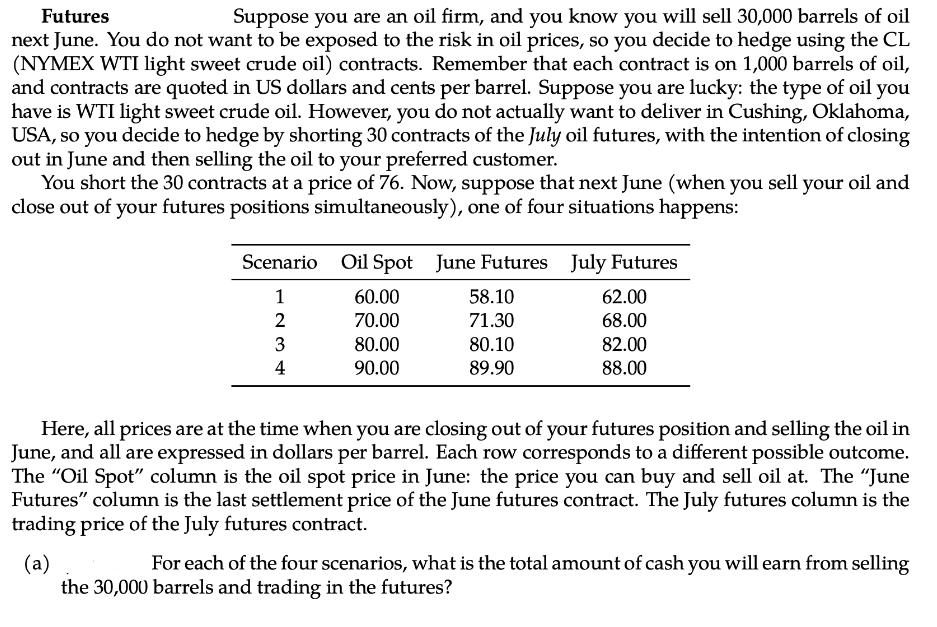

Futures Suppose you are an oil firm, and you know you will sell 30,000 barrels of...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Corporate Finance

ISBN: 9781265533199

13th International Edition

Authors: Stephen Ross, Randolph Westerfield, Jeffrey Jaffe

Posted Date: