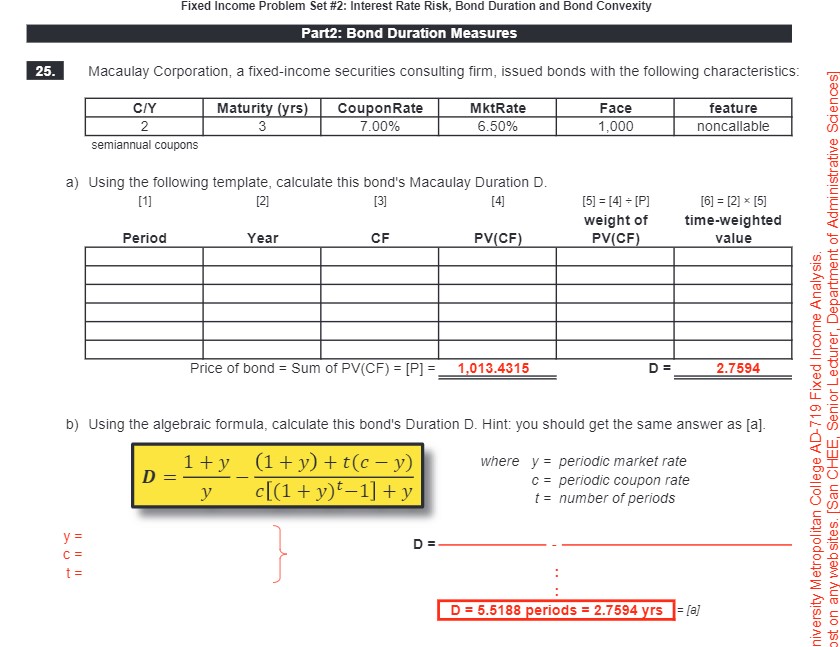

Question: Fixed Income Problem Set #2: Interest Rate Risk, Bond Duration and Bond Convexity Part2: Bond Duration Measures 25. Macaulay Corporation, a fixed-income securities consulting firm,

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts