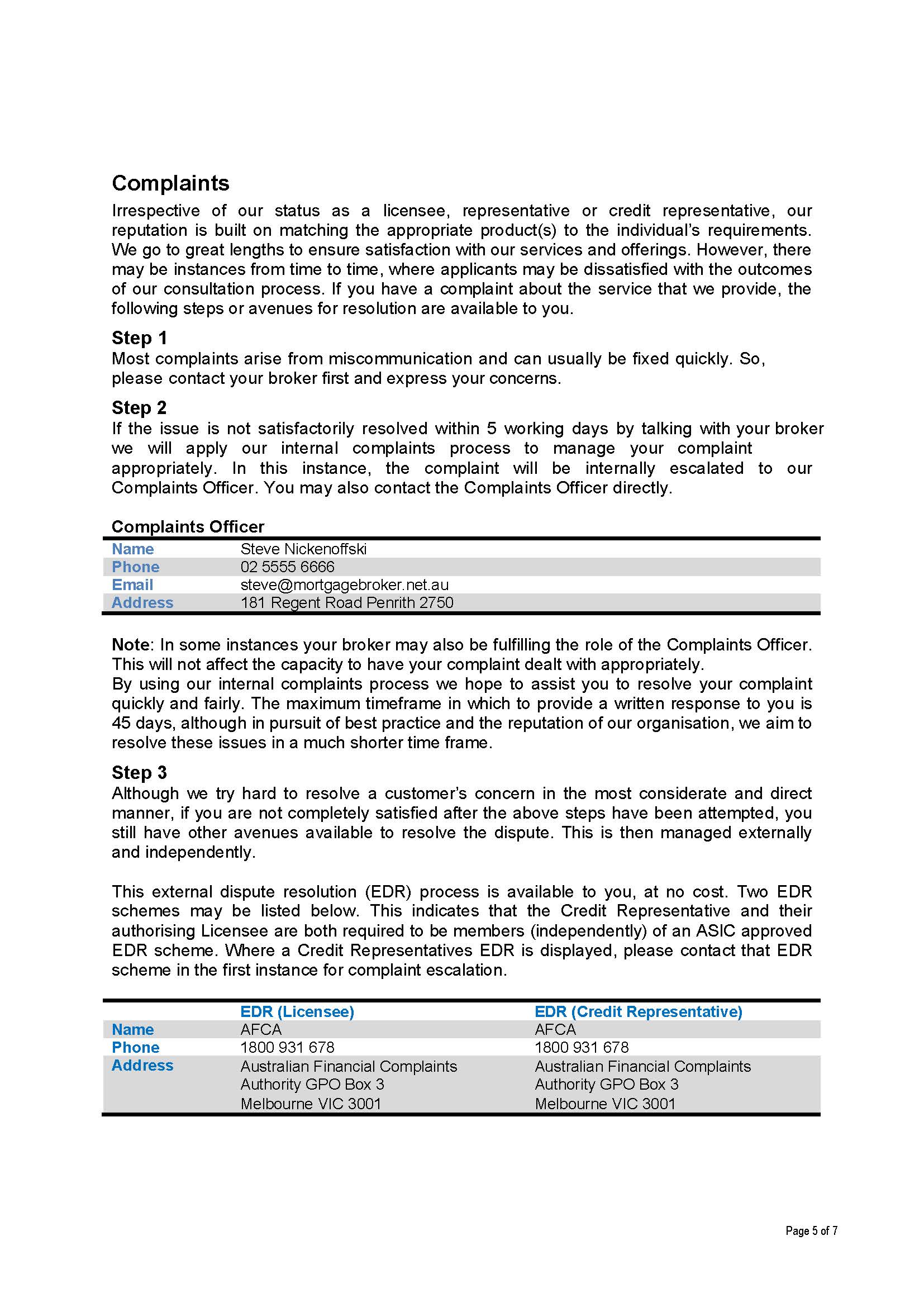

Students Have Also Explored These Related Finance Questions!