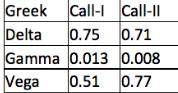

For two European call options, Call-l and Call-Il on a non-dividend-paying stock, you are given: Suppose you

Fantastic news! We've Found the answer you've been seeking!

Question:

For two European call options, Call-l and Call-Il on a non-dividend-paying stock, you are given:

Suppose you just sold 500 units of Call-1.

Using units of Call-II and stock, you delta-hedge and gamma-hedge your position in Call-L What is the total Vega for the call options (both long and short) in your portfolio?

Expert Answer:

Related Book For

Principles of Accounting

ISBN: 978-1133626985

12th edition

Authors: Belverd E. Needles, Marian Powers and Susan V. Crosson

Posted Date: