Question: For part (b) please! The current price of a non-dividend paying stock is $100. You also collect additional information on a series of European options

For part (b) please!

For part (b) please!

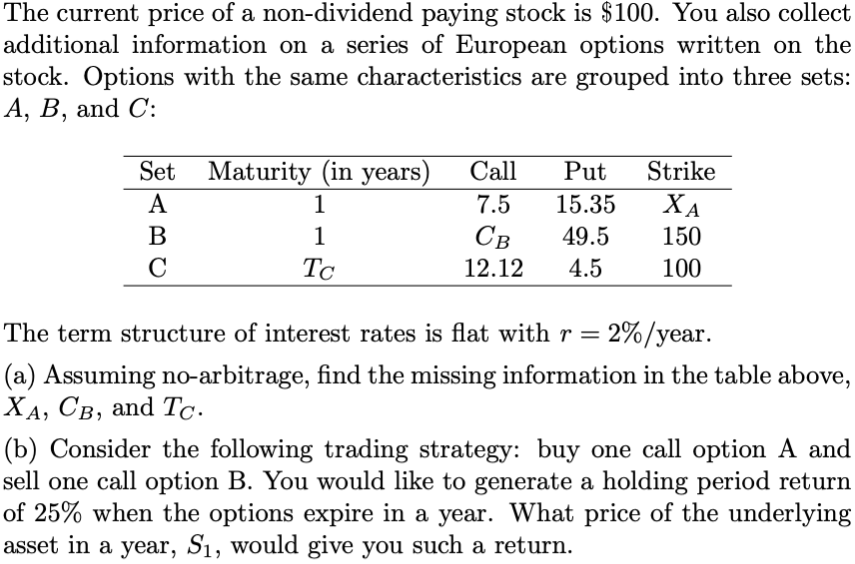

The current price of a non-dividend paying stock is $100. You also collect additional information on a series of European options written on the stock. Options with the same characteristics are grouped into three sets: A, B, and C: Set Maturity (in years) A 1 B 1 c Call 7.5 12.12 Put 15.35 49.5 4.5 Strike XA 150 100 The term structure of interest rates is flat with r = 2%/year. (a) Assuming no-arbitrage, find the missing information in the table above, XA, Cb, and Tc. (b) Consider the following trading strategy: buy one call option A and sell one call option B. You would like to generate a holding period return of 25% when the options expire in a year. What price of the underlying asset in a year, Si, would give you such a return

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts