Question: financial mathematics problem Problem 4. Define by Pr the price of the European put option in the GBM model as the function of x=the value

financial mathematics problem

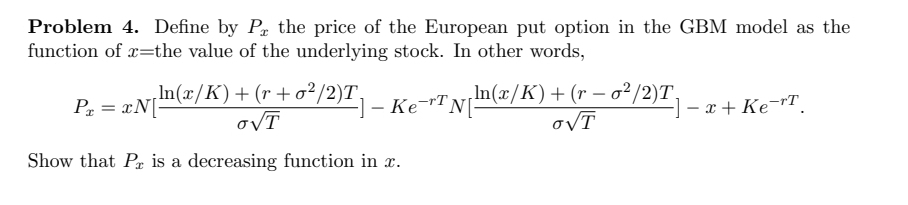

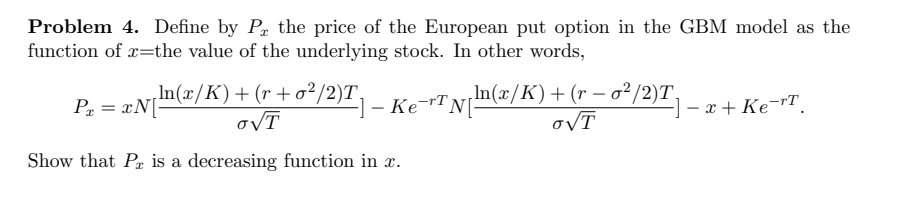

Problem 4. Define by Pr the price of the European put option in the GBM model as the function of x=the value of the underlying stock. In other words, Pa = ENI- In(x/ K) + (r+ 02/2)T In(x/ K) + (r - 02/2)T OVT - Ke TN- - x + Ke-T. OVT Show that Pr is a decreasing function in r

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock