Question: Financial Returns Problem set Following on the example and calculations on page 149 in terms of the effects of leverage on return in a falling

Financial Returns Problem set

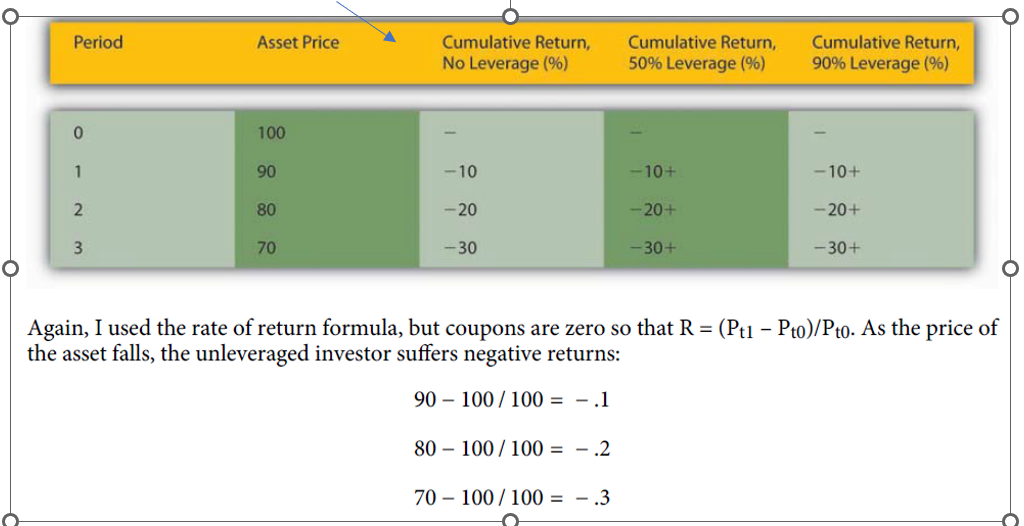

Following on the example and calculations on page 149 in terms of the effects of leverage on return in a falling market (Figure 12.2):

Solve and calculate the following table (keep your answers to three decimals):

Period Asset Price Cumulative return, no leverage (%)

4 60 ----------------

5 50 ___??____

6 40 ___??____

7 30 ___??____

8 20 ___??____

9 10 ___??____

10 5 ___??____

Again, I used the rate of return formula, but coupons are zero so that R=(Pt1Pt0)/Pt0. As the price of the asset falls, the unleveraged investor suffers negative returns: 90100/100=.180100/100=.270100/100=.3

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock