Question: Following the input data from excel in black colour solve the question above. Throughout the case assume costs of 1,000 EUR and revenues of 1,500

Following the input data from excel in black colour solve the question above.

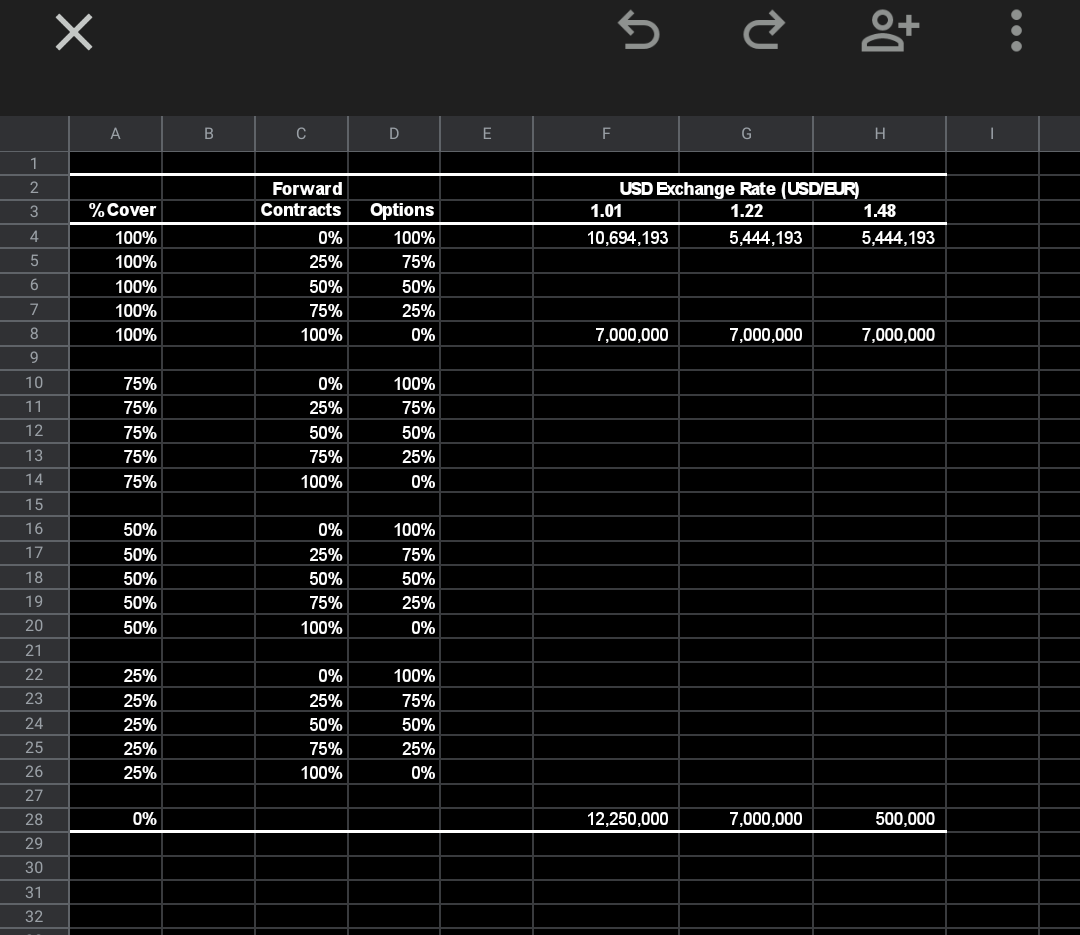

Throughout the case assume costs of 1,000 EUR and revenues of 1,500 USD per participant will be incurred in 1 year. Also assume EUR and USD interest rates of 2% continuously compounded (the forward exchange rate equals the spot exchange rate under CIP). Finally, assume that a 1-year, at-the-money call or put option on 1 EUR (K=1.22 USD/EUR) costs 0.061 (5% of the USD notional) as stated in the case. 1. Exhibit 9 is available on NYU Classes with several rows completed a. Complete Exhibit 9 by calculating the profit in each hedging scenario assuming a final sales volume of 25,000 and the 3 future exchange rates given. Use at-the- money options and don't forget to future value the cost of the options to time 1. b. Plot the profit (on the vertical, Y-axis) against the future exchange rate (on the horizontal, X-axis) for some representative scenarios. Be sure you have the correct variables for the Y and X axes! Notes: 1. Exhibit 9 in the case talks about the hedging impact. I want you to plot profits in each scenario, i.e., revenues less costs plus/minus the payoffs from hedging including the FV of the option cost. 2. I have provided the numbers for a couple of cases in the spreadsheet. Make sure your calculations can match these numbers. X 5 ot A . D E F. G H 1 2 3 USD Exchange Rate (USD/EUR) 1.01 1.22 1.48 10,694,193 5,444,193 5,444,193 4 5 % Cover 100% 100% 100% 100% 100% Forward Contracts 0% 25% 50% 75% 100% Options 100% 75% 50% 25% 0% 6 7 8 7,000,000 7,000,000 7,000,000 9 10 11 12 75% 75% 75% 75% 75% 0% 25% 50% 75% 100% 100% 75% 50% 25% 0% 13 14 15 16 17 18 50% 50% 50% 50% 50% 0% 25% 50% 75% 100% 100% 75% 50% 25% 0% 19 20 21 22 23 24 25 26 100% 75% 25% 25% 25% 25% 25% 0% 25% 50% 75% 100% 50% 25% 0% 27 0% 12,250,000 7,000,000 500,000 28 29 30 31 32 Throughout the case assume costs of 1,000 EUR and revenues of 1,500 USD per participant will be incurred in 1 year. Also assume EUR and USD interest rates of 2% continuously compounded (the forward exchange rate equals the spot exchange rate under CIP). Finally, assume that a 1-year, at-the-money call or put option on 1 EUR (K=1.22 USD/EUR) costs 0.061 (5% of the USD notional) as stated in the case. 1. Exhibit 9 is available on NYU Classes with several rows completed a. Complete Exhibit 9 by calculating the profit in each hedging scenario assuming a final sales volume of 25,000 and the 3 future exchange rates given. Use at-the- money options and don't forget to future value the cost of the options to time 1. b. Plot the profit (on the vertical, Y-axis) against the future exchange rate (on the horizontal, X-axis) for some representative scenarios. Be sure you have the correct variables for the Y and X axes! Notes: 1. Exhibit 9 in the case talks about the hedging impact. I want you to plot profits in each scenario, i.e., revenues less costs plus/minus the payoffs from hedging including the FV of the option cost. 2. I have provided the numbers for a couple of cases in the spreadsheet. Make sure your calculations can match these numbers. X 5 ot A . D E F. G H 1 2 3 USD Exchange Rate (USD/EUR) 1.01 1.22 1.48 10,694,193 5,444,193 5,444,193 4 5 % Cover 100% 100% 100% 100% 100% Forward Contracts 0% 25% 50% 75% 100% Options 100% 75% 50% 25% 0% 6 7 8 7,000,000 7,000,000 7,000,000 9 10 11 12 75% 75% 75% 75% 75% 0% 25% 50% 75% 100% 100% 75% 50% 25% 0% 13 14 15 16 17 18 50% 50% 50% 50% 50% 0% 25% 50% 75% 100% 100% 75% 50% 25% 0% 19 20 21 22 23 24 25 26 100% 75% 25% 25% 25% 25% 25% 0% 25% 50% 75% 100% 50% 25% 0% 27 0% 12,250,000 7,000,000 500,000 28 29 30 31 32

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts