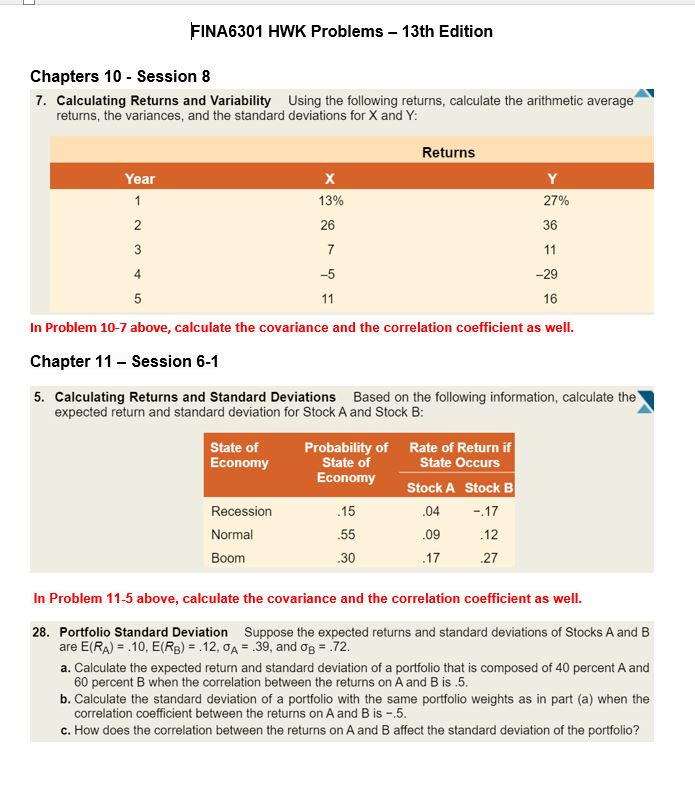

Question: FINA6301 HWK Problems 13th Edition Chapters 10 - Session 8 7. Calculating Returns and Variability Using the following returns, calculate the arithmetic average returns, the

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock