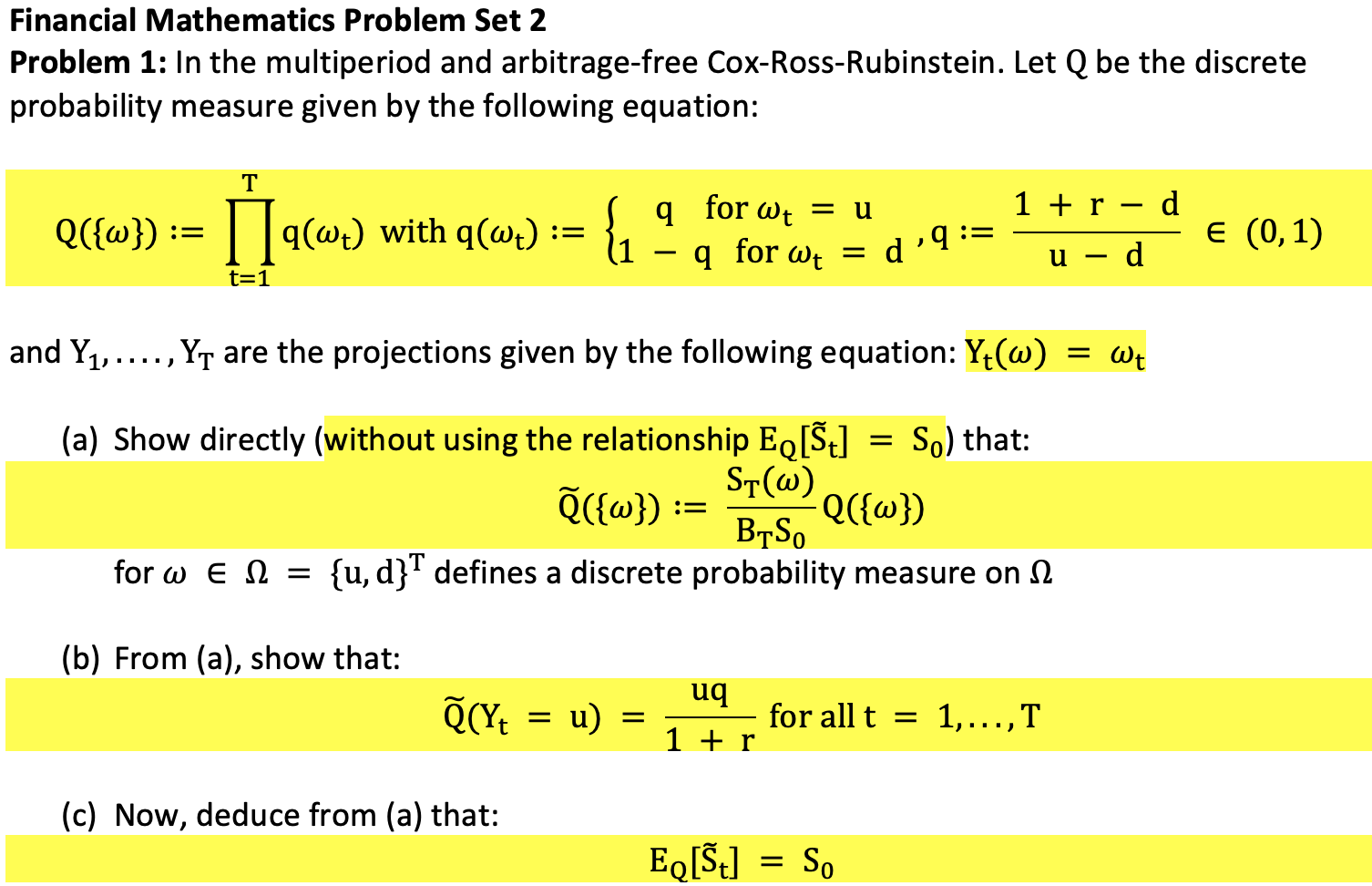

Question: Financial Mathematics Problem Set 2 Problem 1: In the multiperiod and arbitrage-free Cox-Ross-Rubinstein. Let Q be the discrete probability measure given by the following equation:

Financial Mathematics Problem Set 2 Problem 1: In the multiperiod and arbitrage-free Cox-Ross-Rubinstein. Let Q be the discrete probability measure given by the following equation: T 1 + r d Q[{w}) := = law) with 9(w) := { - geforce = d qwtq q Wt = u q at a = ( (0,1) = u d t=1 and Y1, ...., Yt are the projections given by the following equation: Yt(W) = Wt (a) Show directly (without using the relationship Eq[t] So) that: St(w) ({w}) := Q({w}) BTS. for {u, d}T defines a discrete probability measure on 2 = = a (b) From (a), show that: (Yt = u) = = uq for all t 1 + r = 1,...,T (c) Now, deduce from (a) that: Eq[St] = So Financial Mathematics Problem Set 2 Problem 1: In the multiperiod and arbitrage-free Cox-Ross-Rubinstein. Let Q be the discrete probability measure given by the following equation: T 1 + r d Q[{w}) := = law) with 9(w) := { - geforce = d qwtq q Wt = u q at a = ( (0,1) = u d t=1 and Y1, ...., Yt are the projections given by the following equation: Yt(W) = Wt (a) Show directly (without using the relationship Eq[t] So) that: St(w) ({w}) := Q({w}) BTS. for {u, d}T defines a discrete probability measure on 2 = = a (b) From (a), show that: (Yt = u) = = uq for all t 1 + r = 1,...,T (c) Now, deduce from (a) that: Eq[St] = So

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts