Question: Financial econometrics multiple choice questions Question 12 Consider the process y,=3y- 1-2y.-2+u,, where u, is white noise. Consider the following statements about the stationarity of

Financial econometrics multiple choice questions

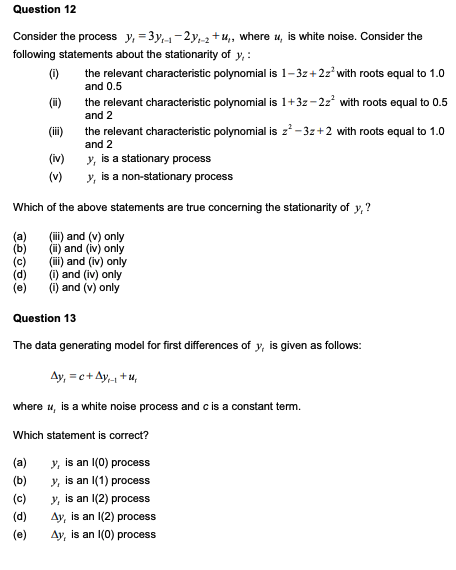

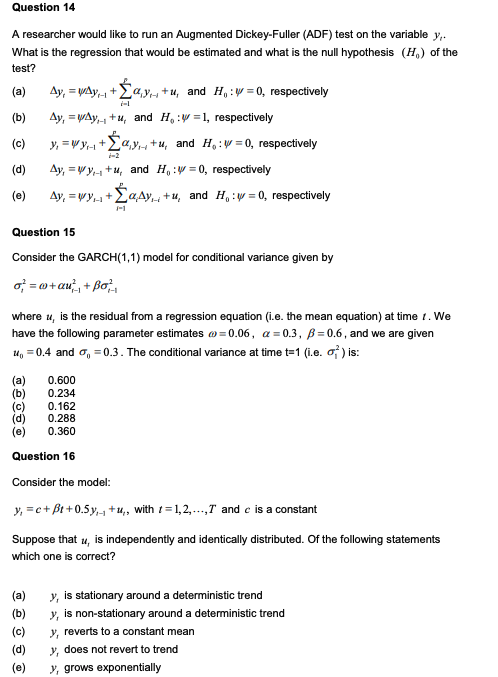

Question 12 Consider the process y,=3y- 1-2y.-2+u,, where u, is white noise. Consider the following statements about the stationarity of y,: ( the relevant characteristic polynomial is 132+2zwith roots equal to 1.0 and 0.5 () the relevant characteristic polynomial is 1+322zwith roots equal to 0.5 and 2 the relevant characteristic polynomial is z? -3z+2 with roots equal to 1.0 and 2 (iv) y, is a stationary process (v) y, is a non-stationary process O@OGO Which of the above statements are true concerning the stationarity of y;? (ii) and (v) only (i) and (iv) only (ii) and (iv) only (i) and (iv) only (i) and (v) only Question 13 The data generating model for first differences of y, is given as follows: Ay, =c+Ay-+u where u, is a white noise process and c is a constant term. Which statement is correct? (a) (b) (c) (d) (e) y, is an I(0) process y, is an (1) process y, is an I(2) process Ay, is an I(2) process Ay, is an I(0) process Question 14 A researcher would like to run an Augmented Dickey-Fuller (ADF) test on the variable y,. What is the regression that would be estimated and what is the null hypothesis (H) of the test? (a) Ay, = wdy-+ayu tu, and H, :v = 0, respectively (b) Ay, EwAy- +u, and H, V = 1, respectively (c) y; =WY + ay. +u, and H,: v= 0, respectively (d) Ay, =V y2 +u, and H, y = 0, respectively (e) Ay, =wy.+q,ay, +u, and He: y = 0, respectively Question 15 Consider the GARCH(1,1) model for conditional variance given by o* = 0+au+Bo- where u, is the residual from a regression equation (i.e. the mean equation) at time 1. We have the following parameter estimates o=0.06, C =0.3, B = 0.6, and we are given Ug = 0.4 and 9, = 0.3. The conditional variance at time t=1 (i.e. o) is: (a) (c) 0.600 0.234 0.162 0.288 0.360 Question 16 Consider the model: y, =c+B++0.5y+u, with 1 =1,2,..,T and is a constant Suppose that u, is independently and identically distributed. Of the following statements which one is correct? (a) (b) (c) (d) y, is stationary around a deterministic trend y, is non-stationary around a deterministic trend y, reverts to a constant mean y, does not revert to trend y, grows exponentially

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts