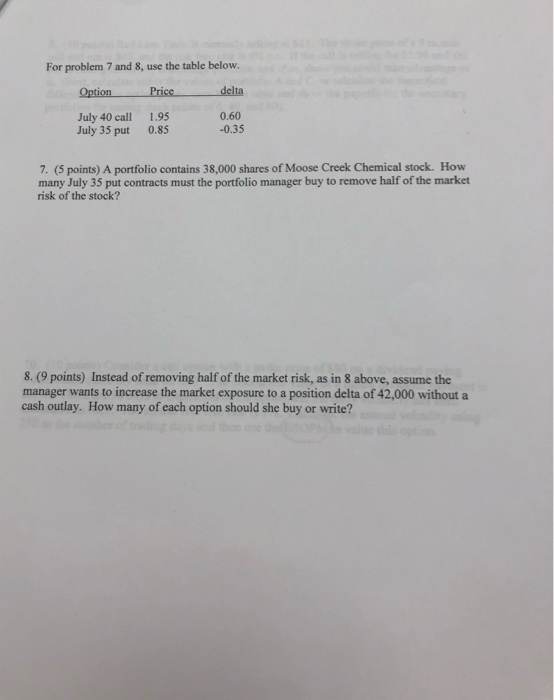

Question: For problem 7 and 8, use the table below. Option Price delta July 40 call July 35 put 1.95 0.85 0.60 -0.35 7. (5 points)

For problem 7 and 8, use the table below. Option Price delta July 40 call July 35 put 1.95 0.85 0.60 -0.35 7. (5 points) A portfolio contains 38,000 shares of Moose Creek Chemical stock. How many July 35 put contracts must the portfolio manager buy to remove half of the market risk of the stock? 8. (9 points) Instead of removing half of the market risk, as in 8 above, assume the manager wants to increase the market exposure to a position delta of 42,000 without a cash outlay. How many of each option should she buy or write? in

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock