Question: *For studying purposes Consider an ARMA(1,1) process yt = Bot pyt-1 + Et + 01Et-1, (1) for t = 1, 2, . .. , T,

*For studying purposes

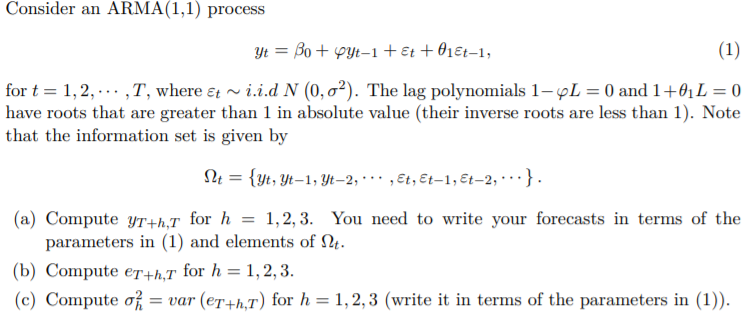

Consider an ARMA(1,1) process yt = Bot pyt-1 + Et + 01Et-1, (1) for t = 1, 2, . .. , T, where at ~ i.i.d N (0, o'). The lag polynomials 1-41 = 0 and 1+01L = 0 have roots that are greater than 1 in absolute value (their inverse roots are less than 1). Note that the information set is given by It = {yt, yt-1, yt-2, " "' , Et, Et-1, Et-2, "..} (a) Compute yrth,T for h = 1,2,3. You need to write your forecasts in terms of the parameters in (1) and elements of 2t. (b) Compute erth,T for h = 1, 2, 3. (c) Compute of = var (erth,T) for h = 1, 2,3 (write it in terms of the parameters in (1))

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock