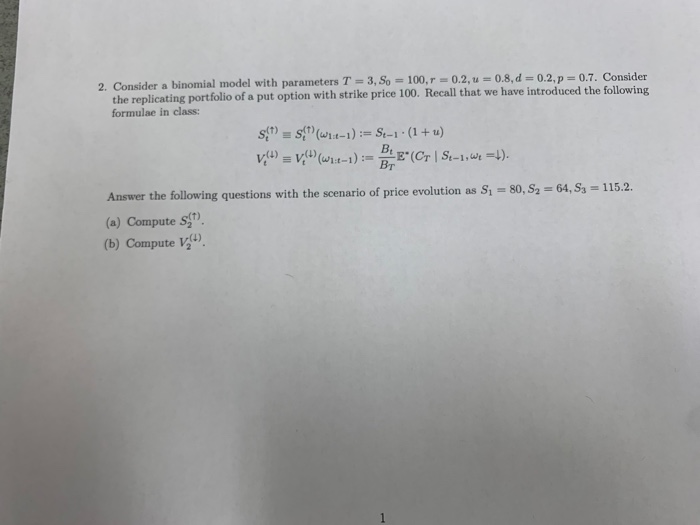

Question: Finacial Modeling 2. Consider a binomial model with parameters T-3, So-100, r 0.2, u-: 08, d-0.2, p-0.7. Consider the replicating portfolio of a put option

2. Consider a binomial model with parameters T-3, So-100, r 0.2, u-: 08, d-0.2, p-0.7. Consider the replicating portfolio of a put option with strike price 100. Recall that we have introduced the following formulae in class: wit-1) Answer the following questions with the scenario of price evolution as S 80,S2 64, Sa 115.2 (o) Compute s$" (b) Compute Vv 2. Consider a binomial model with parameters T-3, So-100, r 0.2, u-: 08, d-0.2, p-0.7. Consider the replicating portfolio of a put option with strike price 100. Recall that we have introduced the following formulae in class: wit-1) Answer the following questions with the scenario of price evolution as S 80,S2 64, Sa 115.2 (o) Compute s$" (b) Compute Vv

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts