For 8824 Department of the Treasury Internal Revenue Service Name shown on tax retur 2 3...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

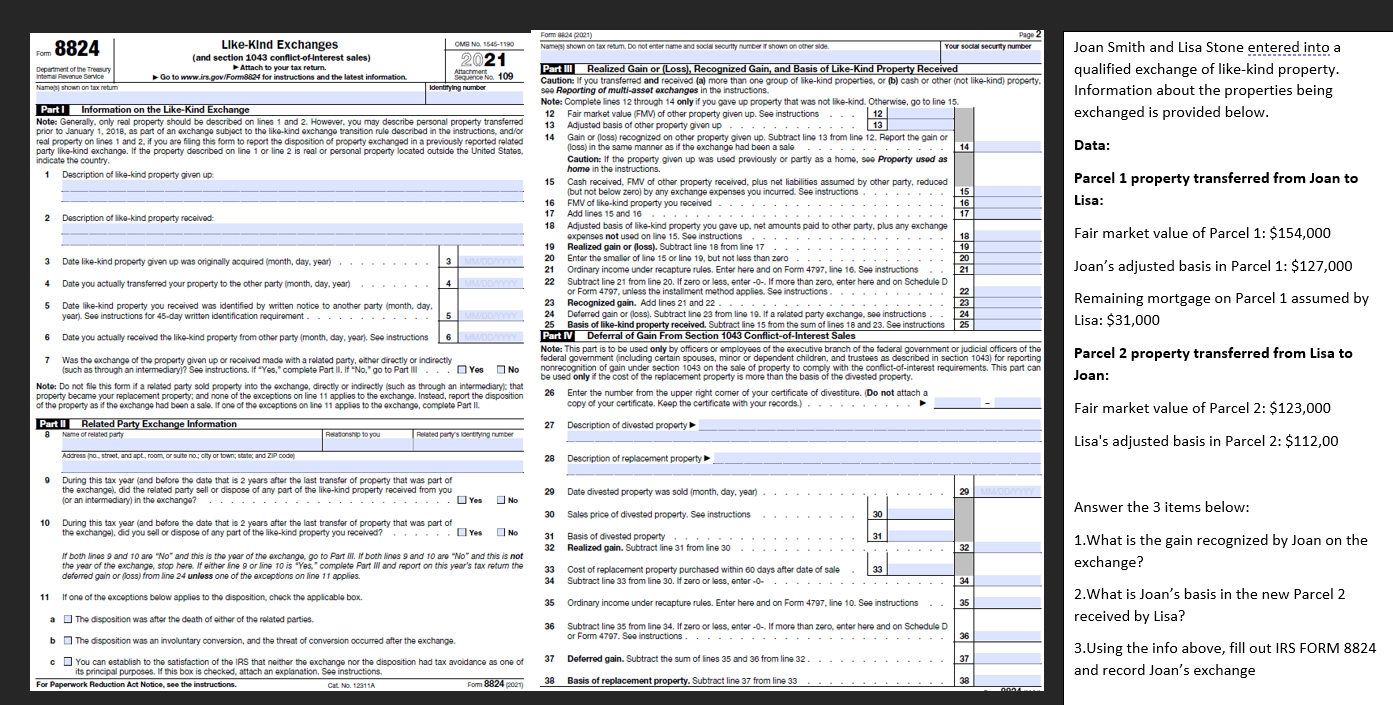

For 8824 Department of the Treasury Internal Revenue Service Name shown on tax retur 2 3 Part I Information on the Like-Kind Exchange Note: Generally, only real property should be described on lines 1 and 2. However, you may describe personal property transferred prior to January 1, 2018, as part of an exchange subject to the like-kind exchange transition rule described in the instructions, and/or real property on lines 1 and 2, if you are filing this form to report the disposition of property exchanged in a previously reported related party like-kind exchange. If the property described on line 1 or line 2 is real or personal property located outside the United States, indicate the country. 1 Description of like-kind property given up 4 6 Date like-kind property given up was originally acquired (month, day, year). Date you actually transferred your property to the other party (month, day, year). 5 Date like-kind property you received was identified by written notice to another party (month, day. year). See instructions for 45-day written identification requirement....... 5 MM/DD/Y Date you actually received the like-kind property from other party (month, day, year). See instructions 6 MM/DD Like-Kind Exchanges (and section 1043 conflict-of-interest sales) Attach to your tax return. Go to www.irs.gov/Form8824 for instructions and the latest information Description of like-kind property received: Part II Related Party Exchange Information 8 Name of related party 11 7 Was the exchange of the property given up or received made with a related party, either directly or indirectly (such as through an intermediary)? See instructions. If "Yes," complete Part II. If "No," go to Part III Yes No Note: Do not file this form if a related party sold property into the exchange, directly or indirectly (such as through an intermediary); that property became your replacement property; and none of the exceptions on line 11 applies to the exchange. Instead, report the disposition of the property as if the exchange had been a sale. If one of the exceptions on line 11 applies to the exchange, complete Part II. a Identifying number Address (no, street, and apt, room, or sulte no.; city or town; state and ZIP code) b OMB No 1545-1190 2021 achmert 109 Relationship to you 3 9 During this tax year (and before the date that is 2 years after the last transfer of property that was part of the exchange), did the related party sell or dispose of any part of the like-kind property received from you (or an intermediary) in the exchange? 4 MM/DD/YYYY ....... Related party's identifying number 10 During this tax year (and before the date that is 2 years after the last transfer of property that was part of the exchange), did you sell or dispose of any part of the like-kind property you received? Yes Yes If both lines 9 and 10 are "No" and this is the year of the exchange, go to Part III. If both lines 9 and 10 are "No" and this is not the year of the exchange, stop here. If either line 9 or line 10 is "Yes," complete Part III and report on this year's tax return the deferred gain or (loss) from line 24 unless one of the exceptions on line 11 applies. If one of the exceptions below applies to the disposition, check the applicable box. The disposition was after the death of either of the related parties. The disposition was an involuntary conversion, and the threat of conversion occurred after the exchange. You can establish to the satisfaction of the IRS that neither the exchange nor the disposition had tax avoidance as one of its principal purposes. If this box is checked, attach an explanation. See instructions. For Paperwork Reduction Act Notice, see the instructions. Cat No. 12311A Form 8824 021) No No Form 24 (2021) Name shown on tax retum. Do not enter name and social security number if shown on other side 15 Part III Realized Gain or (Loss), Recognized Gain, and Basis of Like-Kind Property Received Caution: If you transferred and received (a) more than one group of like-kind properties, or (b) cash or other (not like-kind) property. see Reporting of multi-asset exchanges in the instructions. Note: Complete lines 12 through 14 only if you gave up property that was not like-kind. Otherwise, go to line 15. 12 Fair market value (FMV) of other property given up. See instructions 12 13 13 Adjusted basis of other property given up..... . . . . . . . 14 16 17 18 19 20 21 22 28 29 30 31 32 26 Enter the number from the upper right corner of your certificate of divestiture. (Do not attach a copy of your certificate. Keep the certificate with your records.)......... 27 Description of divested property 33 34 Gain or (loss) recognized on other property given up. Subtract line 13 from line 12. Report the gain or (loss) in the same manner as if the exchange had been a sale Caution: If the property given up was used previously or partly as a home, see Property used as home in the instructions. Cash received, FMV of other property received, plus net liabilities assumed by other party, reduced (but not below zero) by any exchange expenses you incurred. See instructions FMV of like-kind property you received .. Add lines 15 and 16 37 38 Adjusted basis of like-kind property you gave up, net amounts paid to other party, plus any exchange expenses not used on line 15. See instructions. Realized gain or (loss). Subtract line 18 from line 17 Enter the smaller of line 15 or line 19, but not less than zero Ordinary income under recapture rules. Enter here and on Form 4797, line 16. See instructions.. Subtract line 21 from line 20. If zero or less, enter-O-. If more than zero, enter here and on Schedule D or Form 4797, unless the installment method applies. See instructions... Recognized gain. Add lines 21 and 22 Your social security number 23 24 Deferred gain or (loss). Subtract line 23 from line 19. If a related party exchange, see instructions 25 Basis of like-kind property received. Subtract line 15 from the sum of lines 18 and 23. See instructions Part IV Deferral of Gain From Section 1043 Conflict-of-Interest Sales Note: This part is to be used only by officers or employees of the executive branch of the federal government or judicial officers of the federal government (including certain spouses, minor or dependent children, and trustees as described in section 1043) for reporting nonrecognition of gain under section 1043 on the sale of property to comply with the conflict-of-interest requirements. This part can be used only if the cost of the replacement property is more than the basis of the divested property. Description of replacement property Date divested property was sold (month, day, year) Sales price of divested property. See instructions Basis of divested property Realized gain. Subtract line 31 from line 30 30 31 33 14 15 16 17 18 19 20 21 22 23 24 25 29 Cost of replacement property purchased within 60 days after date of sale Subtract line 33 from line 30. If zero or less, enter-O- 35 Ordinary income under recapture rules. Enter here and on Form 4797, line 10. See instructions 36 Subtract line 35 from line 34. If zero or less, enter -0-. If more than zero, enter here and on Schedule D or Form 4797. See instructions...... 36 Deferred gain. Subtract the sum of lines 35 and 36 from line 32 37 Basis of replacement property. Subtract line 37 from line 33 32 Page 2 34 35 38 Joan Smith and Lisa Stone entered into a qualified exchange of like-kind property. Information about the properties being exchanged is provided below. Data: Parcel 1 property transferred from Joan to Lisa: Fair market value of Parcel 1: $154,000 Joan's adjusted basis in Parcel 1: $127,000 Remaining mortgage on Parcel 1 assumed by Lisa: $31,000 Parcel 2 property transferred from Lisa to Joan: Fair market value of Parcel 2: $123,000 Lisa's adjusted basis in Parcel 2: $112,00 Answer the 3 items below: 1. What is the gain recognized by Joan on the exchange? 2.What is Joan's basis in the new Parcel 2 received by Lisa? 3.Using the info above, fill out IRS FORM 8824 and record Joan's exchange For 8824 Department of the Treasury Internal Revenue Service Name shown on tax retur 2 3 Part I Information on the Like-Kind Exchange Note: Generally, only real property should be described on lines 1 and 2. However, you may describe personal property transferred prior to January 1, 2018, as part of an exchange subject to the like-kind exchange transition rule described in the instructions, and/or real property on lines 1 and 2, if you are filing this form to report the disposition of property exchanged in a previously reported related party like-kind exchange. If the property described on line 1 or line 2 is real or personal property located outside the United States, indicate the country. 1 Description of like-kind property given up 4 6 Date like-kind property given up was originally acquired (month, day, year). Date you actually transferred your property to the other party (month, day, year). 5 Date like-kind property you received was identified by written notice to another party (month, day. year). See instructions for 45-day written identification requirement....... 5 MM/DD/Y Date you actually received the like-kind property from other party (month, day, year). See instructions 6 MM/DD Like-Kind Exchanges (and section 1043 conflict-of-interest sales) Attach to your tax return. Go to www.irs.gov/Form8824 for instructions and the latest information Description of like-kind property received: Part II Related Party Exchange Information 8 Name of related party 11 7 Was the exchange of the property given up or received made with a related party, either directly or indirectly (such as through an intermediary)? See instructions. If "Yes," complete Part II. If "No," go to Part III Yes No Note: Do not file this form if a related party sold property into the exchange, directly or indirectly (such as through an intermediary); that property became your replacement property; and none of the exceptions on line 11 applies to the exchange. Instead, report the disposition of the property as if the exchange had been a sale. If one of the exceptions on line 11 applies to the exchange, complete Part II. a Identifying number Address (no, street, and apt, room, or sulte no.; city or town; state and ZIP code) b OMB No 1545-1190 2021 achmert 109 Relationship to you 3 9 During this tax year (and before the date that is 2 years after the last transfer of property that was part of the exchange), did the related party sell or dispose of any part of the like-kind property received from you (or an intermediary) in the exchange? 4 MM/DD/YYYY ....... Related party's identifying number 10 During this tax year (and before the date that is 2 years after the last transfer of property that was part of the exchange), did you sell or dispose of any part of the like-kind property you received? Yes Yes If both lines 9 and 10 are "No" and this is the year of the exchange, go to Part III. If both lines 9 and 10 are "No" and this is not the year of the exchange, stop here. If either line 9 or line 10 is "Yes," complete Part III and report on this year's tax return the deferred gain or (loss) from line 24 unless one of the exceptions on line 11 applies. If one of the exceptions below applies to the disposition, check the applicable box. The disposition was after the death of either of the related parties. The disposition was an involuntary conversion, and the threat of conversion occurred after the exchange. You can establish to the satisfaction of the IRS that neither the exchange nor the disposition had tax avoidance as one of its principal purposes. If this box is checked, attach an explanation. See instructions. For Paperwork Reduction Act Notice, see the instructions. Cat No. 12311A Form 8824 021) No No Form 24 (2021) Name shown on tax retum. Do not enter name and social security number if shown on other side 15 Part III Realized Gain or (Loss), Recognized Gain, and Basis of Like-Kind Property Received Caution: If you transferred and received (a) more than one group of like-kind properties, or (b) cash or other (not like-kind) property. see Reporting of multi-asset exchanges in the instructions. Note: Complete lines 12 through 14 only if you gave up property that was not like-kind. Otherwise, go to line 15. 12 Fair market value (FMV) of other property given up. See instructions 12 13 13 Adjusted basis of other property given up..... . . . . . . . 14 16 17 18 19 20 21 22 28 29 30 31 32 26 Enter the number from the upper right corner of your certificate of divestiture. (Do not attach a copy of your certificate. Keep the certificate with your records.)......... 27 Description of divested property 33 34 Gain or (loss) recognized on other property given up. Subtract line 13 from line 12. Report the gain or (loss) in the same manner as if the exchange had been a sale Caution: If the property given up was used previously or partly as a home, see Property used as home in the instructions. Cash received, FMV of other property received, plus net liabilities assumed by other party, reduced (but not below zero) by any exchange expenses you incurred. See instructions FMV of like-kind property you received .. Add lines 15 and 16 37 38 Adjusted basis of like-kind property you gave up, net amounts paid to other party, plus any exchange expenses not used on line 15. See instructions. Realized gain or (loss). Subtract line 18 from line 17 Enter the smaller of line 15 or line 19, but not less than zero Ordinary income under recapture rules. Enter here and on Form 4797, line 16. See instructions.. Subtract line 21 from line 20. If zero or less, enter-O-. If more than zero, enter here and on Schedule D or Form 4797, unless the installment method applies. See instructions... Recognized gain. Add lines 21 and 22 Your social security number 23 24 Deferred gain or (loss). Subtract line 23 from line 19. If a related party exchange, see instructions 25 Basis of like-kind property received. Subtract line 15 from the sum of lines 18 and 23. See instructions Part IV Deferral of Gain From Section 1043 Conflict-of-Interest Sales Note: This part is to be used only by officers or employees of the executive branch of the federal government or judicial officers of the federal government (including certain spouses, minor or dependent children, and trustees as described in section 1043) for reporting nonrecognition of gain under section 1043 on the sale of property to comply with the conflict-of-interest requirements. This part can be used only if the cost of the replacement property is more than the basis of the divested property. Description of replacement property Date divested property was sold (month, day, year) Sales price of divested property. See instructions Basis of divested property Realized gain. Subtract line 31 from line 30 30 31 33 14 15 16 17 18 19 20 21 22 23 24 25 29 Cost of replacement property purchased within 60 days after date of sale Subtract line 33 from line 30. If zero or less, enter-O- 35 Ordinary income under recapture rules. Enter here and on Form 4797, line 10. See instructions 36 Subtract line 35 from line 34. If zero or less, enter -0-. If more than zero, enter here and on Schedule D or Form 4797. See instructions...... 36 Deferred gain. Subtract the sum of lines 35 and 36 from line 32 37 Basis of replacement property. Subtract line 37 from line 33 32 Page 2 34 35 38 Joan Smith and Lisa Stone entered into a qualified exchange of like-kind property. Information about the properties being exchanged is provided below. Data: Parcel 1 property transferred from Joan to Lisa: Fair market value of Parcel 1: $154,000 Joan's adjusted basis in Parcel 1: $127,000 Remaining mortgage on Parcel 1 assumed by Lisa: $31,000 Parcel 2 property transferred from Lisa to Joan: Fair market value of Parcel 2: $123,000 Lisa's adjusted basis in Parcel 2: $112,00 Answer the 3 items below: 1. What is the gain recognized by Joan on the exchange? 2.What is Joan's basis in the new Parcel 2 received by Lisa? 3.Using the info above, fill out IRS FORM 8824 and record Joan's exchange

Expert Answer:

Related Book For

Income Tax Fundamentals 2013

ISBN: 9781285586618

31st Edition

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

Posted Date:

Students also viewed these law questions

-

The following additional information is available for the Dr. Ivan and Irene Incisor family from Chapters 1-5. Ivan's grandfather died and left a portfolio of municipal bonds. In 2012, they pay Ivan...

-

Find a vector parametrization of the intersection of the surfaces x 2 + y 4 + 2z 3 = 6 and x = y 2 in R 3 .

-

Sara receives $5,500 per year scholarship to attend the state university .Sarah spends $4,000 for tuition, $500 for required textbooks and $1,000 for room and board. Sara also has a part time job on...

-

What does a plot of the probability distribution of outcomes show a decision maker about an assets risk?

-

Show that for a European call or put on a non-dividend-paying stock = N' (d1) SoT SN' (d) -Ke-T N(d2). 2T

-

The manager of a pizza chain in Albuquerque, New Mexico, wants to determine the average size of their advertised 16-inch pizzas. She takes a random sample of 25 pizzas and records their mean and...

-

Number of units sold Selling price per unit Unit cost of goods sold Variable selling expense per unit Total fixed selling expense Variable administrative expense per unit Total fixed administrative...

-

(i) Calculate the double bond equivalents (DBE) for each molecule. (ii) Assign the 1H NMR spectra completely, rationalise the number of peaks, relative integral, their multiplicity or splitting...

-

During the holidays, Kim makes and sells candy. Last holiday season, she made a profit of $10 on each box of candy she sold, and she sold 300 boxes. Based on some experimentation she did, Kim...

-

Southern Florida is known as the "Lightning Capital" of the U.S. It averages 25.1 lightning strikes per year per square mile with a standard deviation of 5.25. A meteorologist believes the number of...

-

Explain and apply the Scarcity Principle, which says that having more of any good thing necessarily requires having less of something else. Explain and apply the Cost-Benefit Principle, which says...

-

Attached is the question Refer to the reading by Einav and Finkelstein: "Adverse Selection: Theory and Empirics in Pictures." Take the case in which all individuals are risk averse and where marginal...

-

The Speedy Oil Change Company advertised a 15-minute wait for anoil change. A sample of 23 oil changes showed a mean time of 13.5minutes and a standard deviation of 4.3 minutes. At the 5% level...

-

18 IVT e(-x) = In x Use the Intermediate Value Theorem to verify there is a solution on the interval (1,2).

-

A business had revenues of $280,000 and operating expenses of $315,000. Did the business (a) Incur a net loss (b) Realize net income?

-

John Fuji (age 37) moved from California to Washington in December 2011. He lives at 468 Cameo Street, Yakima, WA 98901. John's Social Security number is 571-78-5974 and he is single. His earnings...

-

Dr. Ivan I. Incisor and his wife Irene are married and file a joint return for 2012. Ivan's Social Security number is 477-34-4321 and he is 48 years old. Irene I. Incisor's Social Security number is...

-

On September 14, 2012, Jay purchased a passenger automobile that is used 75 percent in his accounting business. The automobile has a basis for depreciation purposes of $35,000, and Jay uses the...

-

Given the four criteria necessary for a sale to be complete, which of the following is not one of those conditions? 1. Delivery has occurred or services rendered. 2. Cash has been collected. 3. The...

-

What is the difference between a business and a pure charity? Between a business and a governmental agency?

-

Sketch the \(P-V\) phase diagram for helium-4 using the sketch of the \(P-T\) phase diagram in Figure 4.3. Ps P S superfluid Pe T To T FIGURE 4.3 Sketch of the P-T phase diagram for helium-4. The...

Study smarter with the SolutionInn App