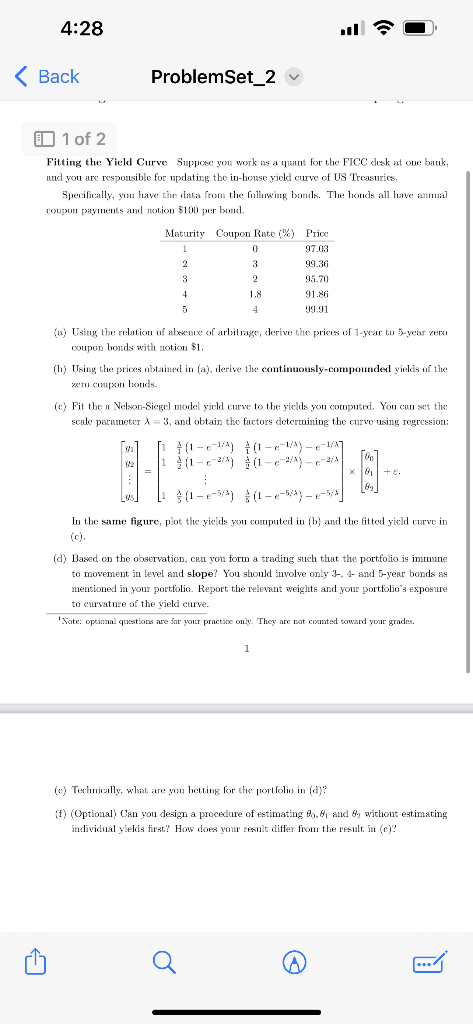

Question: Fitting the Yicld Curve Suppose you work as a quant for the FICC dosk at one bank, and you are responsible for updating the in-house

Fitting the Yicld Curve Suppose you work as a quant for the FICC dosk at one bank, and you are responsible for updating the in-house yjeld curve of US Treasurics. Specifically, you have the data from the following bouls. The honds all have anmal coupun payments and notion $100 per bond. (a) Using the relation of abeence of arbitrage, derive the prices of 1-year to 5-year zero coupon bonds with notion $1. (h) Using the prices abtained in (a), derive the continuously-compounded yields of the weru coupon bonds. (c) Fit the a Nelson-Siege] model yield curve to the yields you computod. You can set the scale parumeter =3, and obtain the factors determining the curve using regression: y1y25=1111(1e1/)2(1e2/)5(1e5/)1(1e1/)e1/2(1e2/)e2/5(1e5/)e5/012+. In the same figure, plot the yields you computed in (b) and the fitted yield curve in (c) (d) Based on the observation, can you form a trading such that the portfolio is immune to movement in level and slope? You should involve only 3-, 4- and 5-year bonds as mentioned in your portfolio. Report the relevant weights and your porttolio's exposure to currature of the yjeld curve. ' Sate: opcional questions are zor your practioe only. They are not coanted coward your grades. 1 (c) Techucally, what are you hetting for the portfolio in (d)? (f) (Optional) Can you design a procedure of estimating 0,1 and 82 without eatimating individial yields firat? How does your result differ from the result in (c)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts