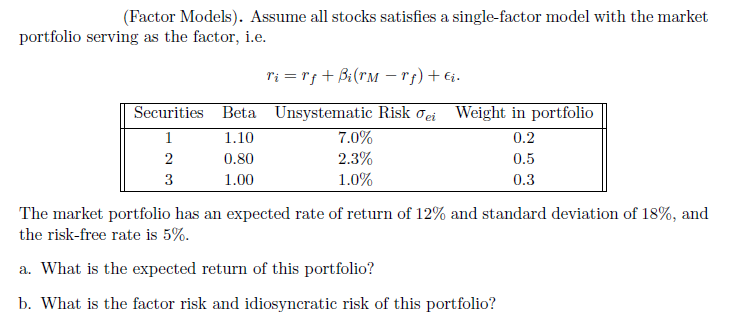

Question: (Factor Models). Assume all stocks satisfies a single-factor model with the market portfolio serving as the factor, i.e. ri=rf+i(rMrf)+i. The market portfolio has an expected

(Factor Models). Assume all stocks satisfies a single-factor model with the market portfolio serving as the factor, i.e. ri=rf+i(rMrf)+i. The market portfolio has an expected rate of return of 12% and standard deviation of 18%, and the risk-free rate is 5%. a. What is the expected return of this portfolio? b. What is the factor risk and idiosyncratic risk of this portfolio

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock