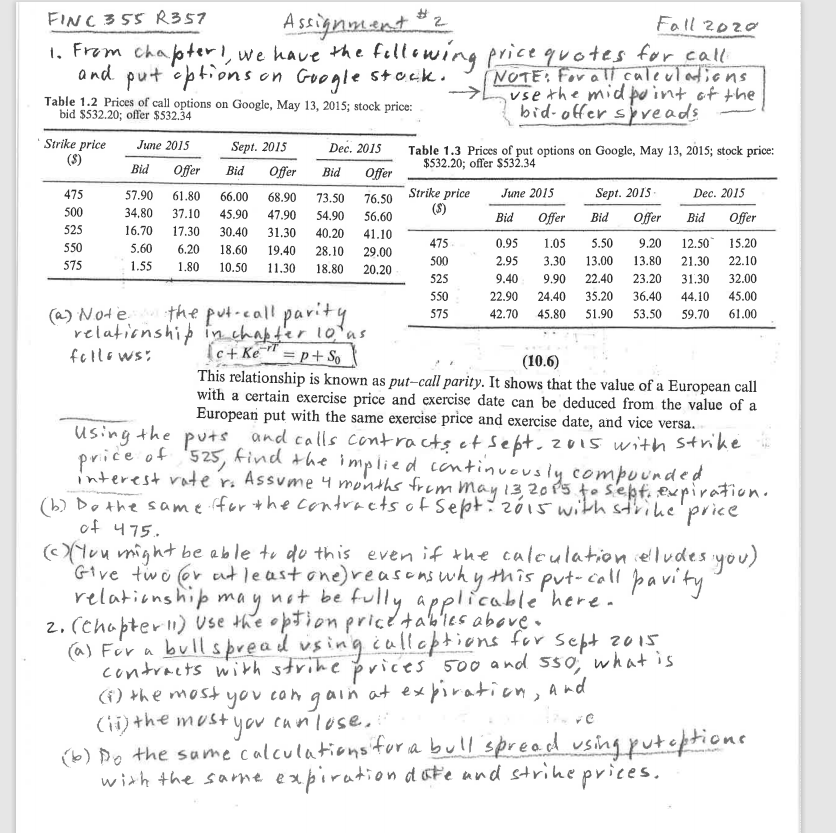

Question: FINC 355 R357 Assignment ? Fall 2020 1. From Chapter! We have the fellowing price quotes for call and put options on Google stock. NOTE:

FINC 355 R357 Assignment ? Fall 2020 1. From Chapter! We have the fellowing price quotes for call and put options on Google stock. NOTE: For all calculations use the midpoint of the bid-offer spreads Table 1.2 Prices of call options on Google, May 13, 2015; stock price: bid $532.20; offer $532.34 Strike price June 2015 Sept. 2015 Dec. 2015 () Table 1.3 Prices of put options on Google, May 13, 2015; stock price: Bid Offer Bid Offer $532.20; offer $532.34 Bid Offer 475 57.90 61.80 66.00 68.90 73.50 June 2015 Strike price 76.50 Sept. 2015 Dec. 2015 500 34.80 37.10 45.90 47.90 54.90 56.60 Bid Offer Bid Offer Bid Offer 525 16.70 17.30 30.40 31.30 40.20 41.10 550 5.60 475 0.95 1.05 5.50 9.20 6.20 19.40 12.50 15.20 18.60 28.10 29.00 575 1.55 2.95 500 3.30 13.00 13.80 1.80 21.30 22.10 10.50 11.30 18.80 20.20 525 9.40 9.90 22.40 23.20 31.30 32.00 550 22.90 24.40 35.20 36.40 44.10 45.00 (a) Note 42.70 45.80 51.90 53.50 59.70 61.00 575 the put-call parity relationship in chapter 10 us follows (c + Ke T = p + So (10.6) This relationship is known as put-call parity. It shows that the value of a European call with a certain exercise price and exercise date can be deduced from the value of a European put with the same exercise price and exercise date, and vice versa. using the puts and calls contracts et sept.zus with strike price of '525, find the implied continuously competence on Interest rater. Assume 4 months from May 13, 2015 to sent expiration. (b) Do the same for the contracts of sept. 2015 with strike price of 475 Muu might be able to do this even if the calculation celludes you) "Give two for at least one) reasons why hy this put-call parity relationship may not be fully applicable here. 2. (Chapter ) Use the option price tables above (a) For a bull spread using calloptions for Sept 2015 contracts with strine prices 500 and 550, what is (1) the most you can gain at expiration, and must you can lose. (b) Do the same calculations for a bull spread using put options with the same expiration date and strike prices. (ii) the most FINC 355 R357 Assignment ? Fall 2020 1. From Chapter! We have the fellowing price quotes for call and put options on Google stock. NOTE: For all calculations use the midpoint of the bid-offer spreads Table 1.2 Prices of call options on Google, May 13, 2015; stock price: bid $532.20; offer $532.34 Strike price June 2015 Sept. 2015 Dec. 2015 () Table 1.3 Prices of put options on Google, May 13, 2015; stock price: Bid Offer Bid Offer $532.20; offer $532.34 Bid Offer 475 57.90 61.80 66.00 68.90 73.50 June 2015 Strike price 76.50 Sept. 2015 Dec. 2015 500 34.80 37.10 45.90 47.90 54.90 56.60 Bid Offer Bid Offer Bid Offer 525 16.70 17.30 30.40 31.30 40.20 41.10 550 5.60 475 0.95 1.05 5.50 9.20 6.20 19.40 12.50 15.20 18.60 28.10 29.00 575 1.55 2.95 500 3.30 13.00 13.80 1.80 21.30 22.10 10.50 11.30 18.80 20.20 525 9.40 9.90 22.40 23.20 31.30 32.00 550 22.90 24.40 35.20 36.40 44.10 45.00 (a) Note 42.70 45.80 51.90 53.50 59.70 61.00 575 the put-call parity relationship in chapter 10 us follows (c + Ke T = p + So (10.6) This relationship is known as put-call parity. It shows that the value of a European call with a certain exercise price and exercise date can be deduced from the value of a European put with the same exercise price and exercise date, and vice versa. using the puts and calls contracts et sept.zus with strike price of '525, find the implied continuously competence on Interest rater. Assume 4 months from May 13, 2015 to sent expiration. (b) Do the same for the contracts of sept. 2015 with strike price of 475 Muu might be able to do this even if the calculation celludes you) "Give two for at least one) reasons why hy this put-call parity relationship may not be fully applicable here. 2. (Chapter ) Use the option price tables above (a) For a bull spread using calloptions for Sept 2015 contracts with strine prices 500 and 550, what is (1) the most you can gain at expiration, and must you can lose. (b) Do the same calculations for a bull spread using put options with the same expiration date and strike prices. (ii) the most

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts