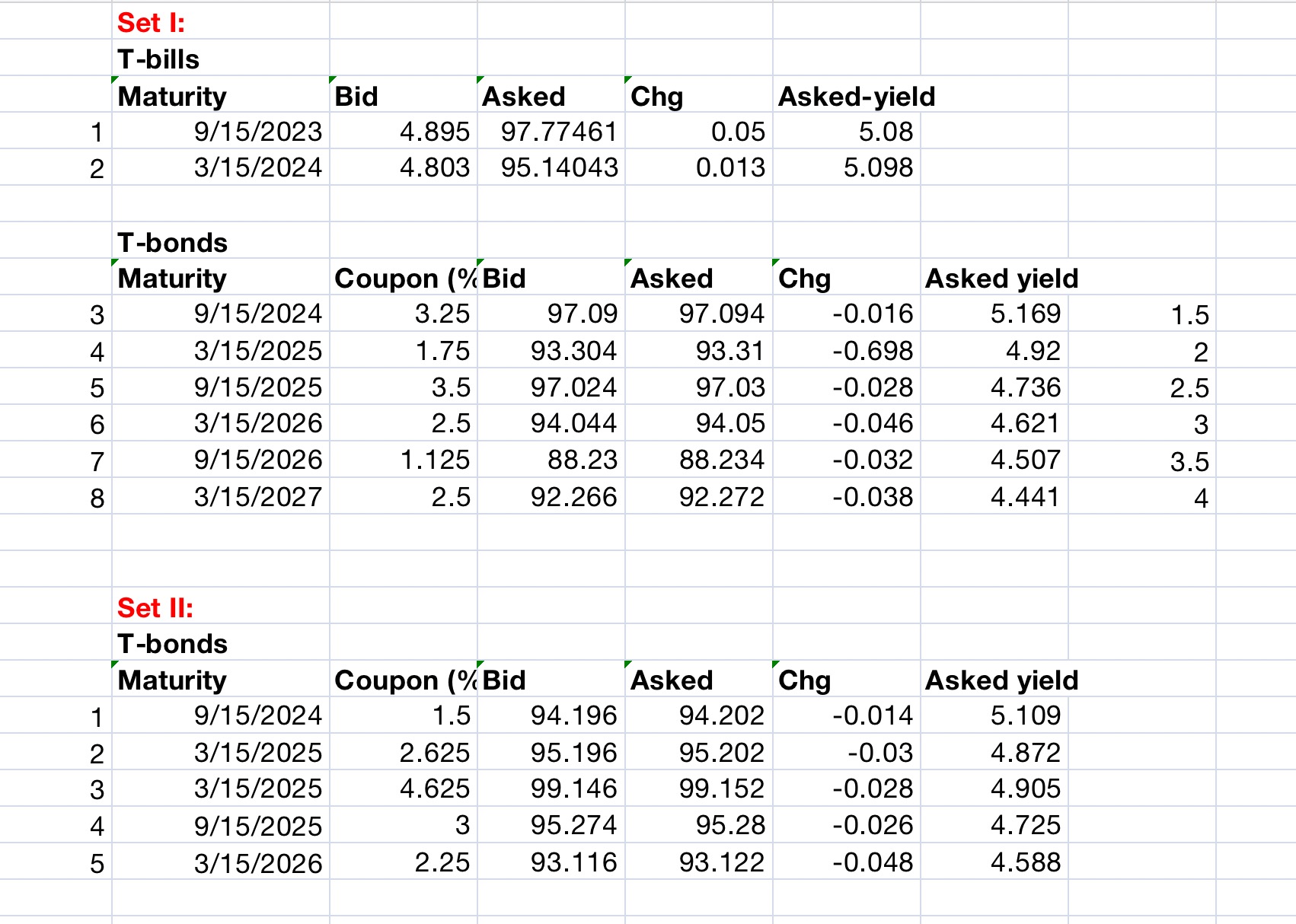

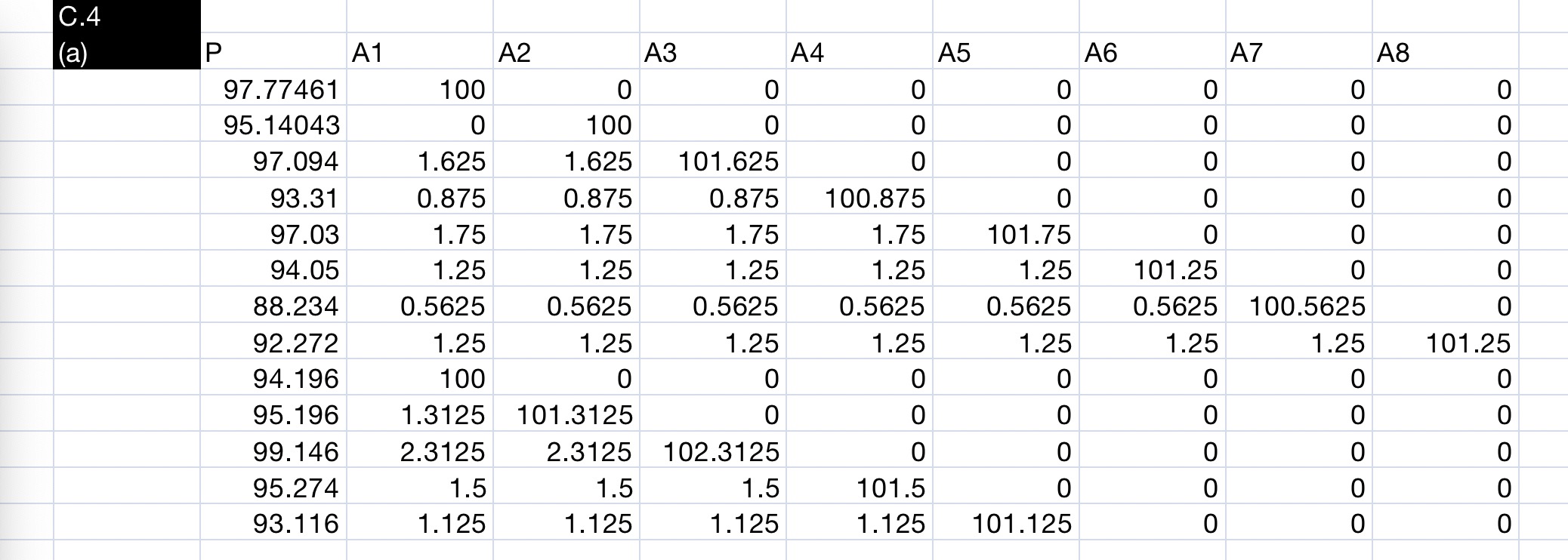

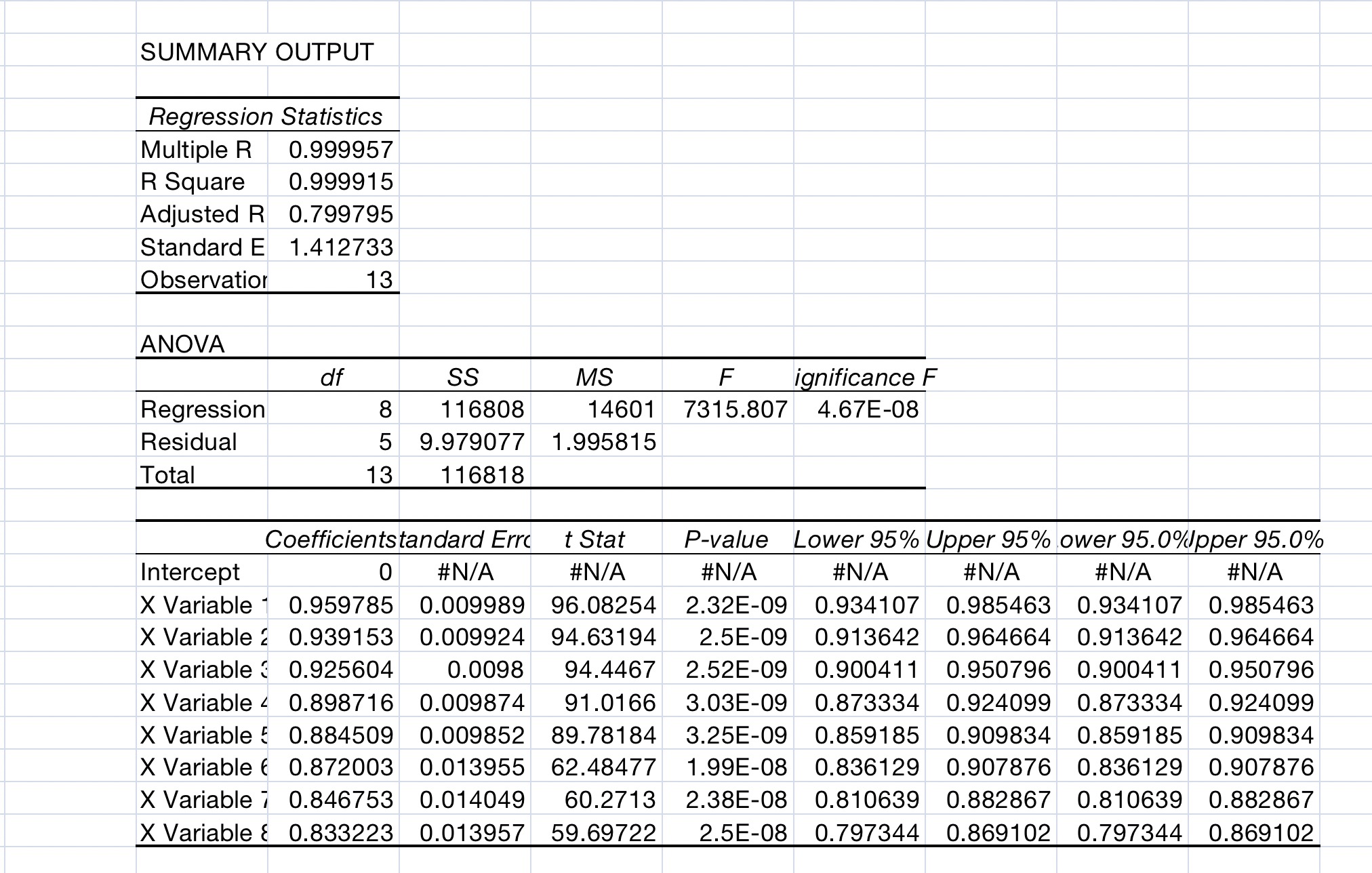

Question: For this part, use first and second set, i.e. total of 12 Treasuries 4. a)Using regression methods, extract zero coupon bonds. (Note: Force the intercept

For this part, use first and second set, i.e. total of 12 Treasuries 4.

a)Using regression methods, extract zero coupon bonds. (Note: Force the intercept to zero in the regression).

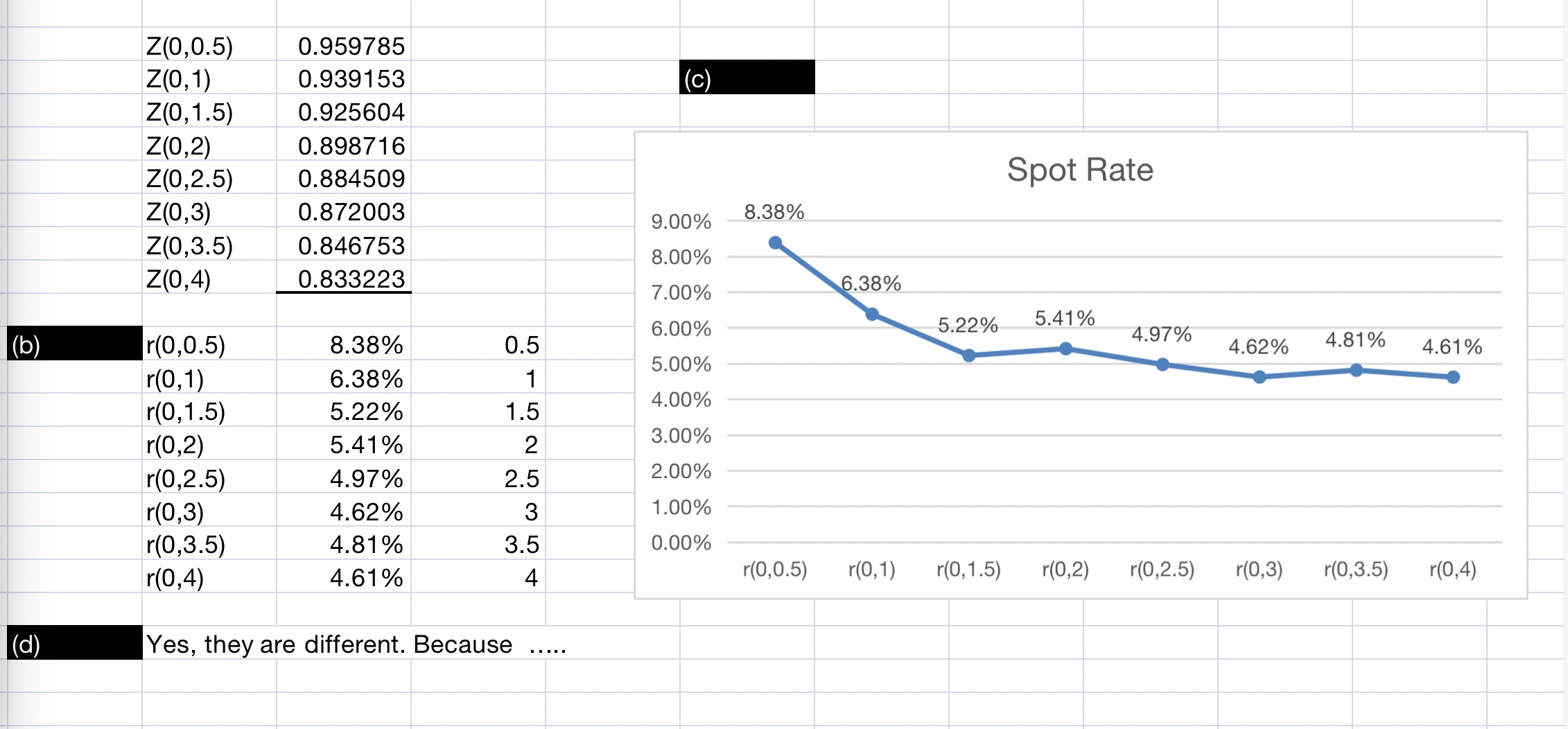

b) Calculate 6 month spot rates

c) Plot the spot rate curve

All the above steps have been completed. See attachedimagesl for details

My question:

d) Compare the spot rates with the ones you found by bootstrapping. Are they different? Why? Why not?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock