Question: For Part 2, how to value put option using portfolio replication method? (a) (i) A call option on the stock of Bovisand has an exercise

For Part 2, how to value put option using portfolio replication method?

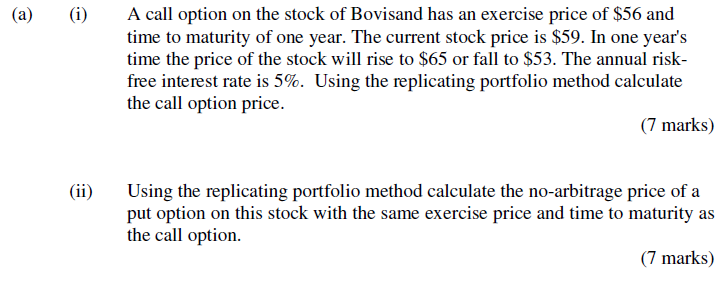

(a) (i) A call option on the stock of Bovisand has an exercise price of $56 and time to maturity of one year. The current stock price is $59. In one year's time the price of the stock will rise to $65 or fall to $53. The annual risk- free interest rate is 5%. Using the replicating portfolio method calculate the call option price. (7 marks) (ii) Using the replicating portfolio method calculate the no-arbitrage price of a put option on this stock with the same exercise price and time to maturity as the call option. (7 marks) (a) (i) A call option on the stock of Bovisand has an exercise price of $56 and time to maturity of one year. The current stock price is $59. In one year's time the price of the stock will rise to $65 or fall to $53. The annual risk- free interest rate is 5%. Using the replicating portfolio method calculate the call option price. (7 marks) (ii) Using the replicating portfolio method calculate the no-arbitrage price of a put option on this stock with the same exercise price and time to maturity as the call option. (7 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts