Question: FIN3003 Home Assignment 2 (Due date: 30 Oct) The assignment can be handwritten or typed. Submission in pdf format via Moodle. You are required to

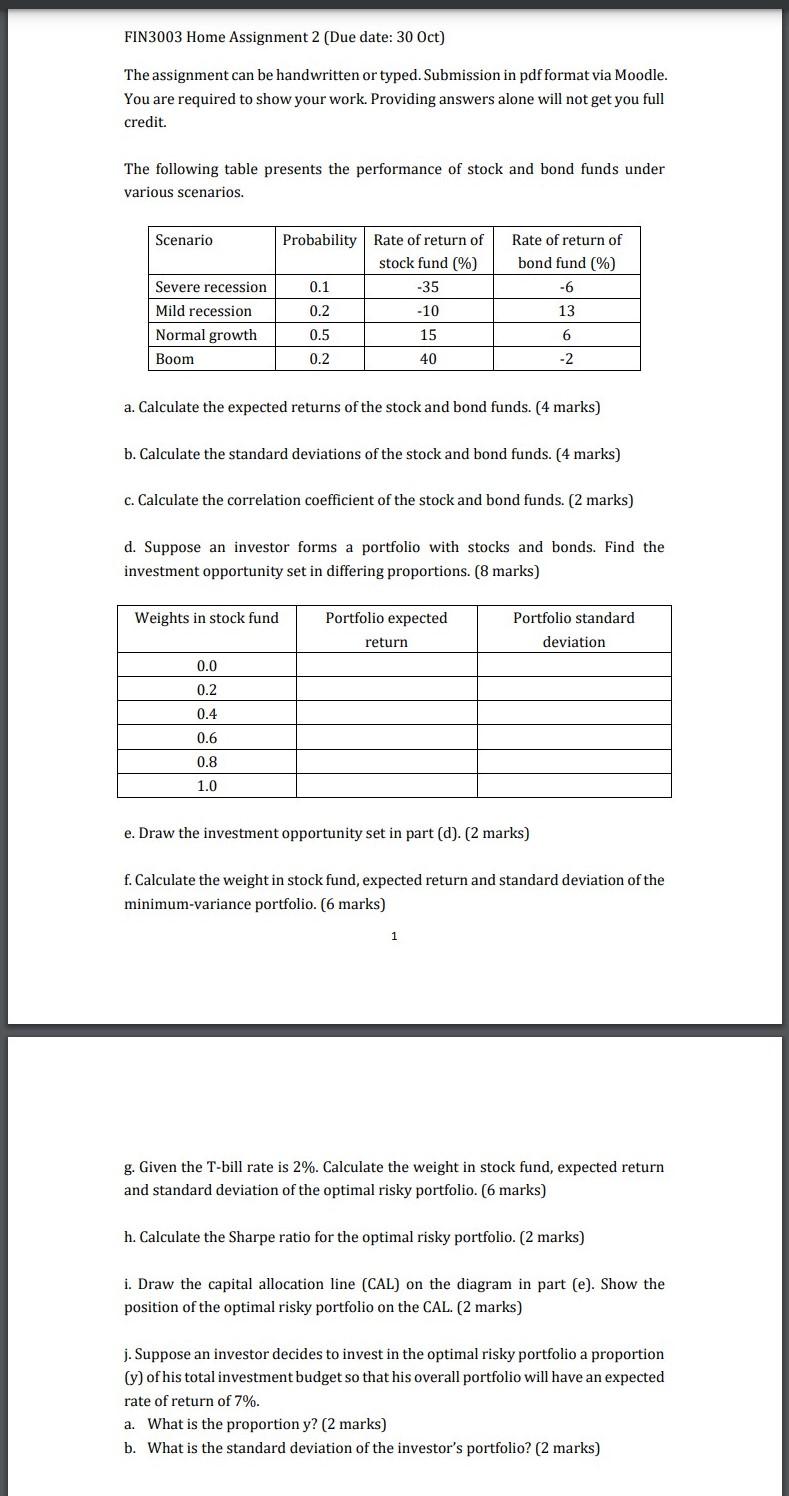

FIN3003 Home Assignment 2 (Due date: 30 Oct) The assignment can be handwritten or typed. Submission in pdf format via Moodle. You are required to show your work. Providing answers alone will not get you full credit. The following table presents the performance of stock and bond funds under various scenarios. Scenario Probability Rate of return of bond fund (%) Rate of return of stock fund (%) -35 -10 -6 0.1 0.2 13 Severe recession Mild recession Normal growth Boom 15 6 0.5 0.2 40 -2 a. Calculate the expected returns of the stock and bond funds. (4 marks) b. Calculate the standard deviations of the stock and bond funds. (4 marks) c. Calculate the correlation coefficient of the stock and bond funds. (2 marks) d. Suppose an investor forms a portfolio with stocks and bonds. Find the investment opportunity set in differing proportions. (8 marks) Weights in stock fund Portfolio expected Portfolio standard deviation return 0.0 0.2 0.4 0.6 0.8 1.0 e. Draw the investment opportunity set in part (d). (2 marks) f. Calculate the weight in stock fund, expected return and standard deviation of the minimum-variance portfolio. (6 marks) g. Given the T-bill rate is 2%. Calculate the weight in stock fund, expected return and standard deviation of the optimal risky portfolio. (6 marks) h. Calculate the Sharpe ratio for the optimal risky portfolio. (2 marks) i. Draw the capital allocation line (CAL) on the diagram in part (e). Show the position of the optimal risky portfolio on the CAL. (2 marks) j. Suppose an investor decides to invest in the optimal risky portfolio a proportion (y) of his total investment budget so that his overall portfolio will have an expected rate of return of 7%. a. What is the proportion y? (2 marks) b. What is the standard deviation of the investor's portfolio? (2 marks) FIN3003 Home Assignment 2 (Due date: 30 Oct) The assignment can be handwritten or typed. Submission in pdf format via Moodle. You are required to show your work. Providing answers alone will not get you full credit. The following table presents the performance of stock and bond funds under various scenarios. Scenario Probability Rate of return of bond fund (%) Rate of return of stock fund (%) -35 -10 -6 0.1 0.2 13 Severe recession Mild recession Normal growth Boom 15 6 0.5 0.2 40 -2 a. Calculate the expected returns of the stock and bond funds. (4 marks) b. Calculate the standard deviations of the stock and bond funds. (4 marks) c. Calculate the correlation coefficient of the stock and bond funds. (2 marks) d. Suppose an investor forms a portfolio with stocks and bonds. Find the investment opportunity set in differing proportions. (8 marks) Weights in stock fund Portfolio expected Portfolio standard deviation return 0.0 0.2 0.4 0.6 0.8 1.0 e. Draw the investment opportunity set in part (d). (2 marks) f. Calculate the weight in stock fund, expected return and standard deviation of the minimum-variance portfolio. (6 marks) g. Given the T-bill rate is 2%. Calculate the weight in stock fund, expected return and standard deviation of the optimal risky portfolio. (6 marks) h. Calculate the Sharpe ratio for the optimal risky portfolio. (2 marks) i. Draw the capital allocation line (CAL) on the diagram in part (e). Show the position of the optimal risky portfolio on the CAL. (2 marks) j. Suppose an investor decides to invest in the optimal risky portfolio a proportion (y) of his total investment budget so that his overall portfolio will have an expected rate of return of 7%. a. What is the proportion y? (2 marks) b. What is the standard deviation of the investor's portfolio? (2 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts