Question: Formally respond to their reply with one paragraph Their reply: I'm a big advocate/believer that information will rarely be useful in isolation as you can

Formally respond to their reply with one paragraph

Their reply:

I'm a big advocate/believer that information will rarely be useful in isolation as you can probably tell. For example, if I was to review a balance sheet that had a cash balance of $2,000,000, one might immediately think that's awesome. I would be wondering what this company's plant assets reveal. Do they lease their buildings or do they own them? $2,000,000 is a lot of cash to lie around without investing in so should they invest in buildings (if they are leasing) or even just invest in bonds?

The same might be able to be said with the tabled information for the company we are analyzing. Are there any accounts that you can use in isolation to make informed decisions?

My post:

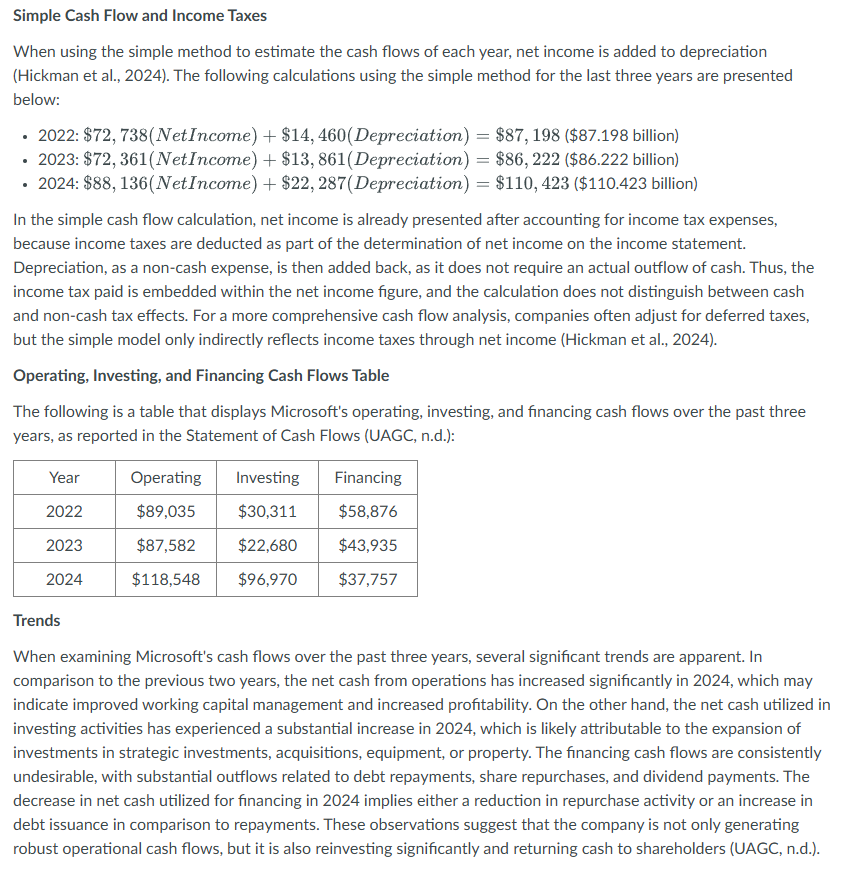

Simple Cash Flow and Income Taxes When using the simple method to estimate the cash flows of each year, net income is added to depreciation (Hickman et al., 2024). The following calculations using the simple method for the last three years are presented below: + 2022: $72, 738( NetIncome) + $14, 460( Depreciation) = $87, 198 ($87.198 billion) 2023: $72, 361(NetIncome) + $13, 861( Depreciation) = $86, 222 ($86.222 billion) + 2024: $88, 136(NetIncome) + $22, 287( Depreciation) = $110, 423 ($110.423 billion) In the simple cash flow calculation, net income is already presented after accounting for income tax expenses, because income taxes are deducted as part of the determination of net income on the income statement. Depreciation, as a non-cash expense, is then added back, as it does not require an actual outflow of cash. Thus, the income tax paid is embedded within the net income figure, and the calculation does not distinguish between cash and non-cash tax effects. For a more comprehensive cash flow analysis, companies often adjust for deferred taxes, but the simple model only indirectly reflects income taxes through net income (Hickman et al., 2024). Operating, Investing, and Financing Cash Flows Table The following is a table that displays Microsoft's operating, investing, and financing cash flows over the past three years, as reported in the Statement of Cash Flows (UAGC, n.d.): Year Operating Investing Financing $89,035 $30,311 $58,876 $87,582 $22,680 $43,935 Trends When examining Microsoft's cash flows over the past three years, several significant trends are apparent. In comparison to the previous two years, the net cash from operations has increased significantly in 2024, which may indicate improved working capital management and increased profitability. On the other hand, the net cash utilized in investing activities has experienced a substantial increase in 2024, which is likely attributable to the expansion of investments in strategic investments, acquisitions, equipment, or property. The financing cash flows are consistently undesirable, with substantial outflows related to debt repayments, share repurchases, and dividend payments. The decrease in net cash utilized for financing in 2024 implies either a reduction in repurchase activity or an increase in debt issuance in comparison to repayments. These observations suggest that the company is not only generating robust operational cash flows, but it is also reinvesting significantly and returning cash to shareholders (UAGC, n.d.). Explain this statement: Depreciation provides a tax shield on income. The value of the depreciation tax shield decreases in line with the reduction in the corporate income tax rate. The tax shield is determined by multiplying the corporate tax rate by the depreciation expense. A reduced tax rate results in a lower tax savings per dollar of depreciation expense, which in turn diminishes the overall benefit to the company's after-tax cash flows. This potential decrease in value may influence investment decisions involving depreciable assets (Hickman et al., 2024). Explain this statement: If the corporate income tax rate decreases, the value of the depreciation tax shield goes down. The value of the depreciation tax shield decreases in line with the reduction in the corporate income tax rate. The tax shield is determined by multiplying the corporate tax rate by the depreciation expense. A reduced tax rate results in a lower tax savings per dollar of depreciation expense, which in turn diminishes the overall benefit to the company's after-tax cash flows. This potential decrease in value may influence investment decisions involving depreciable assets (Hickman et al., 2024). Principles Incremental, after-tax cash flows are essential for assessing the viability of investment projects, as they provide the owners with the actual cash benefit after taxes are taken into account. The emphasis is placed on the changes that are directly attributable to the investment decision when evaluating these financial flows. This includes taking into account only the cash flows that are a direct result and disregarding any cash flows that would have occurred regardless of the investment (Hickman et al., 2024). Taxes are a critical element because they reduce the earnings available to the owners, thereby affecting the net cash flow. Consequently, it is imperative to determine the after-tax effect on financial flows, which necessitates an understanding of taxable income. Depreciation is a critical factor in this context; despite its non-cash charge, it reduces taxable income, thereby reducing the tax liability and, as a result, increasing cash flow through the tax shield it offers (Hickman et al., 2024). This methodology is consistent with the accounting principle of matching, which guarantees that expenses incurred during the utilization of assets with a long lifespan are recognized uniformly throughout the period of use (Hickman et al., 2024). Question How might significant fluctuations in working capital components (such as accounts receivable or payable) affect the reliability of operating cash flow as an indicator of company performance

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!