Question: Financial Institutions Management (8th Edition) SAUNDERS & CORNET Chapter 8, Problem 19QP THE ANSEWR C IS NOT CORRECT, CAN YOU FIX IT OR IF IT

Financial Institutions Management (8th Edition) SAUNDERS & CORNET

Financial Institutions Management (8th Edition) SAUNDERS & CORNET

Chapter 8, Problem 19QP

THE ANSEWR C IS NOT CORRECT, CAN YOU FIX IT OR IF IT IS CORRECT EXPLAIN ME THE RESULT.

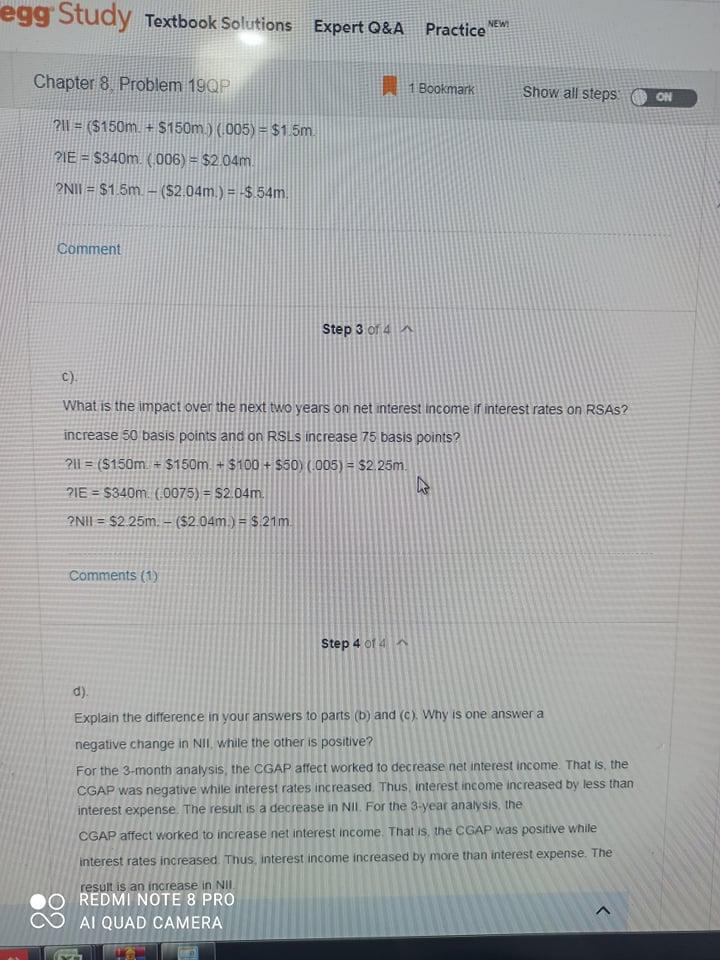

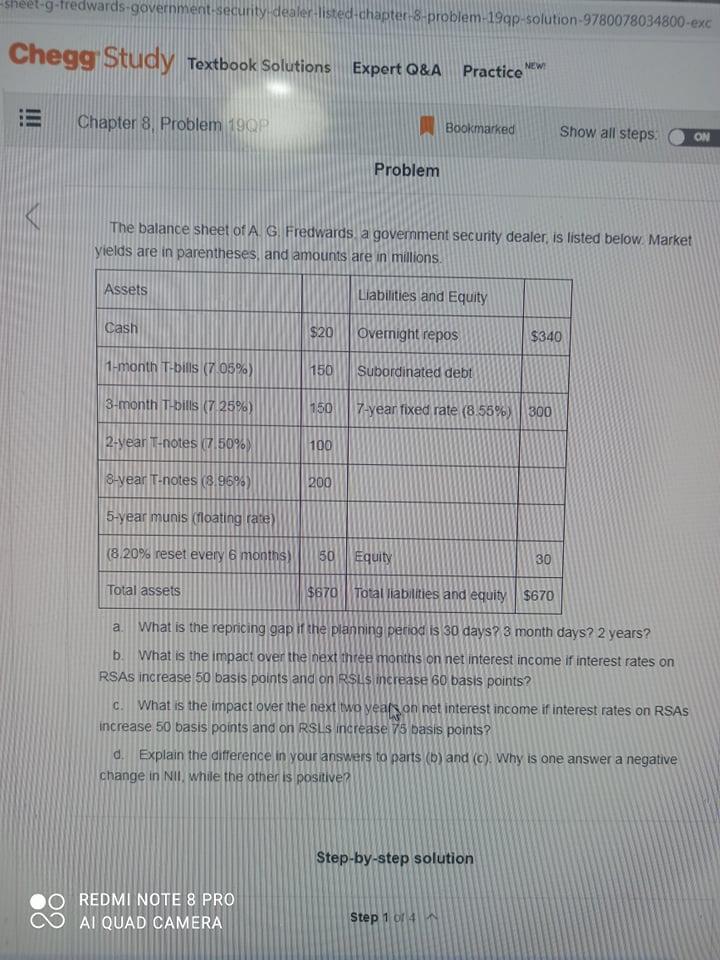

egg Study Textbook Solutions Expert Q&A Practice NEW Chapter 8. Problem 19QP 1 Bookmark Show all steps ON 211 = ($150m. + $150m. /.005) = $1.5m. ?IE = $340m. (006) = $2.04m. 2NII = $1.5m. - ($2.04m.) = $ 54m Comment Step 3 of 4 C) What is the impact over the next two years on net interest income if interest rates on RSAS? increase 50 basis points and on RSLS increase 75 basis points? 211 = ($150m. + $150m. + $100 + $50 (005) = $2.25m. ?IE = $340m. (0075) = $2.04m. ?NII = $2 25m. - ($2.04m.) = $.21m Comments (1) Step 4 of 4 d) Explain the difference in your answers to parts (b) and (c) Why is one answer a negative change in NII while the other is positive? For the 3-month analysis, the CGAP affect worked to decrease net interest income. That is the CGAP was negative while interest rates increased. Thus interest income increased by less than interest expense. The result is a decrease in NII. For the 3-year analysis, the CGAP affect worked to increase net interest income. That is, the CGAP was positive while interest rates increased. Thus, interest income increased by more than interest expense. The result is an increase in NII REDMI NOTE 8 PRO AI QUAD CAMERA sheet-g-fredwards-government security dealer listed chapter 8-problem-199p-solution-9780078034800-exc Chegg Study Textbook Solutions Export O&A Practice mem E Chapter 8 Problem 190 Bookmarked Show all steps ON Problem The balance sheet of A G Fredwards a government security dealer, is listed below Market yields are in parentheses, and amounts are in millions Assets Liabilities and Equity Cash $20 Overnight repos $340 1-month T-bills (705%) 150 Subordinated debt 3-month Thbills (7 25%) 150 7-year fixed rate (8.55%) 300 2-year T-notes (50%) 100 8-year T-notes (8.96%) 200 5-year munis (floating rate) (8.20% reset every 6 months) 50 Equity 30 Total assets $670 Total liabilities and equity $670 a What is the repricing gap if the planning period is 30 days? 3 month days? 2 years? b. What is the impact over the next three months on net interest income if interest rates on RSAs increase 50 basis points and on R$Ls increase 60 basis points? C. What is the impact over the next two years on net interest income if interest rates on RSAS increase 50 basis points and on RSLs increase v5 basis points? d. Explain the difference in your answers to parts (6) and (c). Why is one answer a negative change in NII, while the other is positive? Step-by-step solution O REDMI NOTE 8 PRO AI QUAD CAMERA Step 1 0141

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts