Fiona Company began operations on January 1, Year 1. The company has drafted its Year 5...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

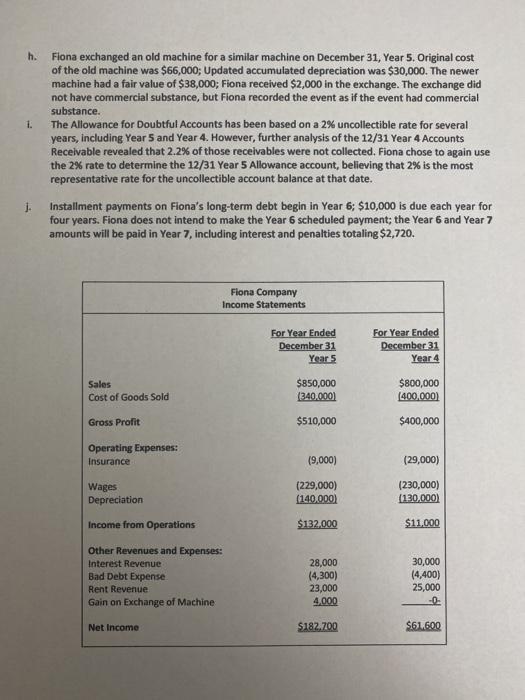

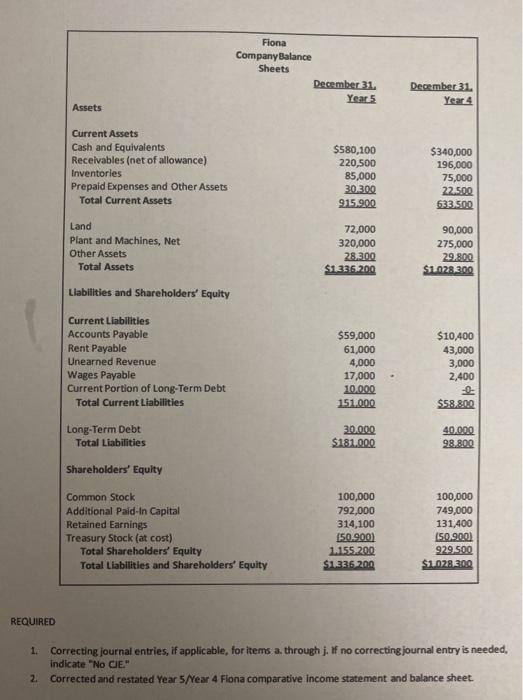

Fiona Company began operations on January 1, Year 1. The company has drafted its Year 5 comparative financial statements. Adjusting Journal Entries have been recorded; the Year 5 books are still open. Fiona will be audited for the first time. Auditors have discovered the following possible errors: a. b. C. d. e. f. g. Fiona purchased a machine on June 30, Year 2, paying $30,000 cash. The machine has a salvage value of $5,000 and a useful life of 5 years. The bookkeeper recorded straight-line depreciation for each year through Year 5, but failed to consider the salvage value. The physical inventory count on December 31, Year 4, improperly excluded merchandise costing $5,000 that had been temporarily stored in a public warehouse. Fiona uses a periodic inventory system. An $18,000 insurance premium was paid on October 1, Year 4, for a policy that expires on September 30, Year 7. The premium was charged to Insurance Expense when paid. No adjustments have been recorded since the payment date. Accrued wages payable to employees of $3,500 were not recorded on December 31, Year 4. This amount was expensed when paid in January, Year 5. Fiona sold land on December 31, Year 3, for $20,000, which was $2,000 above book value. Fiona recorded this journal entry: Cash 20,000 Cash Land Retained Earnings Fiona rented office space to Tyler's Company on January 1, Year 3. Fiona received an advanced payment of $40,000 on that date; the payment covered the Years 3 through 6. Fiona recorded this journal entry on January 1, Year 3: 18,000 2,000 40,000 Rent Payable No journal entries related to this rent have been recorded since the initial cash receipt on January 1, Year 3. 40,000 Fiona failed to accrue $10,000 of Interest Revenue for interest earned in Year 2. Revenue was recorded when the cash collection was received in Year 3. h. i. j. Fiona exchanged an old machine for a similar machine on December 31, Year 5. Original cost of the old machine was $66,000; Updated accumulated depreciation was $30,000. The newer machine had a fair value of $38,000; Fiona received $2,000 in the exchange. The exchange did not have commercial substance, but Fiona recorded the event as if the event had commercial substance. The Allowance for Doubtful Accounts has been based on a 2% uncollectible rate for several years, including Year 5 and Year 4. However, further analysis of the 12/31 Year 4 Accounts Receivable revealed that 2.2% of those receivables were not collected. Fiona chose to again use the 2% rate to determine the 12/31 Year 5 Allowance account, believing that 2% is the most representative rate for the uncollectible account balance at that date. Installment payments on Fiona's long-term debt begin in Year 6; $10,000 is due each year for four years. Fiona does not intend to make the Year 6 scheduled payment; the Year 6 and Year 7 amounts will be paid in Year 7, including interest and penalties totaling $2,720. Sales Cost of Goods Sold Gross Profit Operating Expenses: Insurance Wages Depreciation Income from Operations Other Revenues and Expenses: Interest Revenue Bad Debt Expense Rent Revenue Gain on Exchange of Machine Fiona Company Income Statements Net Income For Year Ended December 31 Year 5 $850,000 (340,000) $510,000 (9,000) (229,000) (140,000) $132,000 28,000 (4,300) 23,000 4,000 $182,700 For Year Ended December 31 Year 4 $800,000 (400,000) $400,000 (29,000) (230,000) (130,000) $11,000 30,000 (4,400) 25,000 -0- $61,600 REQUIRED Assets 2. Current Assets Cash and Equivalents Receivables (net of allowance) Inventories Prepaid Expenses and Other Assets Total Current Assets Land Plant and Machines, Net Other Assets Total Assets Liabilities and Shareholders' Equity Current Liabilities Accounts Payable Rent Payable Unearned Revenue Wages Payable Current Portion of Long-Term Debt Total Current Liabilities Long-Term Debt Total Liabilities Shareholders' Equity Common Stock Additional Paid-In Capital Retained Earnings. Treasury Stock (at cost) Fiona Company Balance Sheets Total Shareholders' Equity Total Liabilities and Shareholders' Equity December 31, Year 5 $580,100 220,500 85,000 30,300 915,900 72,000 320,000 28,300 $1,336,200 $59,000 61,000 4,000 17,000 10,000 151,000 30,000 $181,000 100,000 792,000 314,100 (50,900) 1,155,200 $1,336,200 December 31, Year 4 $340,000 196,000 75,000 22,500 633,500 90,000 275,000 29,800 $1,028,300 $10,400 43,000 3,000 2,400 -0- $58,800 40,000 98,800 100,000 749,000 131,400 (50,900) 929,500 $1,028,300 1. Correcting journal entries, if applicable, for items a. through j. If no correcting journal entry is needed, indicate "No CJE." Corrected and restated Year 5/Year 4 Fiona comparative income statement and balance sheet. Fiona Company began operations on January 1, Year 1. The company has drafted its Year 5 comparative financial statements. Adjusting Journal Entries have been recorded; the Year 5 books are still open. Fiona will be audited for the first time. Auditors have discovered the following possible errors: a. b. The physical inventory count on December 31, Year 4, improperly excluded merchandise costing $5,000 that had been temporarily stored in a public warehouse. Fiona uses a periodic inventory system. C. d. e. Fiona purchased a machine on June 30, Year 2, paying $30,000 cash. The machine has a salvage value of $5,000 and a useful life of 5 years. The bookkeeper recorded straight-line depreciation for each year through Year 5, but failed to consider the salvage value. g. An $18,000 insurance premium was paid on October 1, Year 4, for a policy that expires on September 30, Year 7. The premium was charged to Insurance Expense when paid. No adjustments have been recorded since the payment date. Accrued wages payable to employees of $3,500 were not recorded on December 31, Year 4. This amount was expensed when paid in January, Year 5. Fiona sold land on December 31, Year 3, for $20,000, which was $2,000 above book value. Fiona recorded this journal entry: Cash 20,000 Cash Land Retained Earnings f. Fiona rented office space to Tyler's Company on January 1, Year 3. Fiona received an advanced payment of $40,000 on that date; the payment covered the Years 3 through 6. Fiona recorded this journal entry on January 1, Year 3: 18,000 2,000 40,000 Rent Payable No journal entries related to this rent have been recorded since the initial cash receipt on January 1, Year 3. 40,000 Fiona failed to accrue $10,000 of Interest Revenue for interest earned in Year 2. Revenue was recorded when the cash collection was received in Year 3. h. Fiona exchanged an old machine for a similar machine on December 31, Year 5. Original cost of the old machine was $66,000; Updated accumulated depreciation was $30,000. The newer machine had a fair value of $38,000; Fiona received $2,000 in the exchange. The exchange did not have commercial substance, but Fiona recorded the event as if the event had commercial substance. 1. The Allowance for Doubtful Accounts has been based on a 2% uncollectible rate for several years, including Year 5 and Year 4. However, further analysis of the 12/31 Year 4 Accounts Receivable revealed that 2.2% of those receivables were not collected. Fiona chose to again use the 2% rate to determine the 12/31 Year 5 Allowance account, believing that 2% is the most representative rate for the uncollectible account balance at that date. j. Installment payments on Fiona's long-term debt begin in Year 6; $10,000 is due each year for four years. Fiona does not intend to make the Year 6 scheduled payment; the Year 6 and Year 7 amounts will be paid in Year 7, including interest and penalties totaling $2,720. Sales Cost of Goods Sold Gross Profit Operating Expenses: Insurance Fiona Company Income Statements Wages Depreciation Income from Operations Other Revenues and Expenses: Interest Revenue Bad Debt Expense Rent Revenue Gain on Exchange of Machine Net Income For Year Ended December 31 Year 5 $850,000 (340,000) $510,000 (9,000) (229,000) (140,000) $132,000 28,000 (4,300) 23,000 4,000 $182.700 For Year Ended December 31 Year 4 $800,000 (400,000) $400,000 (29,000) (230,000) (130,000) $11,000 30,000 (4,400) 25,000 $61.600 REQUIRED Assets Current Assets Cash and Equivalents Receivables (net of allowance) Inventories Prepaid Expenses and Other Assets Total Current Assets Land Plant and Machines, Net Other Assets Total Assets Liabilities and Shareholders' Equity Current Liabilities Accounts Payable Rent Payable Unearned Revenue Wages Payable Current Portion of Long-Term Debt Total Current Liabilities Long-Term Debt Total Liabilities Shareholders' Equity Common Stock Additional Paid-In Capital Retained Earnings Treasury Stock (at cost) Fiona Company Balance Sheets Total Shareholders' Equity Total Liabilities and Shareholders' Equity December 31. Year 5 $580,100 220,500 85,000 30.300 915.900 72,000 320,000 28.300 $1.336.200 $59,000 61,000 4,000 17,000 10.000 151.000 30.000 $181.000 100,000 792,000 314,100 (50.900) 1.155.200 $1.336.200 December 31. Year 4 $340,000 196,000 75,000 22.500 633.500 90,000 275,000 29.800 $1.028.300 $10,400 43,000 3,000 2,400 -0- $58.800 40,000 98.800 100,000 749,000 131,400 (50.900) 929.500 $1.028.300 1. Correcting journal entries, if applicable, for items a. through j. If no correcting journal entry is needed, indicate "No CIE." 2. Corrected and restated Year 5/Year 4 Fiona comparative income statement and balance sheet. Fiona Company began operations on January 1, Year 1. The company has drafted its Year 5 comparative financial statements. Adjusting Journal Entries have been recorded; the Year 5 books are still open. Fiona will be audited for the first time. Auditors have discovered the following possible errors: a. b. C. d. e. f. g. Fiona purchased a machine on June 30, Year 2, paying $30,000 cash. The machine has a salvage value of $5,000 and a useful life of 5 years. The bookkeeper recorded straight-line depreciation for each year through Year 5, but failed to consider the salvage value. The physical inventory count on December 31, Year 4, improperly excluded merchandise costing $5,000 that had been temporarily stored in a public warehouse. Fiona uses a periodic inventory system. An $18,000 insurance premium was paid on October 1, Year 4, for a policy that expires on September 30, Year 7. The premium was charged to Insurance Expense when paid. No adjustments have been recorded since the payment date. Accrued wages payable to employees of $3,500 were not recorded on December 31, Year 4. This amount was expensed when paid in January, Year 5. Fiona sold land on December 31, Year 3, for $20,000, which was $2,000 above book value. Fiona recorded this journal entry: Cash 20,000 Cash Land Retained Earnings Fiona rented office space to Tyler's Company on January 1, Year 3. Fiona received an advanced payment of $40,000 on that date; the payment covered the Years 3 through 6. Fiona recorded this journal entry on January 1, Year 3: 18,000 2,000 40,000 Rent Payable No journal entries related to this rent have been recorded since the initial cash receipt on January 1, Year 3. 40,000 Fiona failed to accrue $10,000 of Interest Revenue for interest earned in Year 2. Revenue was recorded when the cash collection was received in Year 3. h. i. j. Fiona exchanged an old machine for a similar machine on December 31, Year 5. Original cost of the old machine was $66,000; Updated accumulated depreciation was $30,000. The newer machine had a fair value of $38,000; Fiona received $2,000 in the exchange. The exchange did not have commercial substance, but Fiona recorded the event as if the event had commercial substance. The Allowance for Doubtful Accounts has been based on a 2% uncollectible rate for several years, including Year 5 and Year 4. However, further analysis of the 12/31 Year 4 Accounts Receivable revealed that 2.2% of those receivables were not collected. Fiona chose to again use the 2% rate to determine the 12/31 Year 5 Allowance account, believing that 2% is the most representative rate for the uncollectible account balance at that date. Installment payments on Fiona's long-term debt begin in Year 6; $10,000 is due each year for four years. Fiona does not intend to make the Year 6 scheduled payment; the Year 6 and Year 7 amounts will be paid in Year 7, including interest and penalties totaling $2,720. Sales Cost of Goods Sold Gross Profit Operating Expenses: Insurance Wages Depreciation Income from Operations Other Revenues and Expenses: Interest Revenue Bad Debt Expense Rent Revenue Gain on Exchange of Machine Fiona Company Income Statements Net Income For Year Ended December 31 Year 5 $850,000 (340,000) $510,000 (9,000) (229,000) (140,000) $132,000 28,000 (4,300) 23,000 4,000 $182,700 For Year Ended December 31 Year 4 $800,000 (400,000) $400,000 (29,000) (230,000) (130,000) $11,000 30,000 (4,400) 25,000 -0- $61,600 REQUIRED Assets 2. Current Assets Cash and Equivalents Receivables (net of allowance) Inventories Prepaid Expenses and Other Assets Total Current Assets Land Plant and Machines, Net Other Assets Total Assets Liabilities and Shareholders' Equity Current Liabilities Accounts Payable Rent Payable Unearned Revenue Wages Payable Current Portion of Long-Term Debt Total Current Liabilities Long-Term Debt Total Liabilities Shareholders' Equity Common Stock Additional Paid-In Capital Retained Earnings. Treasury Stock (at cost) Fiona Company Balance Sheets Total Shareholders' Equity Total Liabilities and Shareholders' Equity December 31, Year 5 $580,100 220,500 85,000 30,300 915,900 72,000 320,000 28,300 $1,336,200 $59,000 61,000 4,000 17,000 10,000 151,000 30,000 $181,000 100,000 792,000 314,100 (50,900) 1,155,200 $1,336,200 December 31, Year 4 $340,000 196,000 75,000 22,500 633,500 90,000 275,000 29,800 $1,028,300 $10,400 43,000 3,000 2,400 -0- $58,800 40,000 98,800 100,000 749,000 131,400 (50,900) 929,500 $1,028,300 1. Correcting journal entries, if applicable, for items a. through j. If no correcting journal entry is needed, indicate "No CJE." Corrected and restated Year 5/Year 4 Fiona comparative income statement and balance sheet. Fiona Company began operations on January 1, Year 1. The company has drafted its Year 5 comparative financial statements. Adjusting Journal Entries have been recorded; the Year 5 books are still open. Fiona will be audited for the first time. Auditors have discovered the following possible errors: a. b. The physical inventory count on December 31, Year 4, improperly excluded merchandise costing $5,000 that had been temporarily stored in a public warehouse. Fiona uses a periodic inventory system. C. d. e. Fiona purchased a machine on June 30, Year 2, paying $30,000 cash. The machine has a salvage value of $5,000 and a useful life of 5 years. The bookkeeper recorded straight-line depreciation for each year through Year 5, but failed to consider the salvage value. g. An $18,000 insurance premium was paid on October 1, Year 4, for a policy that expires on September 30, Year 7. The premium was charged to Insurance Expense when paid. No adjustments have been recorded since the payment date. Accrued wages payable to employees of $3,500 were not recorded on December 31, Year 4. This amount was expensed when paid in January, Year 5. Fiona sold land on December 31, Year 3, for $20,000, which was $2,000 above book value. Fiona recorded this journal entry: Cash 20,000 Cash Land Retained Earnings f. Fiona rented office space to Tyler's Company on January 1, Year 3. Fiona received an advanced payment of $40,000 on that date; the payment covered the Years 3 through 6. Fiona recorded this journal entry on January 1, Year 3: 18,000 2,000 40,000 Rent Payable No journal entries related to this rent have been recorded since the initial cash receipt on January 1, Year 3. 40,000 Fiona failed to accrue $10,000 of Interest Revenue for interest earned in Year 2. Revenue was recorded when the cash collection was received in Year 3. h. Fiona exchanged an old machine for a similar machine on December 31, Year 5. Original cost of the old machine was $66,000; Updated accumulated depreciation was $30,000. The newer machine had a fair value of $38,000; Fiona received $2,000 in the exchange. The exchange did not have commercial substance, but Fiona recorded the event as if the event had commercial substance. 1. The Allowance for Doubtful Accounts has been based on a 2% uncollectible rate for several years, including Year 5 and Year 4. However, further analysis of the 12/31 Year 4 Accounts Receivable revealed that 2.2% of those receivables were not collected. Fiona chose to again use the 2% rate to determine the 12/31 Year 5 Allowance account, believing that 2% is the most representative rate for the uncollectible account balance at that date. j. Installment payments on Fiona's long-term debt begin in Year 6; $10,000 is due each year for four years. Fiona does not intend to make the Year 6 scheduled payment; the Year 6 and Year 7 amounts will be paid in Year 7, including interest and penalties totaling $2,720. Sales Cost of Goods Sold Gross Profit Operating Expenses: Insurance Fiona Company Income Statements Wages Depreciation Income from Operations Other Revenues and Expenses: Interest Revenue Bad Debt Expense Rent Revenue Gain on Exchange of Machine Net Income For Year Ended December 31 Year 5 $850,000 (340,000) $510,000 (9,000) (229,000) (140,000) $132,000 28,000 (4,300) 23,000 4,000 $182.700 For Year Ended December 31 Year 4 $800,000 (400,000) $400,000 (29,000) (230,000) (130,000) $11,000 30,000 (4,400) 25,000 $61.600 REQUIRED Assets Current Assets Cash and Equivalents Receivables (net of allowance) Inventories Prepaid Expenses and Other Assets Total Current Assets Land Plant and Machines, Net Other Assets Total Assets Liabilities and Shareholders' Equity Current Liabilities Accounts Payable Rent Payable Unearned Revenue Wages Payable Current Portion of Long-Term Debt Total Current Liabilities Long-Term Debt Total Liabilities Shareholders' Equity Common Stock Additional Paid-In Capital Retained Earnings Treasury Stock (at cost) Fiona Company Balance Sheets Total Shareholders' Equity Total Liabilities and Shareholders' Equity December 31. Year 5 $580,100 220,500 85,000 30.300 915.900 72,000 320,000 28.300 $1.336.200 $59,000 61,000 4,000 17,000 10.000 151.000 30.000 $181.000 100,000 792,000 314,100 (50.900) 1.155.200 $1.336.200 December 31. Year 4 $340,000 196,000 75,000 22.500 633.500 90,000 275,000 29.800 $1.028.300 $10,400 43,000 3,000 2,400 -0- $58.800 40,000 98.800 100,000 749,000 131,400 (50.900) 929.500 $1.028.300 1. Correcting journal entries, if applicable, for items a. through j. If no correcting journal entry is needed, indicate "No CIE." 2. Corrected and restated Year 5/Year 4 Fiona comparative income statement and balance sheet.

Expert Answer:

Answer rating: 100% (QA)

Based on the provided information we will address each of the possible errors a through j listed in the document and provide the necessary correcting journal entries if applicable Lets go through each ... View the full answer

Posted Date:

Students also viewed these accounting questions

-

The following information is an extract from the financial statements of Diego Ltd SoFP extracts (s) Equity Share capital Share premium Retained earnings Current liabilities Interest payable...

-

A subsidiary of a U.S. company began operations on January I, 2014, in a country whose currency is identified as hyperinflationary. The subsidiary's local currency (LC) is its functional currency....

-

The company ABC Inc. began operations on January 1 of the current year. During the month of January they carried out various business activities. His two partners contributed $ 20,000, in cash, each,...

-

Using Figure 11.25 and the related text, describe the features of terracing, and list the major alterations to soil and water brought about by this agricultural method. Figure 11.25

-

Venzuela Inc. is building a new hockey arena at a cost of $2.5 million. It received a down payment of $500,000 from local businesses to support the project, and now needs to borrow $2 million to...

-

Biondi Industries is a manufacturer of chemicals for various purposes. One of the processes used by Biondi produces HTP3, a chemical used in hot tubs and swimming pools; PST4, a chemical used in...

-

Discuss the criminal trial process.

-

A long cylindrical rod of very high emissivity is heat treated within a long, evacuated oven of square cross section as shown in the sketch. The oven walls exhibit blackbody behavior. Due to...

-

Rose Hill, a soybean farm in northern Minnesota, has a herd of 4 5 dairy cows. The cows produce approximately 2 , 5 2 0 gallons of milk per week. The farm currently sells all its milk to a nearby...

-

Nutrition is often talked about in everyday pop culture. Nutrition science, however, is not always part of the conversation. Respond to the following in a minimum of 175 words: Discuss some examples...

-

After Mario completes his monthly report, his boss reviews it to see if the standards were met. If there are errors, Mario is told he has to work an extra hour each day for the next two weeks. This...

-

Assume a company had sales of $383,000 (all on account) and net income of $60,000. It provided the following excerpts from its balance sheet: This Year Last Year Current assets: Accounts receivable $...

-

A study reports that only 12% of people stick to their New Year's resolutions. Suppose you sample 100 people about whether they stuck to their resolutions. What is the standard error of the...

-

3. (5 points An agent has mean-variance preferences. In particular, her utility for a portfolio with mean return and standard deviation is: U = - 302 2 (5) Two funds are available to the investor,...

-

Kam Company purchased a machine on January 2 , 2 0 1 9 , for $ 2 0 , 0 0 0 . The machine had an expected life of 8 years and a residual value of $ 3 0 0 . The double - declining - balance method of...

-

Assume that diminishing marginal utility applies to both coffee and football tickets and that the consumer is spending all of her income. If a consumer purchases a combination of coffee and football...

-

Using a while loop structure, a loop based on a counter variable which will cycle through 10 iterations. With each iteration of the loop, request a grade from the user and add it to a running total....

-

Imagine a sound wave with a frequency of 1.10 kHz propagating with a speed of 330 m/s. Determine the phase difference in radians between any two points on the wave separated by 10.0 cm.

-

Why does spreading feet apart help a surfer stay on the board?

-

Why will a projectile that moves horizontally at 8 km/s follow a curve that matches the curvature of Earth?

-

How much speed does a freely falling object gain during each second of fall?

Study smarter with the SolutionInn App