Question: For each substantive procedure, select the assertion(s) for which the substantive procedure is designed to detect misstatements. You may use an assertion below more than

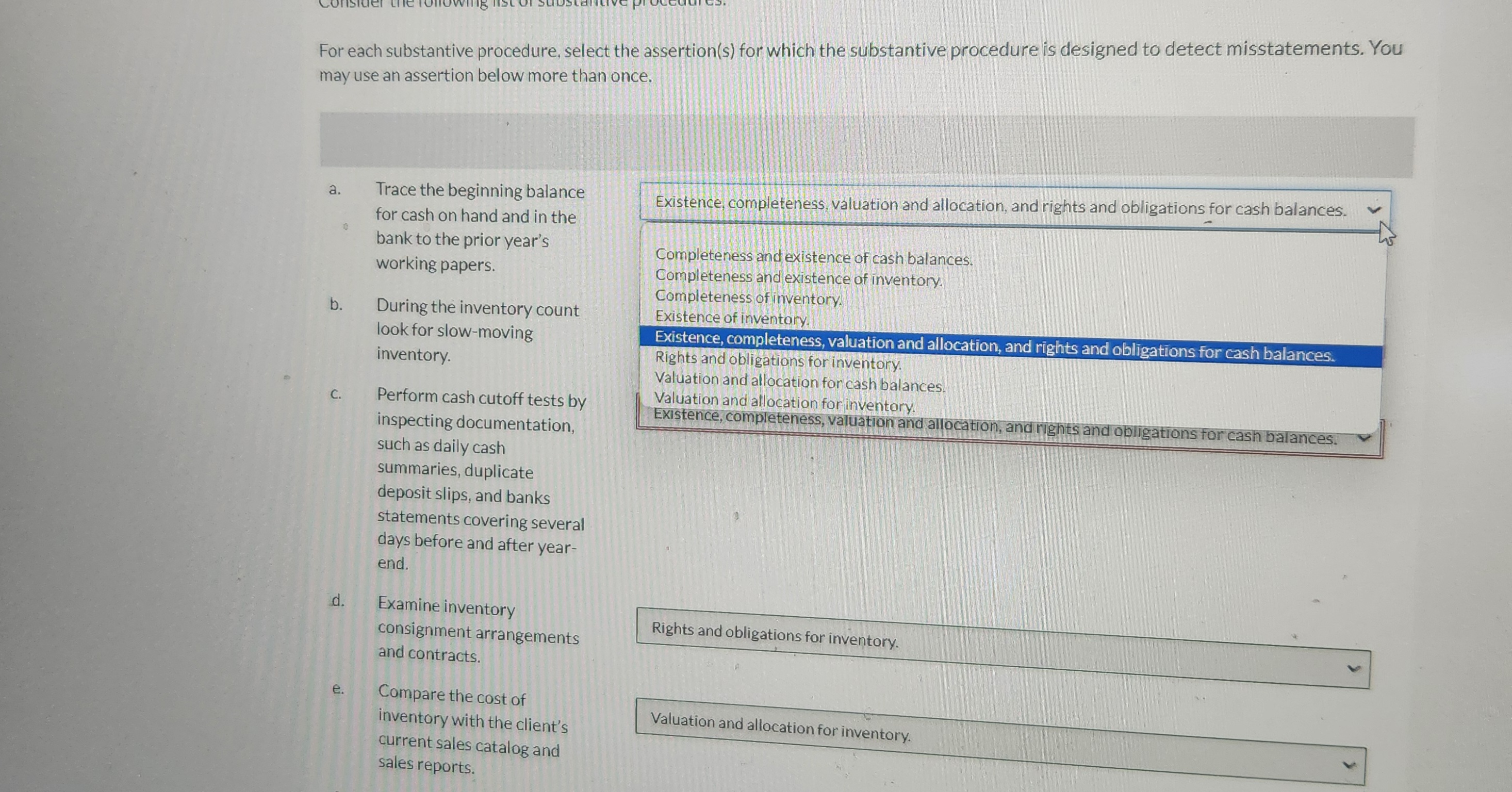

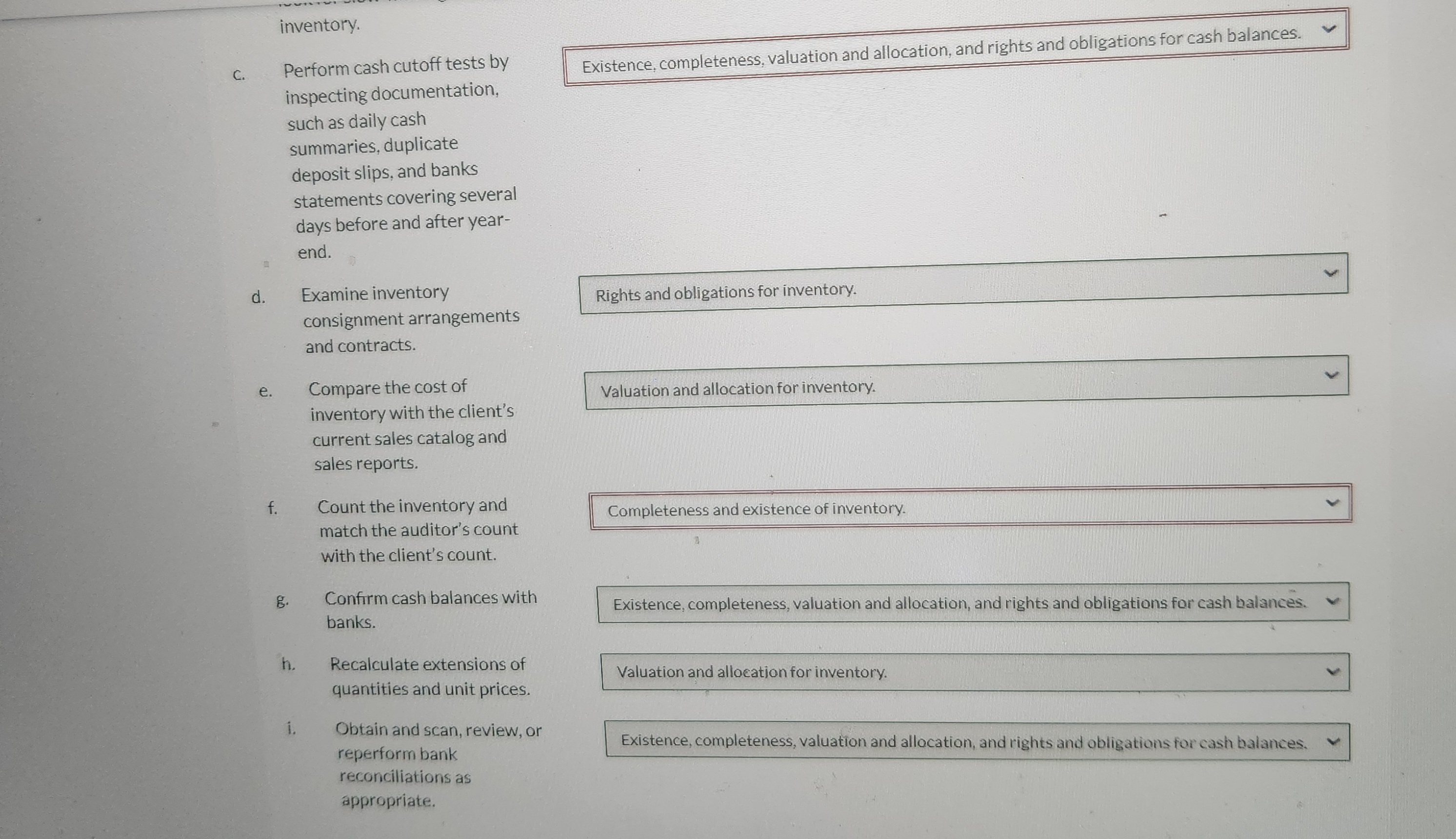

For each substantive procedure, select the assertion(s) for which the substantive procedure is designed to detect misstatements. You may use an assertion below more than once. a. Trace the beginning balance Existence, completeness valuation and allocation, and rights and obligations for cash balances. for cash on hand and in the bank to the prior year's Completeness and existence of cash balances. working papers. Completeness and existence of inventory. Completeness of inventory. b. During the inventory count Existence of inventory. look for slow-moving Existence, completeness, valuation and allocation, and rights and obligations for cash balances. inventory. Rights and obligations for inventory. Valuation and allocation for cash balances. C. Perform cash cutoff tests by Valuation and allocation for inventory. Existence, completeness, valuation and allocation, and rights and obligations for cash balances. inspecting documentation, such as daily cash summaries, duplicate deposit slips, and banks statements covering several days before and after year- end. d. Examine inventory consignment arrangements Rights and obligations for inventory. and contracts. e. Compare the cost of inventory with the client's Valuation and allocation for inventory. current sales catalog and sales reports.inventory. C. Perform cash cutoff tests by Existence, completeness, valuation and allocation, and rights and obligations for cash balances. inspecting documentation, such as daily cash summaries, duplicate deposit slips, and banks statements covering several days before and after year- end. d. Examine inventory Rights and obligations for inventory. consignment arrangements and contracts. e. Compare the cost of Valuation and allocation for inventory. inventory with the client's current sales catalog and sales reports. f . Count the inventory and Completeness and existence of inventory. match the auditor's count with the client's count. B. Confirm cash balances with banks. Existence, completeness, valuation and allocation, and rights and obligations for cash balances. h . Recalculate extensions of quantities and unit prices. Valuation and allocation for inventory. i. Obtain and scan, review, or reperform bank Existence, completeness, valuation and allocation, and rights and obligations for cash balances. reconciliations as appropriate

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!