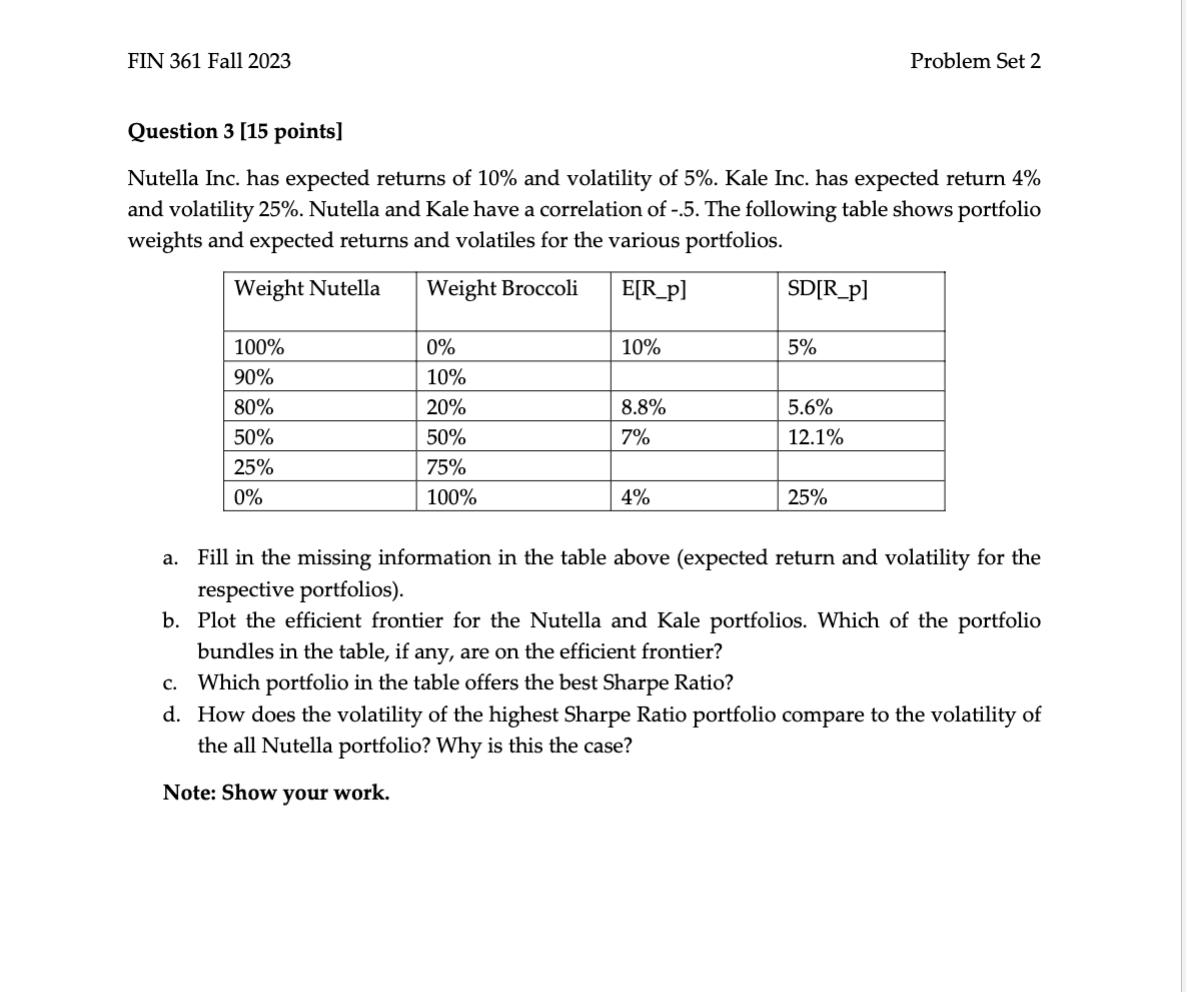

Question: FIN 361 Fall 2023 Problem Set 2 Question 3 [15 points] Nutella Inc. has expected returns of 10% and volatility of 5%. Kale Inc. has

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts