Question: ?Find the global minimum variance portfolio. What is the expected return and variance of return of this portfolio? Expected Monthly Return PG Microsoft BAC Exxon

?Find the global minimum variance portfolio. What is the expected return and variance of return of this portfolio?

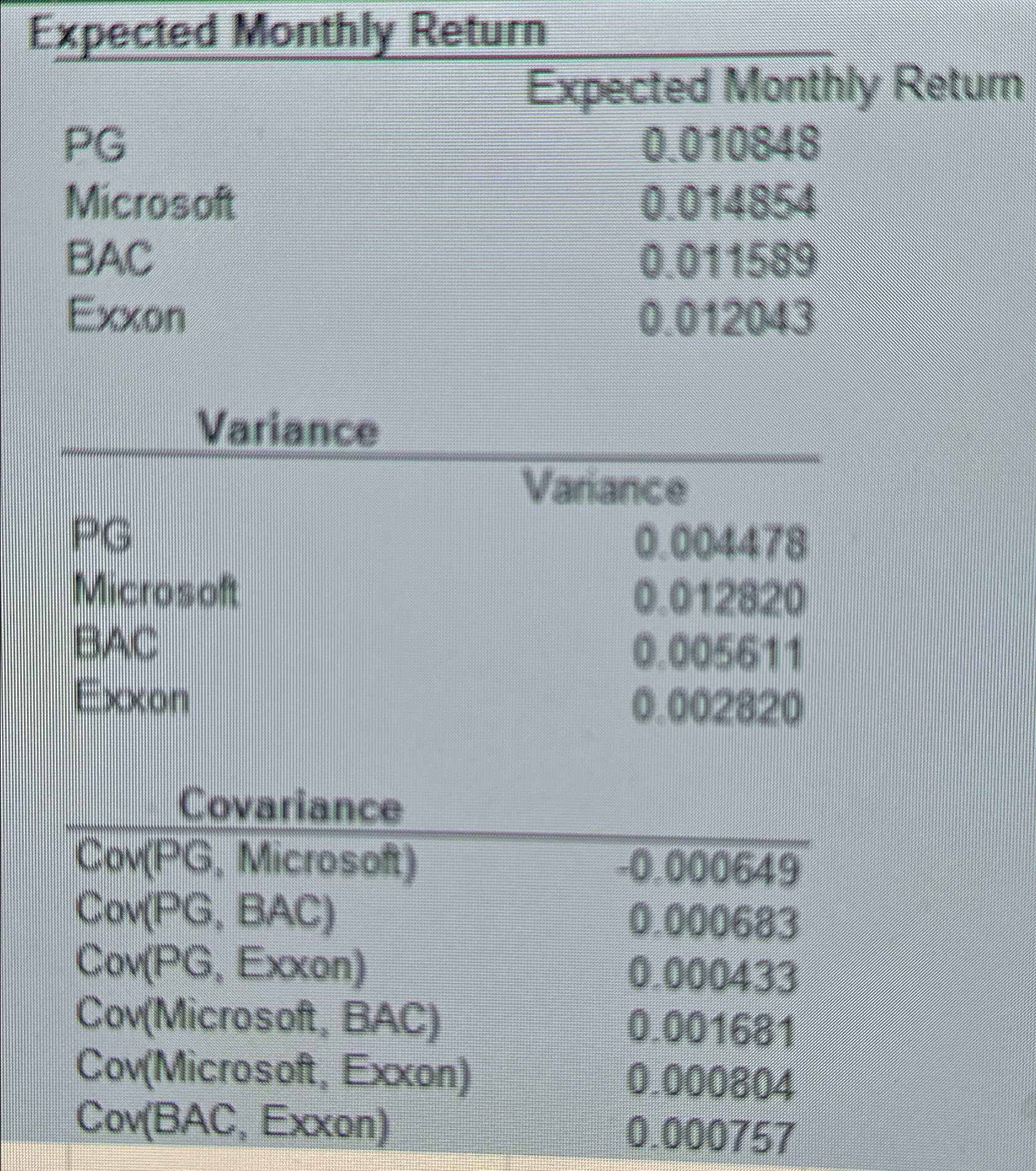

Expected Monthly Return PG Microsoft BAC Exxon Expected Monthly Return 0.010848 0.014854 0.011589 0.012043 Variance Variance PG 0.004478 Microsoft 0.012820 BAC 0.005611 Exxon 0.002820 Covariance Cov(PG, Microsoft) -0.000649 Cov(PG, BAC) 0.000683 Cov(PG, Exxon) 0.000433 Cov(Microsoft, BAC) 0.001681 Cov(Microsoft, Exxon) 0.000804 Cov(BAC, Exxon) 0.000757

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock