Question: For Q 8 - Q 1 0 , consider a market neutral hedge funds invested in the Betting Against Beta strategy. The following assets can

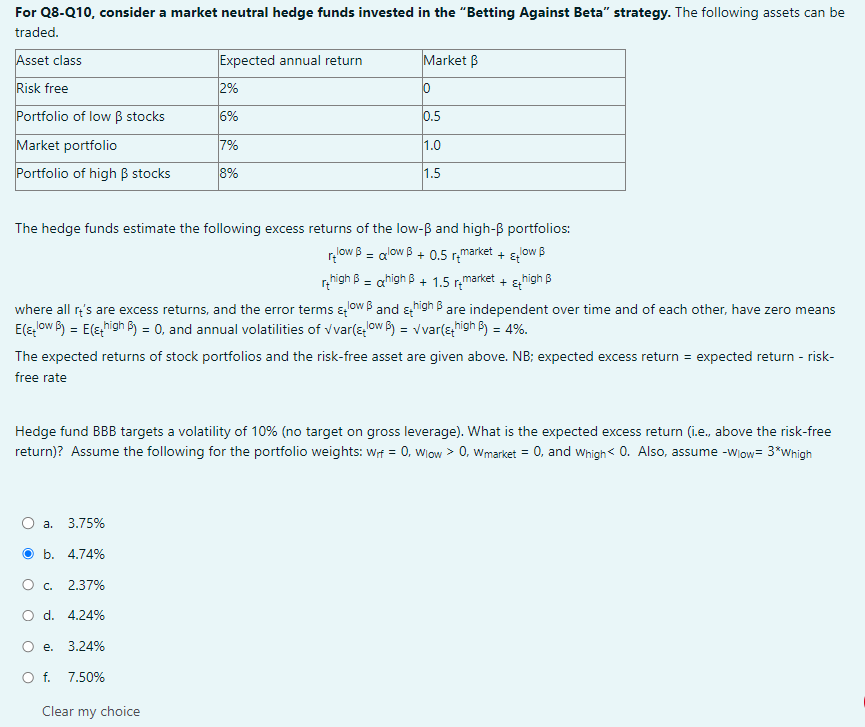

For QQ consider a market neutral hedge funds invested in the "Betting Against Beta" strategy. The following assets can be

traded.

The hedge funds estimate the following excess returns of the low and high portfolios:

where all s are excess returns, and the error terms and high are independent over time and of each other, have zero means

and annual volatilities of Vvar

The expected returns of stock portfolios and the riskfree asset are given above. NB; expected excess return expected return risk

free rate

Hedge fund BBB targets a volatility of no target on gross leverage What is the expected excess return ie above the riskfree

return Assume the following for the portfolio weights: and Also, assume

a

b

c

d

e

f

Clear my choice

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock