Question: Fill out the chart exactly as provided using the following information: You'll develop a multi-year cash flow proforma projection for an office building with multiple

Fill out the chart exactly as provided using the following information:

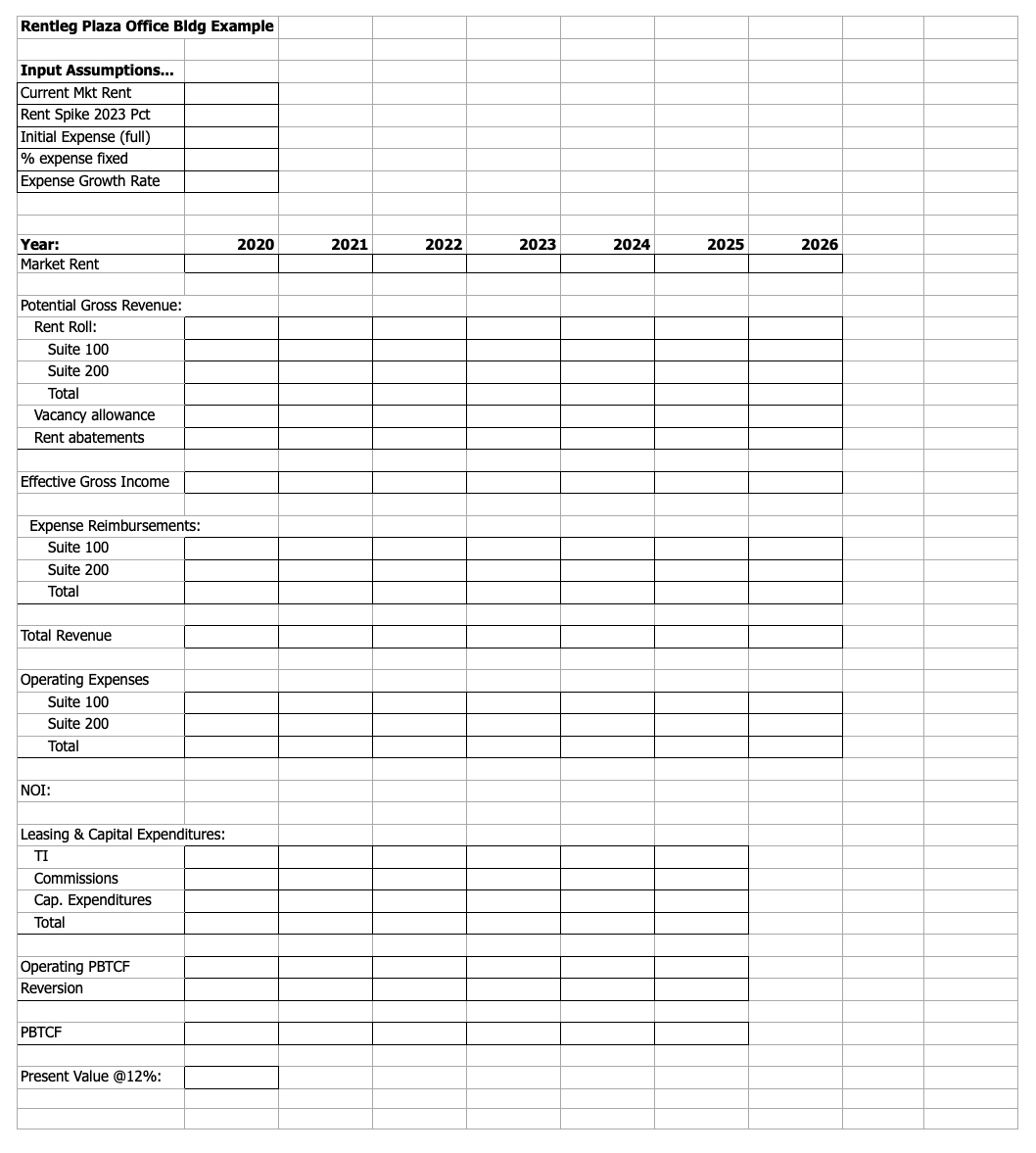

You'll develop a multi-year cash flow proforma projection for an office building with multiple long-term leases, using a provided spreadsheet template.

The office building, Rentleg Plaza, has 30,000 net rentable square feet divided into two office suites. Suite 100 is 20,000 SF and is leased out under a 5-year lease signed 2 years ago (3 more years left on the lease) at $15.00/SF (per year). (Suppose it is the end of 2020, so the lease expires in 3 years at the end of 2023.) The other office, Suite 200, is 10,000 SF and is currently vacant.

In the land where Rentleg Plaza is located, the past few years have seen the office market softened greatly due to excess supply of newly-built space. As a result, rents have fallen. The currently typical rental rate in the market for buildings like Rentleg Plaza is $14.00/SF on 5-year leases, with concessions amounting to one month free rent up front for each year of lease term (e.g., a 5-year lease would get the first 5 months rent free). In these conditions, you expect Suite 200 will not lease up for a year (i.e., expected occupancy after 12 months, at the beginning of 2022, in a 5-year lease running through 2026), and will require $10/SF Tenant Improvement (Tenant Finishing) expenditures by the landlord at that time.

With virtually no new office building development on the horizon, it is likely that the present modest growth in office demand will bring the rental market back into equilibrium within, say, 3 years, so that by 2023 we will be back into something like equilibrium. In these circumstances, it is reasonable to forecast no growth in (nominal) rental rates in the market for the next two years (2020-2022) followed by a rent growth spike of, lets say, 20%, in 2023, with then no further growth in rents for the next few years beyond that time. We would also expect the rent concessions (e.g., the free rent up front) to disappear from typical market deals by 2023.

Suppose it is reasonable to assume that when the lease on Suite 100 expires, there is only a 50% chance the existing tenant will renew. If they do not renew, there will be 6 months vacancy in the space, and it will require $10.00/SF in tenant improvement expenditures (TI) paid for by the landlord in the first year of lease (plus a 6% commission to a leasing broker) to obtain a new tenant. On the other hand, if the current tenant does renew (50% probability), it will only require $3.00/SF in TI plus a 3% brokerage commission. The brokerage commissions are paid by the landlord, up front at the time the lease is signed, based on the entire (undiscounted) cumulative revenue of the lease, less free rent concessions.

The type of lease that is common in the market in which Rentleg Plaza competes is what is known as a gross or full service lease, with an expense stop. This means that the landlord pays the building operating expenses, except that the tenant must pay their pro-rata share of any expenses over and above a stop amount specified in the lease. The stop amount is typically defined at or near the annual operating expenses (per SF) which the building was experiencing as of the time when the lease was signed. The expense stop on the existing lease in Suite 100 is $4.00/SF. The expense stop in the new lease in Suite 200 is expected to be $5.00/SF, and the expense stop in all following leases is expected to be the pro-rata operating expense of that space in its first year of occupancy.

The current operating expenses of the building (projected for 2021) would be $4.81/SF if the building were fully occupied all year; of which 19% are variable, that is, directly proportional to occupancy, while the remaining 81% are fixed (independent of occupancy). Operating expenses are expected to grow at the rate of 4% per year.

In addition to normal operating expenses and the previously noted leasing and tenant improvement expenditures, there is also expected to be $1.00/SF/yr of general capital improvement expenditures.

Assume that the reversion cap rate at the end of year 5 is 10%, and the discount rate is 12% per annum. The seller pays 5% brokers commission.

This is the type of pro forma that a broker would typically take to a potential investor, or a borrower would take to a lender. (Keep in mind that a real world pro forma is typically 10 years, not 5, and buildings often have dozens of spaces and leases (not just two), as well as several individual operating expense line items. Nevertheless, this simple example should be sufficient to help you to understand the basic nuts and bolts.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts