Question: Flag question: Question 4 Question 4 You have the following information: Stock A B C D Market Alpha 1% 2% 3% -2% 0% Beta 1.25

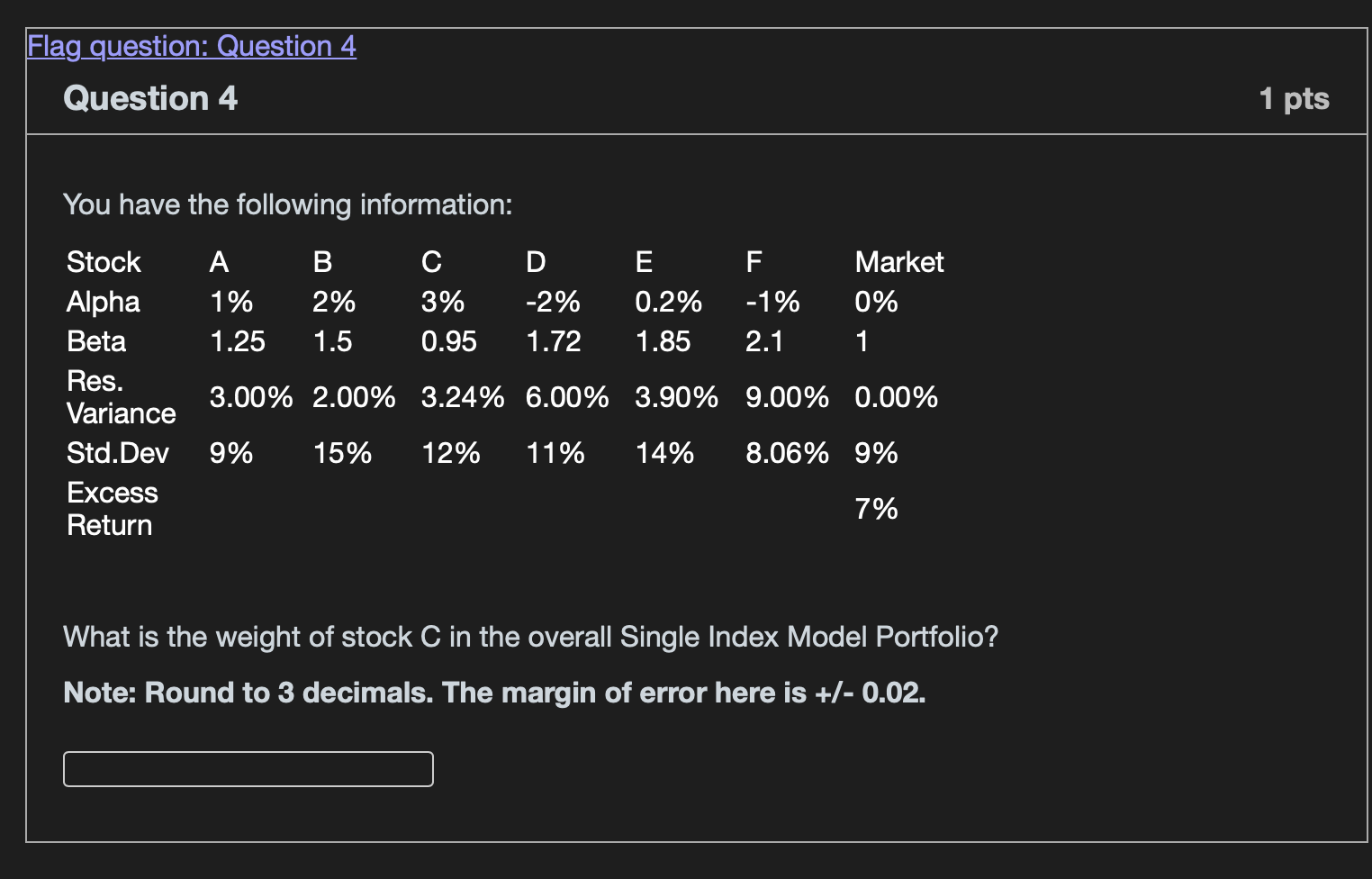

Flag question: Question 4 Question 4 You have the following information: Stock A B C D Market Alpha 1% 2% 3% -2% 0% Beta 1.25 1.5 0.95 1.72 1 Res. 3.00% 2.00% 3.24% 6.00% 3.90% 9.00% 0.00% Variance Std.Dev 9% 15% 12% 11% 14% 8.06% 9% Excess 7% Return What is the weight of stock C in the overall Single Index Model Portfolio? Note: Round to 3 decimals. The margin of error here is +/- 0.02. E 0.2% F -1% 1.85 2.1 1 pts Flag question: Question 4 Question 4 You have the following information: Stock A B C D Market Alpha 1% 2% 3% -2% 0% Beta 1.25 1.5 0.95 1.72 1 Res. 3.00% 2.00% 3.24% 6.00% 3.90% 9.00% 0.00% Variance Std.Dev 9% 15% 12% 11% 14% 8.06% 9% Excess 7% Return What is the weight of stock C in the overall Single Index Model Portfolio? Note: Round to 3 decimals. The margin of error here is +/- 0.02. E 0.2% F -1% 1.85 2.1 1 pts

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts