Question: Figure 2 : CAPM Evaluation for Fund I and II ( c ) Based on CAPM regression results in Figure 2 , could we tell

Figure : CAPM Evaluation for Fund I and II

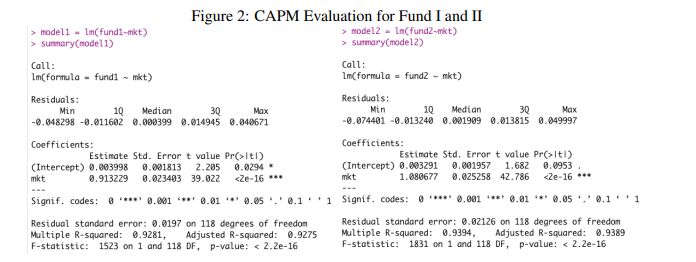

c Based on CAPM regression results in Figure could we tell if Fund I deliver a positive alpha beyond the market? Please write down the null hypothesis and make your conclusion. Hint: You are allowed to use to approximate for the calculation.

d Based on CAPM regression results in Figure could we tell if Fund II has a market beta of Please write down the null hypothesis and make your conclusion. Hint: You are allowed to use to approximate for the calculation.

e Based on above analysis, if the market drops or in September, what is the probability for both Fund I and II lose or for a month?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock