Question: For model Y = XB + e, with E(e) = 0 and Cov(e) = variance*omega. Solve the following question manually and show your process. 0.2.

For model Y = XB + e, with E(e) = 0 and Cov(e) = variance*omega. Solve the following question manually and show your process.

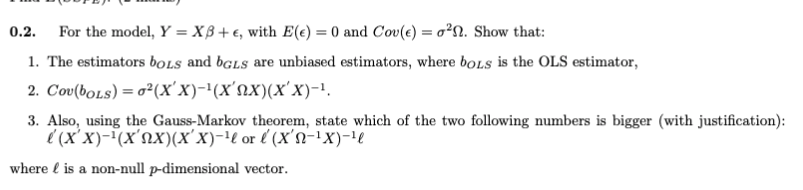

0.2. For the model, Y = X8 + 6, with E() =0 and Cov(e) = 020. Show that: 1. The estimators boys and bars are unbiased estimators, where boys is the OLS estimator, 2. Cou(boLS) = "(XX)-(X'nX)(X'X)-1. 3. Also, using the Gauss-Markov theorem, state which of the two following numbers is bigger (with justification): ('(Xx)-(X'Sx)(X'X)-le or /(X'9-1x)-1/ where { is a non-null p-dimensional vector

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock