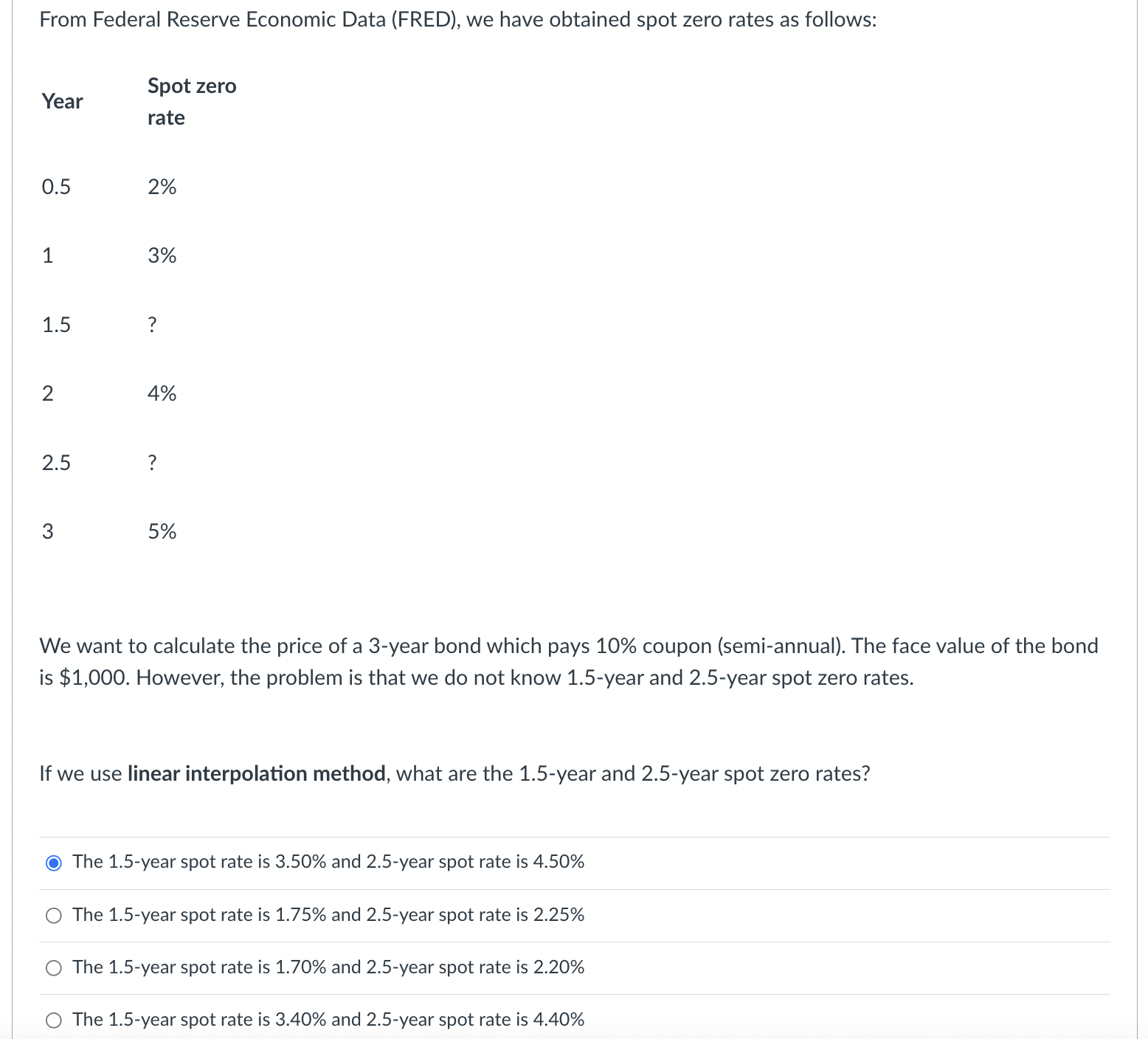

Question: From Federal Reserve Economic Data ( FRED ) , we have obtained spot zero rates as follows: Year Spot zero rate 0 . 5 2

From Federal Reserve Economic Data FRED we have obtained spot zero rates as follows:

Year

Spot zero

rate

We want to calculate the price of a year bond which pays coupon semiannual The face value of the bond

is $ However, the problem is that we do not know year and year spot zero rates.

If we use linear interpolation method, what are the year and year spot zero rates?

The year spot rate is and year spot rate is

The year spot rate is and year spot rate is

The year spot rate is and year spot rate is

The year spot rate is and year spot rate is

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock