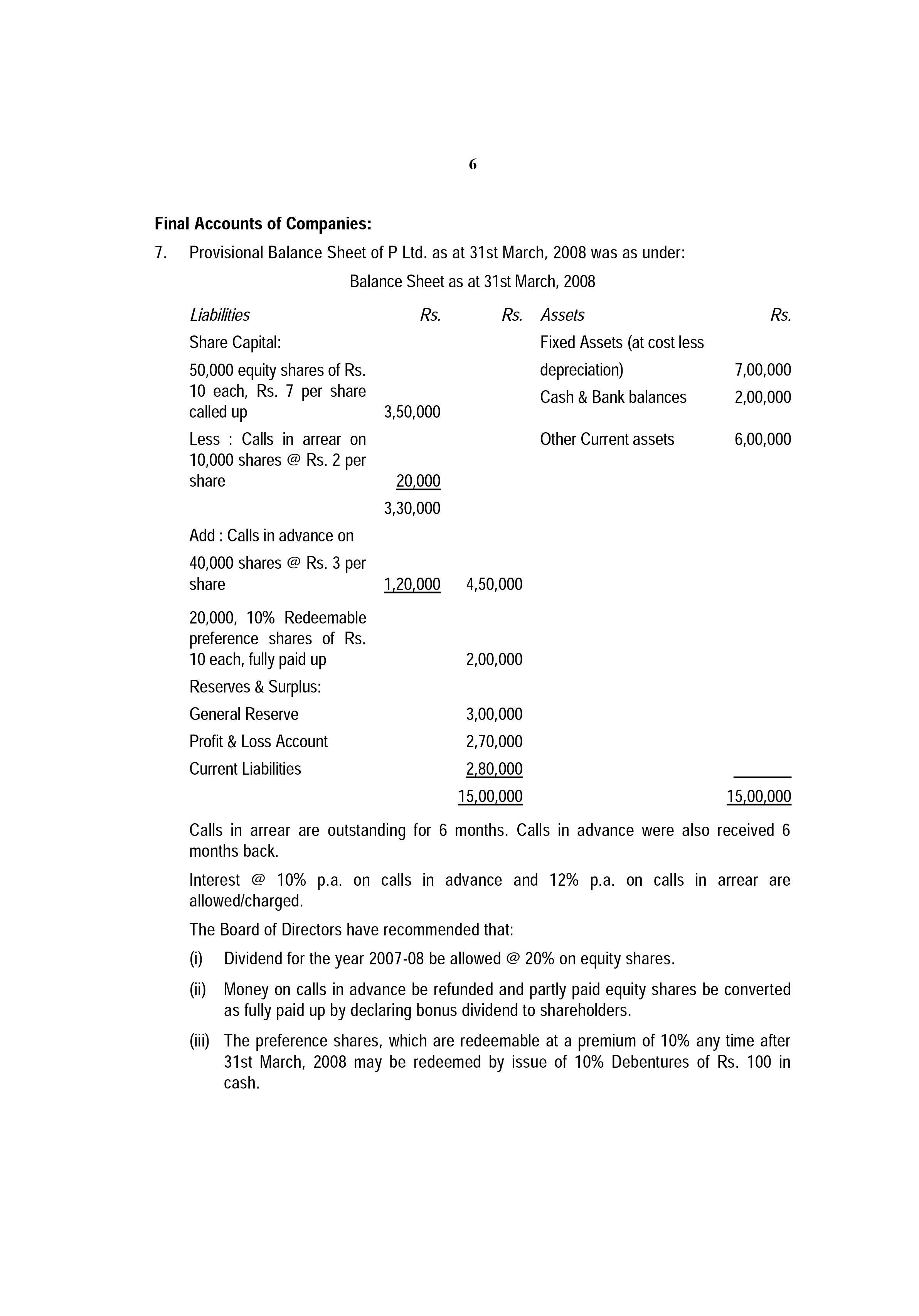

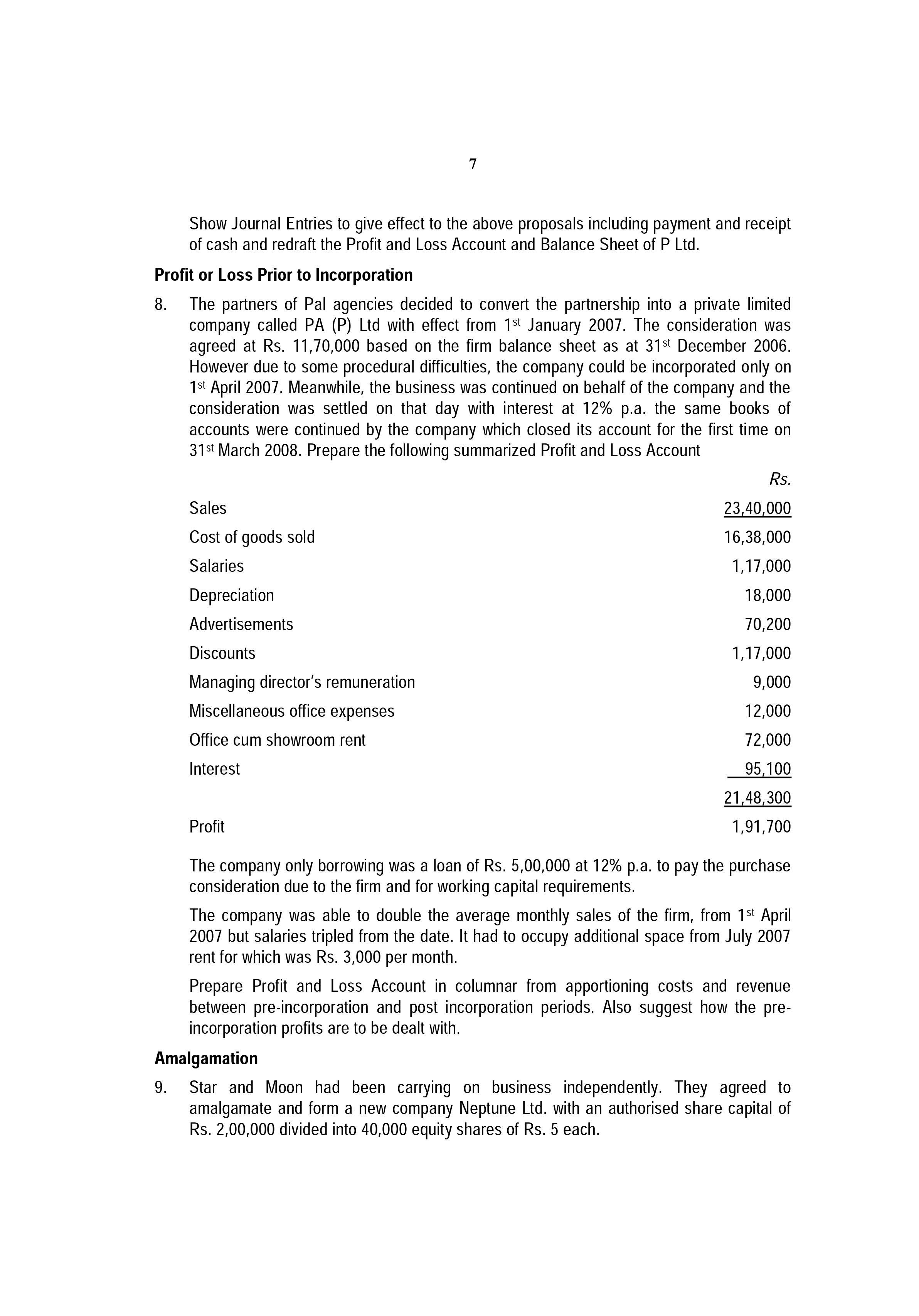

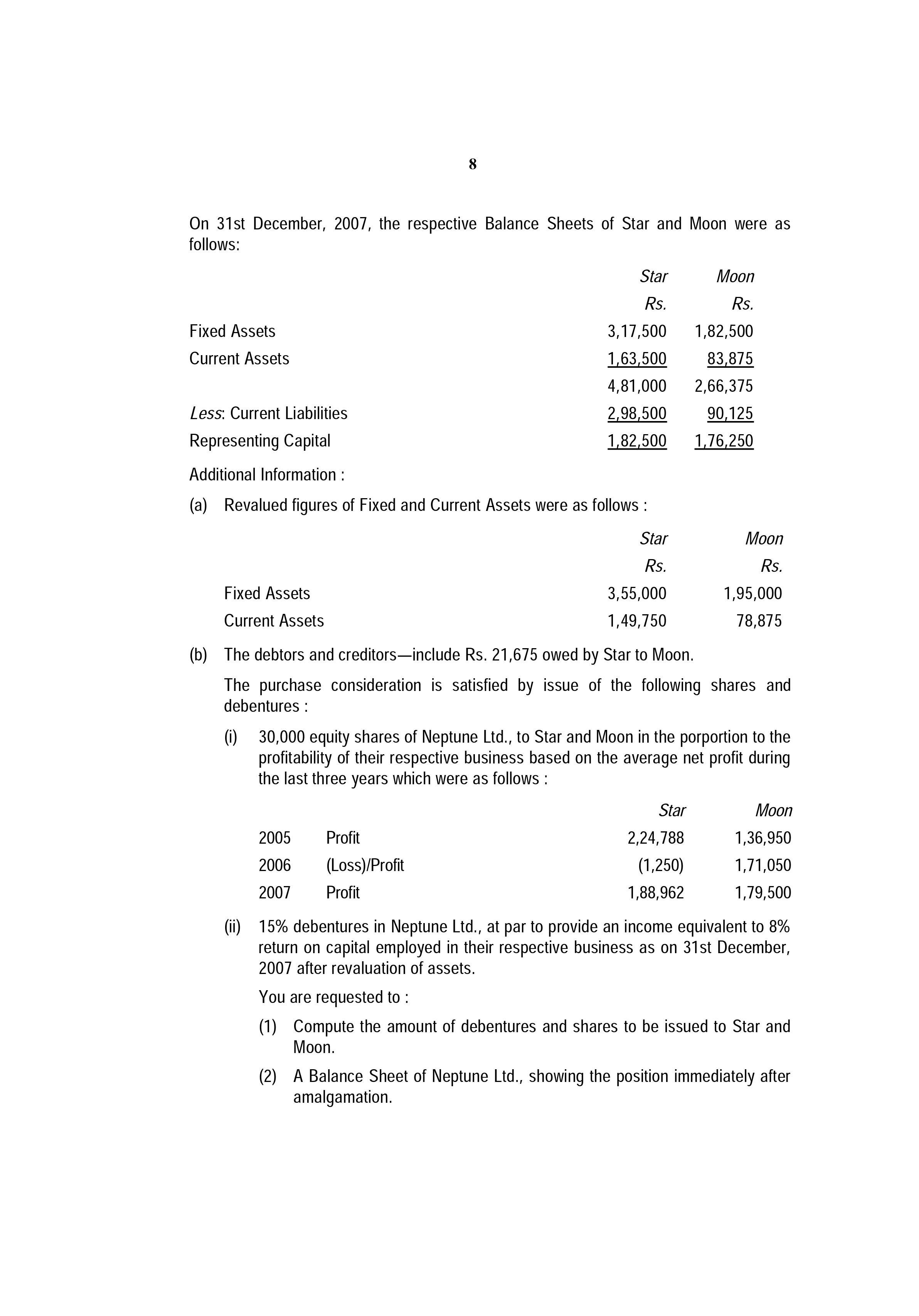

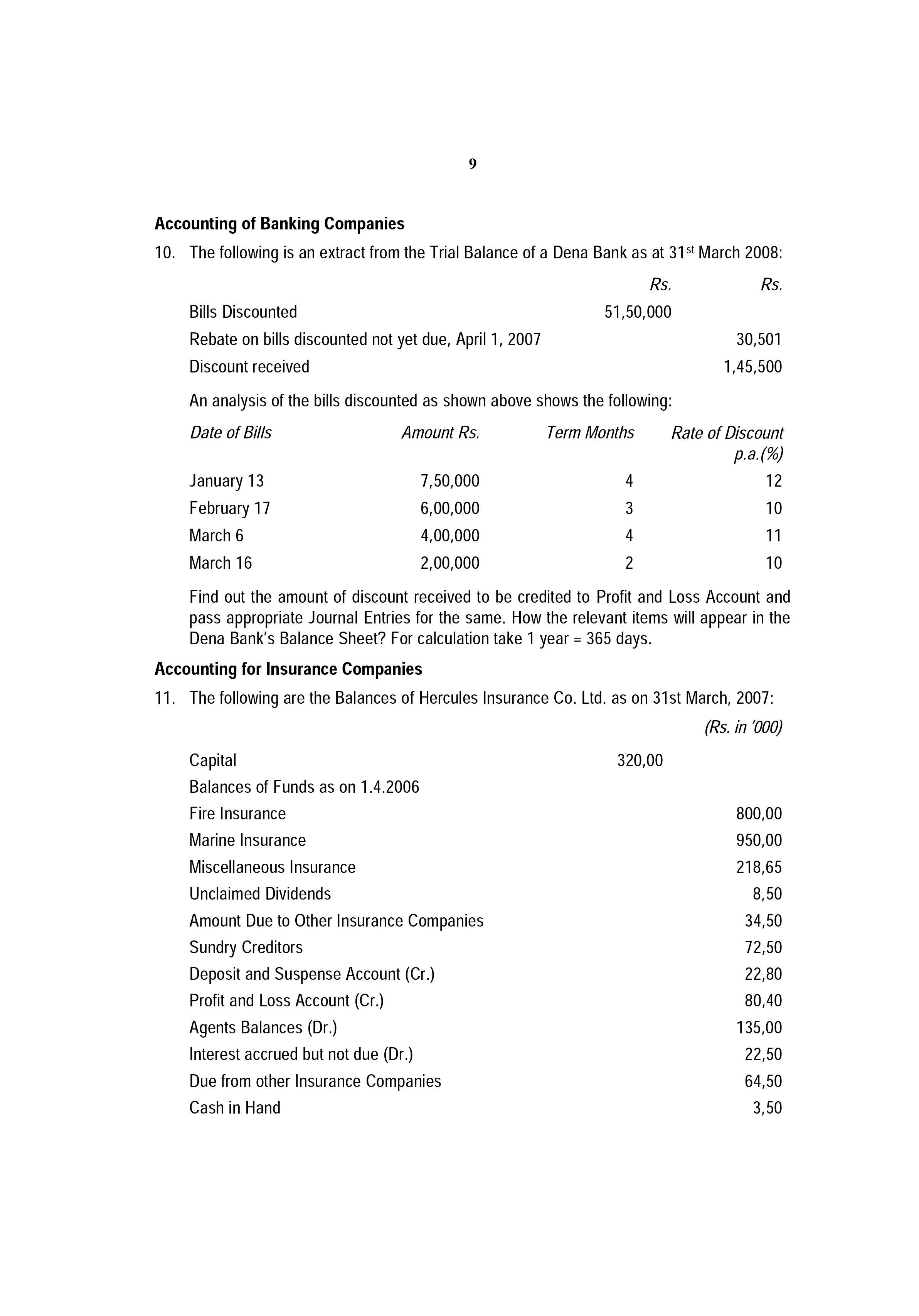

Final Accounts of Companies: 7. Provisional Balance Sheet of P Ltd. as at 31st March, 2008...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

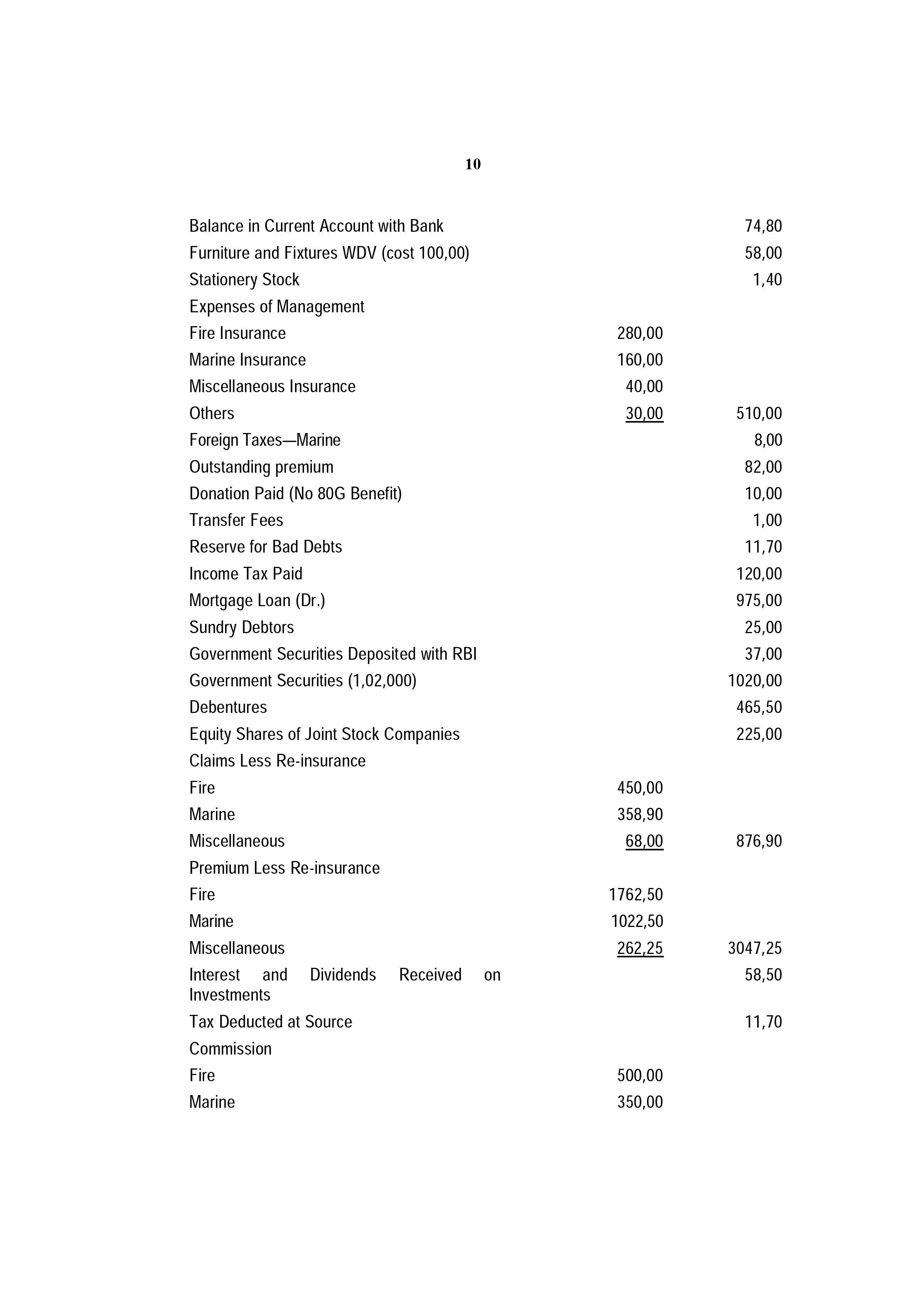

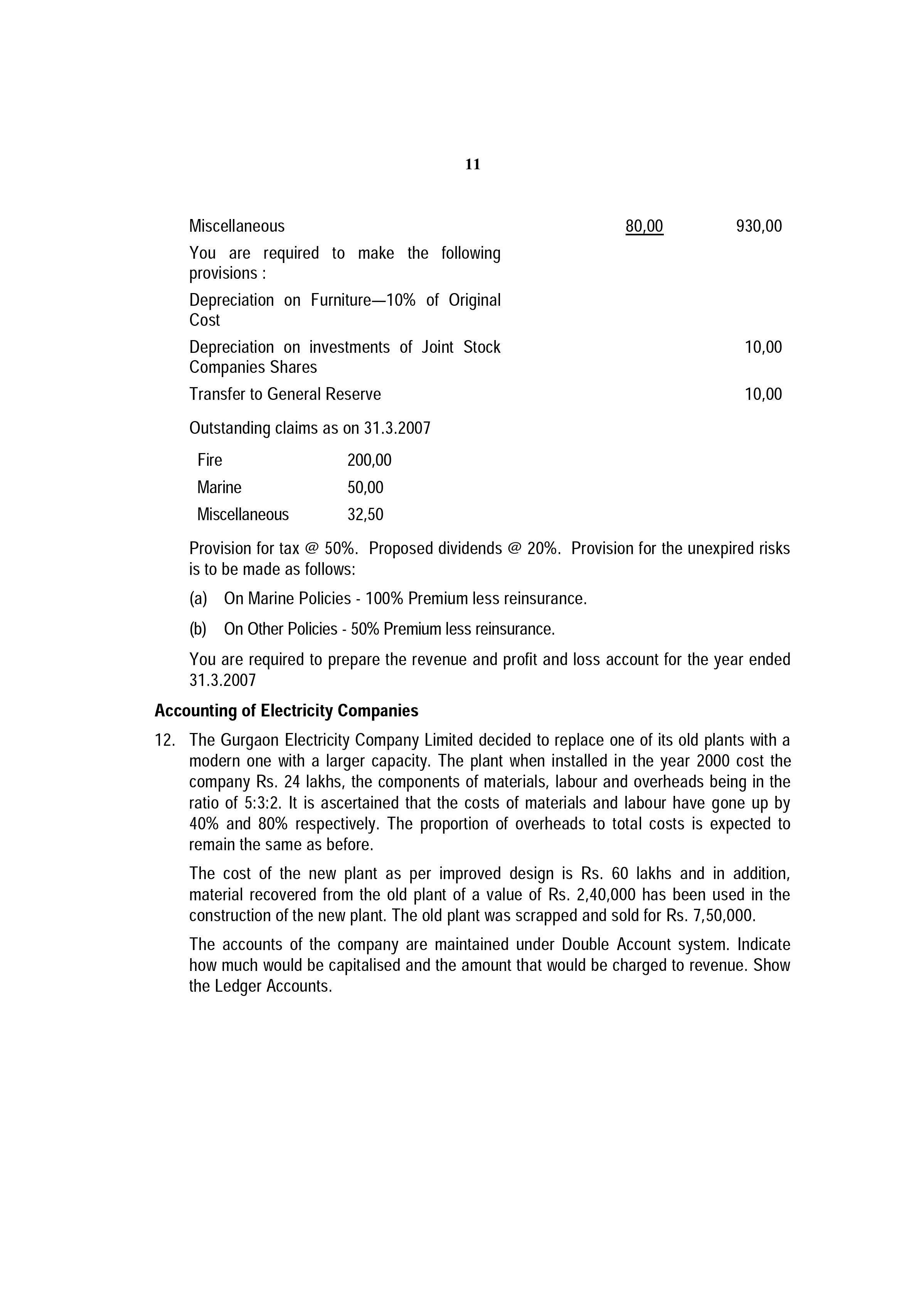

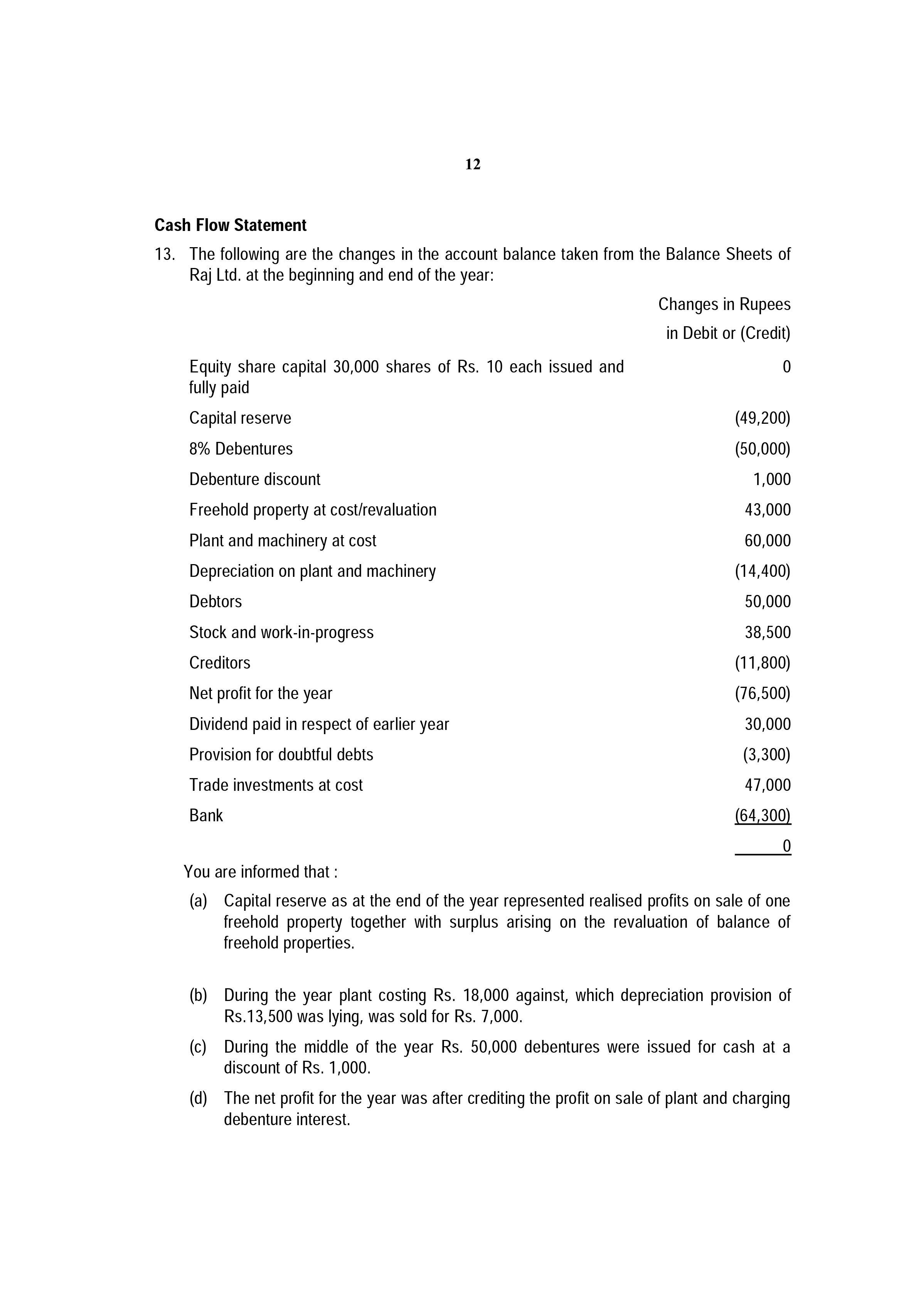

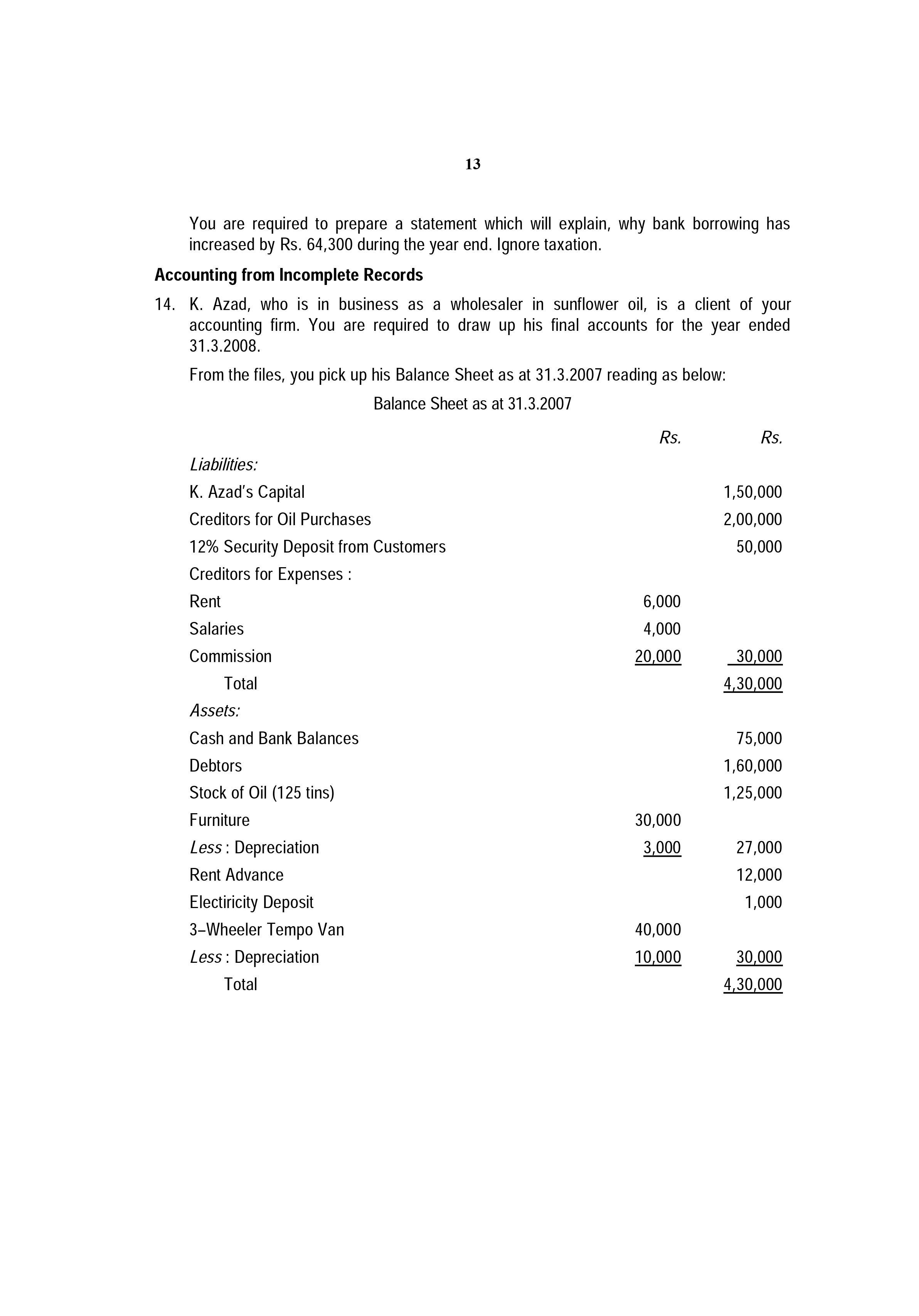

Final Accounts of Companies: 7. Provisional Balance Sheet of P Ltd. as at 31st March, 2008 was as under: Balance Sheet as at 31st March, 2008 Rs. Liabilities Share Capital: 50,000 equity shares of Rs. 10 each, Rs. 7 per share called up Less Calls in arrear on 10,000 shares @ Rs. 2 per share Add: Calls in advance on 40,000 shares @ Rs. 3 share per 20,000, 10% Redeemable preference shares of Rs. 10 each, fully paid up Reserves & Surplus: General Reserve Profit & Loss Account Current Liabilities 3,50,000 20,000 3,30,000 6 1,20,000 Rs. Assets 4,50,000 2,00,000 3,00,000 2,70,000 2,80,000 15,00,000 Fixed Assets (at cost less depreciation) Cash & Bank balances Other Current assets Rs. 7,00,000 2,00,000 6,00,000 15,00,000 Calls in arrear are outstanding for 6 months. Calls in advance were also received 6 months back. Interest @ 10% p.a. on calls in advance and 12% p.a. on calls in arrear are allowed/charged. The Board of Directors have recommended that: (i) Dividend for the year 2007-08 be allowed @ 20% on equity shares. (ii) Money on calls in advance be refunded and partly paid equity shares be converted as fully paid up by declaring bonus dividend to shareholders. (iii) The preference shares, which are redeemable at a premium of 10% any time after 31st March, 2008 may be redeemed by issue of 10% Debentures of Rs. 100 in cash. Show Journal Entries to give effect to the above proposals including payment and receipt of cash and redraft the Profit and Loss Account and Balance Sheet of P Ltd. Profit or Loss Prior to Incorporation 8. The partners of Pal agencies decided to convert the partnership into a private limited company called PA (P) Ltd with effect from 1st January 2007. The consideration was agreed at Rs. 11,70,000 based on the firm balance sheet as at 31st December 2006. However due to some procedural difficulties, the company could be incorporated only on 1st April 2007. Meanwhile, the business was continued on behalf of the company and the consideration was settled on that day with interest at 12% p.a. the same books of accounts were continued by the company which closed its account for the first time on 31st March 2008. Prepare the following summarized Profit and Loss Account Sales Cost of goods sold Salaries Depreciation Advertisements 7 Discounts Managing director's remuneration Miscellaneous office expenses Office cum showroom rent Interest Profit Rs. 23,40,000 16,38,000 1,17,000 18,000 70,200 1,17,000 9,000 12,000 72,000 95,100 21,48,300 1,91,700 The company only borrowing was a loan of Rs. 5,00,000 at 12% p.a. to pay the purchase consideration due to the firm and for working capital requirements. The company was able to double the average monthly sales of the firm, from 1st April 2007 but salaries tripled from the date. It had to occupy additional space from July 2007 rent for which was Rs. 3,000 per month. Prepare Profit and Loss Account in columnar from apportioning costs and revenue between pre-incorporation and post incorporation periods. Also suggest how the pre- incorporation profits are to be dealt with. Amalgamation 9. Star and Moon had been carrying on business independently. They agreed to amalgamate and form a new company Neptune Ltd. with an authorised share capital of Rs. 2,00,000 divided into 40,000 equity shares of Rs. 5 each. On 31st December, 2007, the respective Balance Sheets of Star and Moon were as follows: Fixed Assets Current Assets Fixed Assets Current Assets 8 Less: Current Liabilities Representing Capital Additional Information : (a) Revalued figures of Fixed and Current Assets were as follows: Star Rs. 2005 2006 2007 Profit (Loss)/Profit Profit 3,17,500 1,82,500 1,63,500 83,875 4,81,000 2,66,375 2,98,500 90,125 1,82,500 1,76,250 Star Rs. 3,55,000 1,49,750 Moon Rs. (b) The debtors and creditors-include Rs. 21,675 owed by Star to Moon. The purchase consideration is satisfied by issue of the following shares and debentures : Moon Rs. (i) 30,000 equity shares of Neptune Ltd., to Star and Moon in the porportion to the profitability of their respective business based on the average net profit during the last three years which were as follows: Star 2,24,788 (1,250) 1,88,962 1,95,000 78,875 Moon 1,36,950 1,71,050 1,79,500 (ii) 15% debentures in Neptune Ltd., at par to provide an income equivalent to 8% return on capital employed in their respective business as on 31st December, 2007 after revaluation of assets. You are requested to : (1) Compute the amount of debentures and shares to be issued to Star and Moon. (2) A Balance Sheet of Neptune Ltd., showing the position immediately after amalgamation. Accounting of Banking Companies 10. The following is an extract from the Trial Balance of a Dena Bank as at 31st March 2008: Rs. Rs. 51,50,000 Bills Discounted Rebate on bills discounted not yet due, April 1, 2007 Discount received 9 An analysis of the bills discounted as shown above shows the following: Date of Bills Amount Rs. Term Months January 13 February 17 March 6 March 16 7,50,000 6,00,000 4,00,000 2,00,000 Capital Balances of Funds as on 1.4.2006 Fire Insurance Marine Insurance 4 3 4 2 Find out the amount of discount received to be credited to Profit and Loss Account and pass appropriate Journal Entries for the same. How the relevant items will appear in the Dena Bank's Balance Sheet? For calculation take 1 year = 365 days. Miscellaneous Insurance Unclaimed Dividends Amount Due to Other Insurance Companies Sundry Creditors Deposit and Suspense Account (Cr.) Profit and Loss Account (Cr.) Agents Balances (Dr.) Interest accrued but not due (Dr.) Due from other Insurance Companies Cash in Hand Accounting for Insurance Companies 11. The following are the Balances of Hercules Insurance Co. Ltd. as on 31st March, 2007: (Rs. in '000) 30,501 1,45,500 Rate of Discount p.a.(%) 12 10 11 10 320,00 800,00 950,00 218,65 8,50 34,50 72,50 22,80 80,40 135,00 22,50 64,50 3,50 Balance in Current Account with Bank Furniture and Fixtures WDV (cost 100,00) Stationery Stock Expenses of Management Fire Insurance Marine Insurance Miscellaneous Insurance Others Foreign Taxes-Marine Outstanding premium Donation Paid (No 80G Benefit) Transfer Fees Reserve for Bad Debts Income Tax Paid Mortgage Loan (Dr.) Sundry Debtors Government Securities Deposited with RBI Government Securities (1,02,000) Debentures Equity Shares of Joint Stock Companies Claims Less Re-insurance Fire Marine 10 Miscellaneous Premium Less Re-insurance Fire Marine Miscellaneous Interest and Dividends Received on Investments Tax Deducted at Source Commission Fire Marine 280,00 160,00 40,00 30,00 450,00 358,90 68,00 1762,50 1022,50 262,25 500,00 350,00 74,80 58,00 1,40 510,00 8,00 82,00 10,00 1,00 11,70 120,00 975,00 25,00 37,00 1020,00 465,50 225,00 876,90 3047,25 58,50 11,70 11 Miscellaneous You are required to make the following provisions : Depreciation on Furniture-10% of Original Cost Depreciation on investments of Joint Stock Companies Shares Transfer to General Reserve Outstanding claims as on 31.3.2007 Fire Marine Miscellaneous 200,00 50,00 32,50 80,00 930,00 10,00 10,00 Provision for tax @ 50%. Proposed dividends @ 20%. Provision for the unexpired risks is to be made as follows: (a) On Marine Policies - 100% Premium less reinsurance. (b) On Other Policies - 50% Premium less reinsurance. You are required to prepare the revenue and profit and loss account for the year ended 31.3.2007 Accounting of Electricity Companies 12. The Gurgaon Electricity Company Limited decided to replace one of its old plants with a modern one with a larger capacity. The plant when installed in the year 2000 cost the company Rs. 24 lakhs, the components of materials, labour and overheads being in the ratio of 5:3:2. It is ascertained that the costs of materials and labour have gone up by 40% and 80% respectively. The proportion of overheads to total costs is expected to remain the same as before. The cost of the new plant as per improved design is Rs. 60 lakhs and in addition, material recovered from the old plant of a value of Rs. 2,40,000 has been used in the construction of the new plant. The old plant was scrapped and sold for Rs. 7,50,000. The accounts of the company are maintained under Double Account system. Indicate how much would be capitalised and the amount that would be charged to revenue. Show the Ledger Accounts. 12 Cash Flow Statement 13. The following are the changes in the account balance taken from the Balance Sheets of Raj Ltd. at the beginning and end of the year: Equity share capital 30,000 shares of Rs. 10 each issued and fully paid Capital reserve 8% Debentures Debenture discount Freehold property at cost/revaluation Plant and machinery at cost Depreciation on plant and machinery Debtors Stock and work-in-progress Creditors Net profit for the year Dividend paid in respect of earlier year Provision for doubtful debts Trade investments at cost Bank Changes in Rupees in Debit or (Credit) 0 (49,200) (50,000) 1,000 43,000 60,000 (14,400) 50,000 38,500 (11,800) (76,500) 30,000 (3,300) 47,000 (64,300) 0 You are informed that : (a) Capital reserve as at the end of the year represented realised profits on sale of one freehold property together with surplus arising on the revaluation of balance of freehold properties. (b) During the year plant costing Rs. 18,000 against, which depreciation provision of Rs.13,500 was lying, was sold for Rs. 7,000. (c) During the middle of the year Rs. 50,000 debentures were issued for cash at a discount of Rs. 1,000. (d) The net profit for the year was after crediting the profit on sale of plant and charging debenture interest. You are required to prepare a statement which will explain, why bank borrowing has increased by Rs. 64,300 during the year end. Ignore taxation. Accounting from Incomplete Records 14. K. Azad, who is in business as a wholesaler in sunflower oil, is a client of your accounting firm. You are required to draw up his final accounts for the year ended 31.3.2008. From the files, you pick up his Balance Sheet as at 31.3.2007 reading as below: Balance Sheet as at 31.3.2007 Liabilities: K. Azad's Capital Creditors for Oil Purchases 13 12% Security Deposit from Customers Creditors for Expenses : Rent Salaries Commission Total Assets: Cash and Bank Balances Debtors Stock of Oil (125 tins) Furniture Less: Depreciation Rent Advance Electiricity Deposit 3-Wheeler Tempo Van Less: Depreciation Total Rs. 6,000 4,000 20,000 30,000 3,000 40,000 10,000 Rs. 1,50,000 2,00,000 50,000 30,000 4,30,000 75,000 1,60,000 1,25,000 27,000 12,000 1,000 30,000 4,30,000 A Summary of the rough Cash Book of K. Azad for the year ended 31.3.2008 is as below : Receipts: Cash Sales Collections from Debtors Payments to: Landlord Salaries 14 Cash and Bank Summary Miscellaneous Office Expenses Commission Personal Income-tax Transfer on 1.10.2007 for 12% Fixed Deposit Creditors for Oil Supplies 5,26,500 26,73,500 79,000 48,000 12,000 20,000 50,000 6,00,000 24,00,000 A scrutiny of the other records gives you the following information : (i) During the year oil was purchased at 250 tins per month basis at a unit cost of Rs. 1,000. 5 tins were damaged in transit in respect of which insurance claim has been preferred. The surveyors have since approved the claim at 80%. The damaged ones were sold for Rs. 1,500 which is included in the cash sales. One tin has been used up for personal consumption. Total number of tins sold during the year was 3,000 at a unit price of Rs. 1,750. (ii) Rent until 30.9.2007 was Rs. 6,000 per month and was increased thereafter by Rs. 1,000 per month. Additional advance rent of Rs. 2,000 was paid and this is included in the figure of payments to landlord. (iii) Provide depreciation at 10% and 25% of WDV on furniture and tempo van respectively. (iv) It is further noticed that a customer has paid Rs. 10,000 on 31.3.2008 as security deposit by cash. One of the staff has defalcated. The claim against the Insurance Company is pending. You are requested to prepare final accounts for the year ended 31.3.2008 Introduction to Government Accounts 15. Define the term consolidated fund in context of Government accounting. Final Accounts of Companies: 7. Provisional Balance Sheet of P Ltd. as at 31st March, 2008 was as under: Balance Sheet as at 31st March, 2008 Rs. Liabilities Share Capital: 50,000 equity shares of Rs. 10 each, Rs. 7 per share called up Less Calls in arrear on 10,000 shares @ Rs. 2 per share Add: Calls in advance on 40,000 shares @ Rs. 3 share per 20,000, 10% Redeemable preference shares of Rs. 10 each, fully paid up Reserves & Surplus: General Reserve Profit & Loss Account Current Liabilities 3,50,000 20,000 3,30,000 6 1,20,000 Rs. Assets 4,50,000 2,00,000 3,00,000 2,70,000 2,80,000 15,00,000 Fixed Assets (at cost less depreciation) Cash & Bank balances Other Current assets Rs. 7,00,000 2,00,000 6,00,000 15,00,000 Calls in arrear are outstanding for 6 months. Calls in advance were also received 6 months back. Interest @ 10% p.a. on calls in advance and 12% p.a. on calls in arrear are allowed/charged. The Board of Directors have recommended that: (i) Dividend for the year 2007-08 be allowed @ 20% on equity shares. (ii) Money on calls in advance be refunded and partly paid equity shares be converted as fully paid up by declaring bonus dividend to shareholders. (iii) The preference shares, which are redeemable at a premium of 10% any time after 31st March, 2008 may be redeemed by issue of 10% Debentures of Rs. 100 in cash. Final Accounts of Companies: 7. Provisional Balance Sheet of P Ltd. as at 31st March, 2008 was as under: Balance Sheet as at 31st March, 2008 Rs. Liabilities Share Capital: 50,000 equity shares of Rs. 10 each, Rs. 7 per share called up Less Calls in arrear on 10,000 shares @ Rs. 2 per share Add: Calls in advance on 40,000 shares @ Rs. 3 share per 20,000, 10% Redeemable preference shares of Rs. 10 each, fully paid up Reserves & Surplus: General Reserve Profit & Loss Account Current Liabilities 3,50,000 20,000 3,30,000 6 1,20,000 Rs. Assets 4,50,000 2,00,000 3,00,000 2,70,000 2,80,000 15,00,000 Fixed Assets (at cost less depreciation) Cash & Bank balances Other Current assets Rs. 7,00,000 2,00,000 6,00,000 15,00,000 Calls in arrear are outstanding for 6 months. Calls in advance were also received 6 months back. Interest @ 10% p.a. on calls in advance and 12% p.a. on calls in arrear are allowed/charged. The Board of Directors have recommended that: (i) Dividend for the year 2007-08 be allowed @ 20% on equity shares. (ii) Money on calls in advance be refunded and partly paid equity shares be converted as fully paid up by declaring bonus dividend to shareholders. (iii) The preference shares, which are redeemable at a premium of 10% any time after 31st March, 2008 may be redeemed by issue of 10% Debentures of Rs. 100 in cash. Show Journal Entries to give effect to the above proposals including payment and receipt of cash and redraft the Profit and Loss Account and Balance Sheet of P Ltd. Profit or Loss Prior to Incorporation 8. The partners of Pal agencies decided to convert the partnership into a private limited company called PA (P) Ltd with effect from 1st January 2007. The consideration was agreed at Rs. 11,70,000 based on the firm balance sheet as at 31st December 2006. However due to some procedural difficulties, the company could be incorporated only on 1st April 2007. Meanwhile, the business was continued on behalf of the company and the consideration was settled on that day with interest at 12% p.a. the same books of accounts were continued by the company which closed its account for the first time on 31st March 2008. Prepare the following summarized Profit and Loss Account Sales Cost of goods sold Salaries Depreciation Advertisements 7 Discounts Managing director's remuneration Miscellaneous office expenses Office cum showroom rent Interest Profit Rs. 23,40,000 16,38,000 1,17,000 18,000 70,200 1,17,000 9,000 12,000 72,000 95,100 21,48,300 1,91,700 The company only borrowing was a loan of Rs. 5,00,000 at 12% p.a. to pay the purchase consideration due to the firm and for working capital requirements. The company was able to double the average monthly sales of the firm, from 1st April 2007 but salaries tripled from the date. It had to occupy additional space from July 2007 rent for which was Rs. 3,000 per month. Prepare Profit and Loss Account in columnar from apportioning costs and revenue between pre-incorporation and post incorporation periods. Also suggest how the pre- incorporation profits are to be dealt with. Amalgamation 9. Star and Moon had been carrying on business independently. They agreed to amalgamate and form a new company Neptune Ltd. with an authorised share capital of Rs. 2,00,000 divided into 40,000 equity shares of Rs. 5 each. Show Journal Entries to give effect to the above proposals including payment and receipt of cash and redraft the Profit and Loss Account and Balance Sheet of P Ltd. Profit or Loss Prior to Incorporation 8. The partners of Pal agencies decided to convert the partnership into a private limited company called PA (P) Ltd with effect from 1st January 2007. The consideration was agreed at Rs. 11,70,000 based on the firm balance sheet as at 31st December 2006. However due to some procedural difficulties, the company could be incorporated only on 1st April 2007. Meanwhile, the business was continued on behalf of the company and the consideration was settled on that day with interest at 12% p.a. the same books of accounts were continued by the company which closed its account for the first time on 31st March 2008. Prepare the following summarized Profit and Loss Account Sales Cost of goods sold Salaries Depreciation Advertisements 7 Discounts Managing director's remuneration Miscellaneous office expenses Office cum showroom rent Interest Profit Rs. 23,40,000 16,38,000 1,17,000 18,000 70,200 1,17,000 9,000 12,000 72,000 95,100 21,48,300 1,91,700 The company only borrowing was a loan of Rs. 5,00,000 at 12% p.a. to pay the purchase consideration due to the firm and for working capital requirements. The company was able to double the average monthly sales of the firm, from 1st April 2007 but salaries tripled from the date. It had to occupy additional space from July 2007 rent for which was Rs. 3,000 per month. Prepare Profit and Loss Account in columnar from apportioning costs and revenue between pre-incorporation and post incorporation periods. Also suggest how the pre- incorporation profits are to be dealt with. Amalgamation 9. Star and Moon had been carrying on business independently. They agreed to amalgamate and form a new company Neptune Ltd. with an authorised share capital of Rs. 2,00,000 divided into 40,000 equity shares of Rs. 5 each. On 31st December, 2007, the respective Balance Sheets of Star and Moon were as follows: Fixed Assets Current Assets Fixed Assets Current Assets 8 Less: Current Liabilities Representing Capital Additional Information : (a) Revalued figures of Fixed and Current Assets were as follows: Star Rs. 2005 2006 2007 Profit (Loss)/Profit Profit 3,17,500 1,82,500 1,63,500 83,875 4,81,000 2,66,375 2,98,500 90,125 1,82,500 1,76,250 Star Rs. 3,55,000 1,49,750 Moon Rs. (b) The debtors and creditors-include Rs. 21,675 owed by Star to Moon. The purchase consideration is satisfied by issue of the following shares and debentures : Moon Rs. (i) 30,000 equity shares of Neptune Ltd., to Star and Moon in the porportion to the profitability of their respective business based on the average net profit during the last three years which were as follows: Star 2,24,788 (1,250) 1,88,962 1,95,000 78,875 Moon 1,36,950 1,71,050 1,79,500 (ii) 15% debentures in Neptune Ltd., at par to provide an income equivalent to 8% return on capital employed in their respective business as on 31st December, 2007 after revaluation of assets. You are requested to : (1) Compute the amount of debentures and shares to be issued to Star and Moon. (2) A Balance Sheet of Neptune Ltd., showing the position immediately after amalgamation. On 31st December, 2007, the respective Balance Sheets of Star and Moon were as follows: Fixed Assets Current Assets Fixed Assets Current Assets 8 Less: Current Liabilities Representing Capital Additional Information : (a) Revalued figures of Fixed and Current Assets were as follows: Star Rs. 2005 2006 2007 Profit (Loss)/Profit Profit 3,17,500 1,82,500 1,63,500 83,875 4,81,000 2,66,375 2,98,500 90,125 1,82,500 1,76,250 Star Rs. 3,55,000 1,49,750 Moon Rs. (b) The debtors and creditors-include Rs. 21,675 owed by Star to Moon. The purchase consideration is satisfied by issue of the following shares and debentures : Moon Rs. (i) 30,000 equity shares of Neptune Ltd., to Star and Moon in the porportion to the profitability of their respective business based on the average net profit during the last three years which were as follows: Star 2,24,788 (1,250) 1,88,962 1,95,000 78,875 Moon 1,36,950 1,71,050 1,79,500 (ii) 15% debentures in Neptune Ltd., at par to provide an income equivalent to 8% return on capital employed in their respective business as on 31st December, 2007 after revaluation of assets. You are requested to : (1) Compute the amount of debentures and shares to be issued to Star and Moon. (2) A Balance Sheet of Neptune Ltd., showing the position immediately after amalgamation. Accounting of Banking Companies 10. The following is an extract from the Trial Balance of a Dena Bank as at 31st March 2008: Rs. Rs. 51,50,000 Bills Discounted Rebate on bills discounted not yet due, April 1, 2007 Discount received 9 An analysis of the bills discounted as shown above shows the following: Date of Bills Amount Rs. Term Months January 13 February 17 March 6 March 16 7,50,000 6,00,000 4,00,000 2,00,000 Capital Balances of Funds as on 1.4.2006 Fire Insurance Marine Insurance 4 3 4 2 Find out the amount of discount received to be credited to Profit and Loss Account and pass appropriate Journal Entries for the same. How the relevant items will appear in the Dena Bank's Balance Sheet? For calculation take 1 year = 365 days. Miscellaneous Insurance Unclaimed Dividends Amount Due to Other Insurance Companies Sundry Creditors Deposit and Suspense Account (Cr.) Profit and Loss Account (Cr.) Agents Balances (Dr.) Interest accrued but not due (Dr.) Due from other Insurance Companies Cash in Hand Accounting for Insurance Companies 11. The following are the Balances of Hercules Insurance Co. Ltd. as on 31st March, 2007: (Rs. in '000) 30,501 1,45,500 Rate of Discount p.a.(%) 12 10 11 10 320,00 800,00 950,00 218,65 8,50 34,50 72,50 22,80 80,40 135,00 22,50 64,50 3,50 Accounting of Banking Companies 10. The following is an extract from the Trial Balance of a Dena Bank as at 31st March 2008: Rs. Rs. 51,50,000 Bills Discounted Rebate on bills discounted not yet due, April 1, 2007 Discount received 9 An analysis of the bills discounted as shown above shows the following: Date of Bills Amount Rs. Term Months January 13 February 17 March 6 March 16 7,50,000 6,00,000 4,00,000 2,00,000 Capital Balances of Funds as on 1.4.2006 Fire Insurance Marine Insurance 4 3 4 2 Find out the amount of discount received to be credited to Profit and Loss Account and pass appropriate Journal Entries for the same. How the relevant items will appear in the Dena Bank's Balance Sheet? For calculation take 1 year = 365 days. Miscellaneous Insurance Unclaimed Dividends Amount Due to Other Insurance Companies Sundry Creditors Deposit and Suspense Account (Cr.) Profit and Loss Account (Cr.) Agents Balances (Dr.) Interest accrued but not due (Dr.) Due from other Insurance Companies Cash in Hand Accounting for Insurance Companies 11. The following are the Balances of Hercules Insurance Co. Ltd. as on 31st March, 2007: (Rs. in '000) 30,501 1,45,500 Rate of Discount p.a.(%) 12 10 11 10 320,00 800,00 950,00 218,65 8,50 34,50 72,50 22,80 80,40 135,00 22,50 64,50 3,50 Balance in Current Account with Bank Furniture and Fixtures WDV (cost 100,00) Stationery Stock Expenses of Management Fire Insurance Marine Insurance Miscellaneous Insurance Others Foreign Taxes-Marine Outstanding premium Donation Paid (No 80G Benefit) Transfer Fees Reserve for Bad Debts Income Tax Paid Mortgage Loan (Dr.) Sundry Debtors Government Securities Deposited with RBI Government Securities (1,02,000) Debentures Equity Shares of Joint Stock Companies Claims Less Re-insurance Fire Marine 10 Miscellaneous Premium Less Re-insurance Fire Marine Miscellaneous Interest and Dividends Received on Investments Tax Deducted at Source Commission Fire Marine 280,00 160,00 40,00 30,00 450,00 358,90 68,00 1762,50 1022,50 262,25 500,00 350,00 74,80 58,00 1,40 510,00 8,00 82,00 10,00 1,00 11,70 120,00 975,00 25,00 37,00 1020,00 465,50 225,00 876,90 3047,25 58,50 11,70 Balance in Current Account with Bank Furniture and Fixtures WDV (cost 100,00) Stationery Stock Expenses of Management Fire Insurance Marine Insurance Miscellaneous Insurance Others Foreign Taxes-Marine Outstanding premium Donation Paid (No 80G Benefit) Transfer Fees Reserve for Bad Debts Income Tax Paid Mortgage Loan (Dr.) Sundry Debtors Government Securities Deposited with RBI Government Securities (1,02,000) Debentures Equity Shares of Joint Stock Companies Claims Less Re-insurance Fire Marine 10 Miscellaneous Premium Less Re-insurance Fire Marine Miscellaneous Interest and Dividends Received on Investments Tax Deducted at Source Commission Fire Marine 280,00 160,00 40,00 30,00 450,00 358,90 68,00 1762,50 1022,50 262,25 500,00 350,00 74,80 58,00 1,40 510,00 8,00 82,00 10,00 1,00 11,70 120,00 975,00 25,00 37,00 1020,00 465,50 225,00 876,90 3047,25 58,50 11,70 11 Miscellaneous You are required to make the following provisions : Depreciation on Furniture-10% of Original Cost Depreciation on investments of Joint Stock Companies Shares Transfer to General Reserve Outstanding claims as on 31.3.2007 Fire Marine Miscellaneous 200,00 50,00 32,50 80,00 930,00 10,00 10,00 Provision for tax @ 50%. Proposed dividends @ 20%. Provision for the unexpired risks is to be made as follows: (a) On Marine Policies - 100% Premium less reinsurance. (b) On Other Policies - 50% Premium less reinsurance. You are required to prepare the revenue and profit and loss account for the year ended 31.3.2007 Accounting of Electricity Companies 12. The Gurgaon Electricity Company Limited decided to replace one of its old plants with a modern one with a larger capacity. The plant when installed in the year 2000 cost the company Rs. 24 lakhs, the components of materials, labour and overheads being in the ratio of 5:3:2. It is ascertained that the costs of materials and labour have gone up by 40% and 80% respectively. The proportion of overheads to total costs is expected to remain the same as before. The cost of the new plant as per improved design is Rs. 60 lakhs and in addition, material recovered from the old plant of a value of Rs. 2,40,000 has been used in the construction of the new plant. The old plant was scrapped and sold for Rs. 7,50,000. The accounts of the company are maintained under Double Account system. Indicate how much would be capitalised and the amount that would be charged to revenue. Show the Ledger Accounts. 11 Miscellaneous You are required to make the following provisions : Depreciation on Furniture-10% of Original Cost Depreciation on investments of Joint Stock Companies Shares Transfer to General Reserve Outstanding claims as on 31.3.2007 Fire Marine Miscellaneous 200,00 50,00 32,50 80,00 930,00 10,00 10,00 Provision for tax @ 50%. Proposed dividends @ 20%. Provision for the unexpired risks is to be made as follows: (a) On Marine Policies - 100% Premium less reinsurance. (b) On Other Policies - 50% Premium less reinsurance. You are required to prepare the revenue and profit and loss account for the year ended 31.3.2007 Accounting of Electricity Companies 12. The Gurgaon Electricity Company Limited decided to replace one of its old plants with a modern one with a larger capacity. The plant when installed in the year 2000 cost the company Rs. 24 lakhs, the components of materials, labour and overheads being in the ratio of 5:3:2. It is ascertained that the costs of materials and labour have gone up by 40% and 80% respectively. The proportion of overheads to total costs is expected to remain the same as before. The cost of the new plant as per improved design is Rs. 60 lakhs and in addition, material recovered from the old plant of a value of Rs. 2,40,000 has been used in the construction of the new plant. The old plant was scrapped and sold for Rs. 7,50,000. The accounts of the company are maintained under Double Account system. Indicate how much would be capitalised and the amount that would be charged to revenue. Show the Ledger Accounts. 12 Cash Flow Statement 13. The following are the changes in the account balance taken from the Balance Sheets of Raj Ltd. at the beginning and end of the year: Equity share capital 30,000 shares of Rs. 10 each issued and fully paid Capital reserve 8% Debentures Debenture discount Freehold property at cost/revaluation Plant and machinery at cost Depreciation on plant and machinery Debtors Stock and work-in-progress Creditors Net profit for the year Dividend paid in respect of earlier year Provision for doubtful debts Trade investments at cost Bank Changes in Rupees in Debit or (Credit) 0 (49,200) (50,000) 1,000 43,000 60,000 (14,400) 50,000 38,500 (11,800) (76,500) 30,000 (3,300) 47,000 (64,300) 0 You are informed that : (a) Capital reserve as at the end of the year represented realised profits on sale of one freehold property together with surplus arising on the revaluation of balance of freehold properties. (b) During the year plant costing Rs. 18,000 against, which depreciation provision of Rs.13,500 was lying, was sold for Rs. 7,000. (c) During the middle of the year Rs. 50,000 debentures were issued for cash at a discount of Rs. 1,000. (d) The net profit for the year was after crediting the profit on sale of plant and charging debenture interest. 12 Cash Flow Statement 13. The following are the changes in the account balance taken from the Balance Sheets of Raj Ltd. at the beginning and end of the year: Equity share capital 30,000 shares of Rs. 10 each issued and fully paid Capital reserve 8% Debentures Debenture discount Freehold property at cost/revaluation Plant and machinery at cost Depreciation on plant and machinery Debtors Stock and work-in-progress Creditors Net profit for the year Dividend paid in respect of earlier year Provision for doubtful debts Trade investments at cost Bank Changes in Rupees in Debit or (Credit) 0 (49,200) (50,000) 1,000 43,000 60,000 (14,400) 50,000 38,500 (11,800) (76,500) 30,000 (3,300) 47,000 (64,300) 0 You are informed that : (a) Capital reserve as at the end of the year represented realised profits on sale of one freehold property together with surplus arising on the revaluation of balance of freehold properties. (b) During the year plant costing Rs. 18,000 against, which depreciation provision of Rs.13,500 was lying, was sold for Rs. 7,000. (c) During the middle of the year Rs. 50,000 debentures were issued for cash at a discount of Rs. 1,000. (d) The net profit for the year was after crediting the profit on sale of plant and charging debenture interest. You are required to prepare a statement which will explain, why bank borrowing has increased by Rs. 64,300 during the year end. Ignore taxation. Accounting from Incomplete Records 14. K. Azad, who is in business as a wholesaler in sunflower oil, is a client of your accounting firm. You are required to draw up his final accounts for the year ended 31.3.2008. From the files, you pick up his Balance Sheet as at 31.3.2007 reading as below: Balance Sheet as at 31.3.2007 Liabilities: K. Azad's Capital Creditors for Oil Purchases 13 12% Security Deposit from Customers Creditors for Expenses : Rent Salaries Commission Total Assets: Cash and Bank Balances Debtors Stock of Oil (125 tins) Furniture Less: Depreciation Rent Advance Electiricity Deposit 3-Wheeler Tempo Van Less: Depreciation Total Rs. 6,000 4,000 20,000 30,000 3,000 40,000 10,000 Rs. 1,50,000 2,00,000 50,000 30,000 4,30,000 75,000 1,60,000 1,25,000 27,000 12,000 1,000 30,000 4,30,000 You are required to prepare a statement which will explain, why bank borrowing has increased by Rs. 64,300 during the year end. Ignore taxation. Accounting from Incomplete Records 14. K. Azad, who is in business as a wholesaler in sunflower oil, is a client of your accounting firm. You are required to draw up his final accounts for the year ended 31.3.2008. From the files, you pick up his Balance Sheet as at 31.3.2007 reading as below: Balance Sheet as at 31.3.2007 Liabilities: K. Azad's Capital Creditors for Oil Purchases 13 12% Security Deposit from Customers Creditors for Expenses : Rent Salaries Commission Total Assets: Cash and Bank Balances Debtors Stock of Oil (125 tins) Furniture Less: Depreciation Rent Advance Electiricity Deposit 3-Wheeler Tempo Van Less: Depreciation Total Rs. 6,000 4,000 20,000 30,000 3,000 40,000 10,000 Rs. 1,50,000 2,00,000 50,000 30,000 4,30,000 75,000 1,60,000 1,25,000 27,000 12,000 1,000 30,000 4,30,000 A Summary of the rough Cash Book of K. Azad for the year ended 31.3.2008 is as below : Receipts: Cash Sales Collections from Debtors Payments to: Landlord Salaries 14 Cash and Bank Summary Miscellaneous Office Expenses Commission Personal Income-tax Transfer on 1.10.2007 for 12% Fixed Deposit Creditors for Oil Supplies 5,26,500 26,73,500 79,000 48,000 12,000 20,000 50,000 6,00,000 24,00,000 A scrutiny of the other records gives you the following information : (i) During the year oil was purchased at 250 tins per month basis at a unit cost of Rs. 1,000. 5 tins were damaged in transit in respect of which insurance claim has been preferred. The surveyors have since approved the claim at 80%. The damaged ones were sold for Rs. 1,500 which is included in the cash sales. One tin has been used up for personal consumption. Total number of tins sold during the year was 3,000 at a unit price of Rs. 1,750. (ii) Rent until 30.9.2007 was Rs. 6,000 per month and was increased thereafter by Rs. 1,000 per month. Additional advance rent of Rs. 2,000 was paid and this is included in the figure of payments to landlord. (iii) Provide depreciation at 10% and 25% of WDV on furniture and tempo van respectively. (iv) It is further noticed that a customer has paid Rs. 10,000 on 31.3.2008 as security deposit by cash. One of the staff has defalcated. The claim against the Insurance Company is pending. You are requested to prepare final accounts for the year ended 31.3.2008 Introduction to Government Accounts 15. Define the term consolidated fund in context of Government accounting. A Summary of the rough Cash Book of K. Azad for the year ended 31.3.2008 is as below : Receipts: Cash Sales Collections from Debtors Payments to: Landlord Salaries 14 Cash and Bank Summary Miscellaneous Office Expenses Commission Personal Income-tax Transfer on 1.10.2007 for 12% Fixed Deposit Creditors for Oil Supplies 5,26,500 26,73,500 79,000 48,000 12,000 20,000 50,000 6,00,000 24,00,000 A scrutiny of the other records gives you the following information : (i) During the year oil was purchased at 250 tins per month basis at a unit cost of Rs. 1,000. 5 tins were damaged in transit in respect of which insurance claim has been preferred. The surveyors have since approved the claim at 80%. The damaged ones were sold for Rs. 1,500 which is included in the cash sales. One tin has been used up for personal consumption. Total number of tins sold during the year was 3,000 at a unit price of Rs. 1,750. (ii) Rent until 30.9.2007 was Rs. 6,000 per month and was increased thereafter by Rs. 1,000 per month. Additional advance rent of Rs. 2,000 was paid and this is included in the figure of payments to landlord. (iii) Provide depreciation at 10% and 25% of WDV on furniture and tempo van respectively. (iv) It is further noticed that a customer has paid Rs. 10,000 on 31.3.2008 as security deposit by cash. One of the staff has defalcated. The claim against the Insurance Company is pending. You are requested to prepare final accounts for the year ended 31.3.2008 Introduction to Government Accounts 15. Define the term consolidated fund in context of Government accounting.

Expert Answer:

Related Book For

Auditing a risk based approach to conducting a quality audit

ISBN: 978-1133939153

9th edition

Authors: Karla Johnstone, Audrey Gramling, Larry Rittenberg

Posted Date:

Students also viewed these accounting questions

-

Read the case study "Southwest Airlines," found in Part 2 of your textbook. Review the "Guide to Case Analysis" found on pp. CA1 - CA11 of your textbook. (This guide follows the last case in the...

-

Balance sheet of Company Jolie dated 31.12.2017 showed the following accounte a) tangible fixed assets (building) 40 000 b) intangible fixed assets (a trademark) 5 000 e) trade receivables 20 000 d)...

-

The Crazy Eddie fraud may appear smaller and gentler than the massive billion-dollar frauds exposed in recent times, such as Bernie Madoffs Ponzi scheme, frauds in the subprime mortgage market, the...

-

Prove Theorem 9.7.1. Theorem 9.7.1 Principal Axes Theorem for ft3 Let ax2 + by2 + cz2 + 2dxy + 2exz + 2fyz + gx + hy + iz + j = 0 be the equation of a quadric Q, and let xTAx = ax2 + by2 + cz2 + 2dxy...

-

In January 2003, Gary Ryder and Washington Mutual Bank, F. A., executed a note in which Ryder promised to pay $2,450,000, plus interest at a rate that could vary from month to month. The amount of...

-

A responsibility center in which a manager is responsible for revenues, costs, and investments is a(n) a. cost center. b. profit center. c. revenue center. d. investment center.

-

With reference to Exercise 11.3, express \(90 \%\) limits of prediction for the tearing strength in terms of the temperature \(x_{0}\). Choosing suitable values of \(x_{0}\), sketch graphs of the...

-

City Copy Center sells laser printers and supplies. Assume City Copy Center started the year with 100 containers of ink (average cost of $8.30 each, FIFO cost of $8.40 each, LIFO cost of $8.10 each)....

-

Electric potential is measured at points A = ( - 2 , - 3 ) cm and B = ( 5 , - 4 ) cm . The measurements are VA = 9 V and VB = 3 6 V , respectively. The electric field points exclusively along the x -...

-

During 2020, you were hired as the Chief Financial Officer for MC Travel Inc., a fairly young travel company that is growing quickly. A key accounting staff member has prepared the financial...

-

National Inc, manufactures two models of CMD that can be used as cell phones, MPX, and digital camcorders. Model High F Great P Annual Sales in Units 10, 200 16, 200 National uses a volume-based...

-

Trading online increasingly involves developing multichannel strategies. Give three examples of potential channel conflicts that might arise from using the Internet. Illustrate your answer with...

-

Setting long-term strategic objectives for a website is unrealistic since the rate of change in the marketplace is so rapid. Discuss.

-

Summarise how each of the micro-environment factors may directly drive the content and services provided by a website.

-

What is the purpose of a digital marketing audit? What should it involve?

-

Competition is intensified when trading online. Discuss the extent to which you feel this assertion is true.

-

A business has a policy of capitalizing expenditure over 500. You are working on the accounting records of a business for the year ended 31 March 2019. A machine was acquired on 1 April 2016. The...

-

Linda Lopez opened a beauty studio, Lindas Salon, on January 2, 2011. The salon also sells beauty supplies. In January 2012, Lopez realized she had never filed any tax reports for her business and...

-

The audit of GolfDay Company, a manufacturer of bicycle racks and golf carts, is almost finished. Krista Heiss is the most experienced auditor on this audit and is in charge of performing final...

-

Provide examples of the subject matter of an assurance engagement.

-

Locate and read the article listed below and answer the following questions. Nigrini, M., and L. Mittermaier. 1997. The Use of Benfords Law as an Aid in Analytical Procedures. Auditing: A Journal of...

-

Who is currently in your own network that you could use for prospecting? How might you add to your network?

-

Pick any three of the sources of prospects discussed in the chapter and pick a product or service you like. Develop several ideas for how you would use each source to locate leads for the product or...

-

Why do you think a salesperson might experience call reluctance? How can it be overcome?

Study smarter with the SolutionInn App