Question: Finance question in the picture. Problem 3 (40 points). Suppose there are two uncorrelated risky assets A and B. Asset A has volatility 20% and

Finance question in the picture.

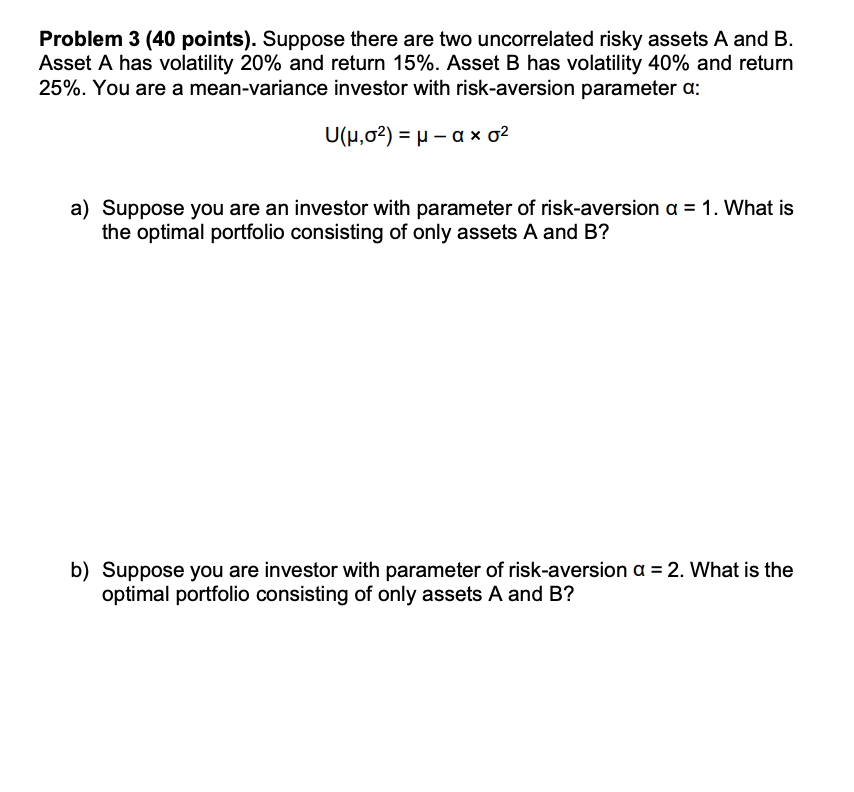

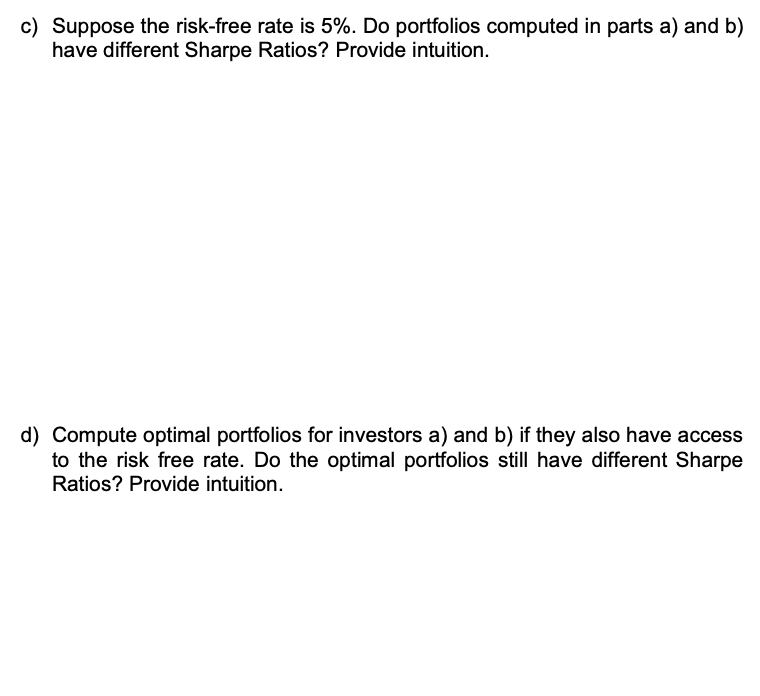

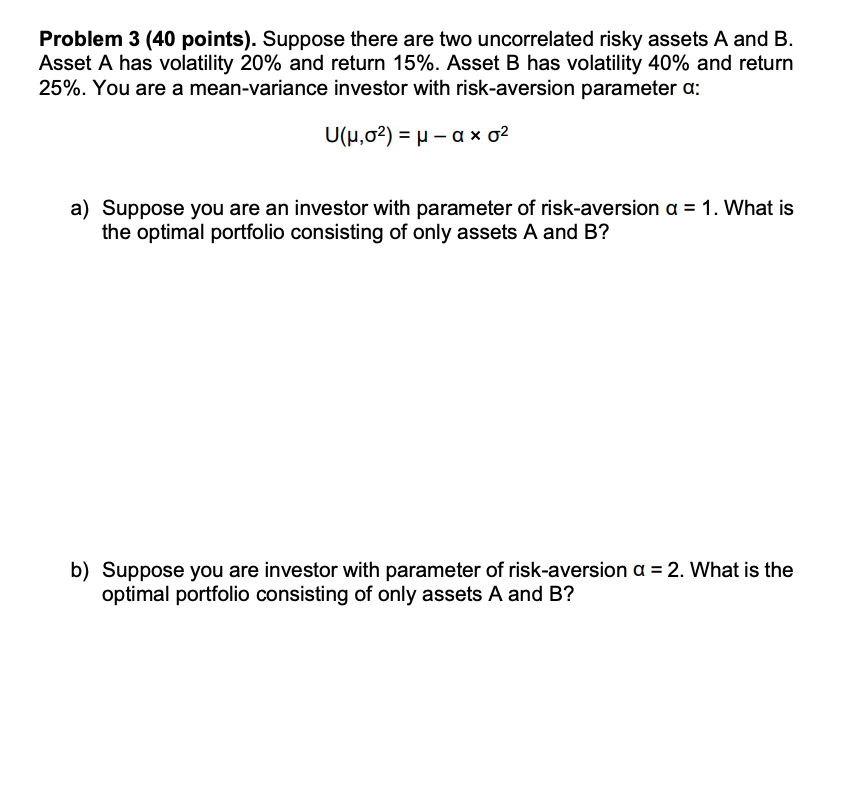

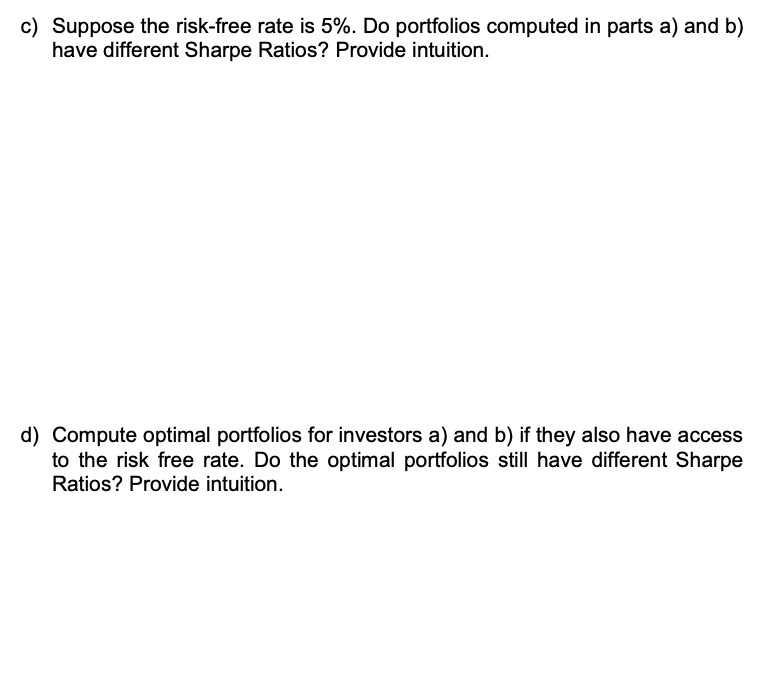

Problem 3 (40 points). Suppose there are two uncorrelated risky assets A and B. Asset A has volatility 20% and return 15%. Asset B has volatility 40% and return 25%. You are a mean-variance investor with risk-aversion parameter a: U(u.02) = u a x 02 a) Suppose you are an investor with parameter of risk-aversion o = 1. What is the optimal portfolio oonsisting of only assets A and B? b) Suppose you are investor with parameter of risk-aversion Cl = 2. What is the optimal portfolio consisting of only assets A and B? o) Suppose the risk-free rate is 5%. Do portfolios oomputed in parts a} and b) have different Sharpe Ratios? Provide intuition. d) Compute optimal portfolios for investors a) and b) if they also have access to the risk free rate. Do the optimal portfolios still have different Sharpe Ratios? Provide intuition

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts