Question: Given that npx = 0.3, npy = 0.4, npz = 0.6, find the probability that, of the lives (x), (y) and (z), (a) none will

Given that npx = 0.3, npy = 0.4, npz = 0.6, find the probability that, of the lives (x), (y) and

(z),

(a) none will survive n years

(b) exactly one will survive n years

(c) at least one will survive n years.

Prove that

(IA)xy = axy ? d.(Ia)xy

Express in terms of px, py, and pz the probabilities that, of three lives (x), (y) and (z),

(a) all three will survive one year

(b) at least one will survive one year

(c) exactly two will survive one year

(d) at least two will survive one year

11.4 Derive the formula

exy = E(K) = X?

t=1

tpxy where K = integer part of T (T = min{T1, T2})

using P r{K = k} = k|qxy.

Evaluate A75:75 on the basis of A1967 ? 70 ultimate at 4% interest.

The probability that at least one of three lives aged 60 will survive to age 65 is eight times the

probability that exactly one will survive to age 65. Assuming that the 3 lives are independent

and subject to the same table of mortality, find the probability that exactly one life will

survive to age 65.

(i) Define tpxy and show that tpxy = tpx + tpy ? tpxy

(ii) Hence, or otherwise, show that axy = ax + ay ? axy

12 years ago a man then aged 48 effected a without profits whole life assurance for 10,000

(payable at the end of the year of death) by annual premiums. The premium now due is

unpaid. He now wishes to alter the policy so that the same sum assured will be payable at

the end of the year of the first death of himself and his wife, who is 4 years older than himself.

Calculate the revised office annual premium, ceasing on the first death, if the office uses the

following basis for premiums and reserves.

mortality: A1967-70 ultimate, rated down 4 years for female lives,

interest: 4% per annum,

expenses: 3% of all office premiums including the first, with additional initial expenses of 1 1

2%

of the sum assured. (This additional initial expense is not charged again on the conversion of

an existing policy, providing that the sum assured does not increase.)

Consider the random variable L equal to the present value of 1 payable immediately on

(i) the first death of (x) and (y), and

(ii) the second death, in each case at a given rate of interest i p.a.

Show that, in case (i),

var(L) = A?

xy ? (A

xy)

2

where ?

indicates a rate of interest of 2i+i

2 p.a., and give a corresponding result for case (ii).

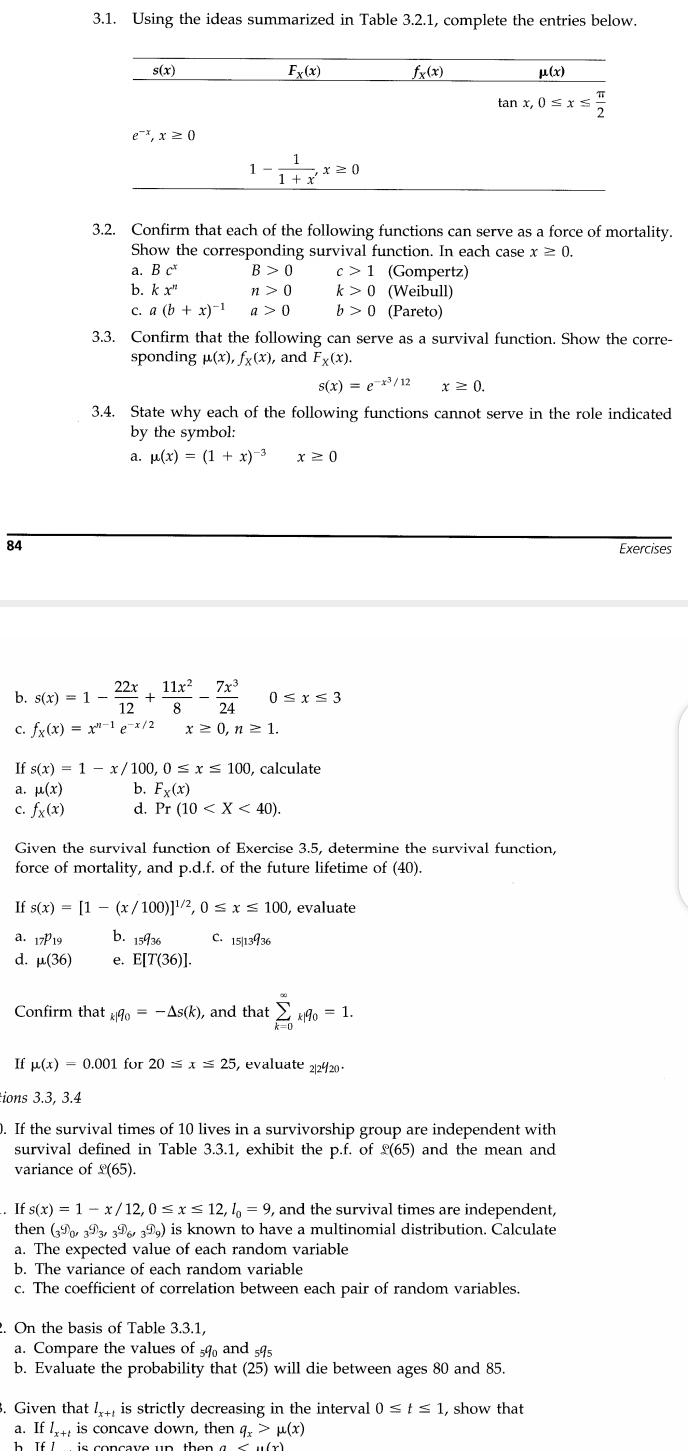

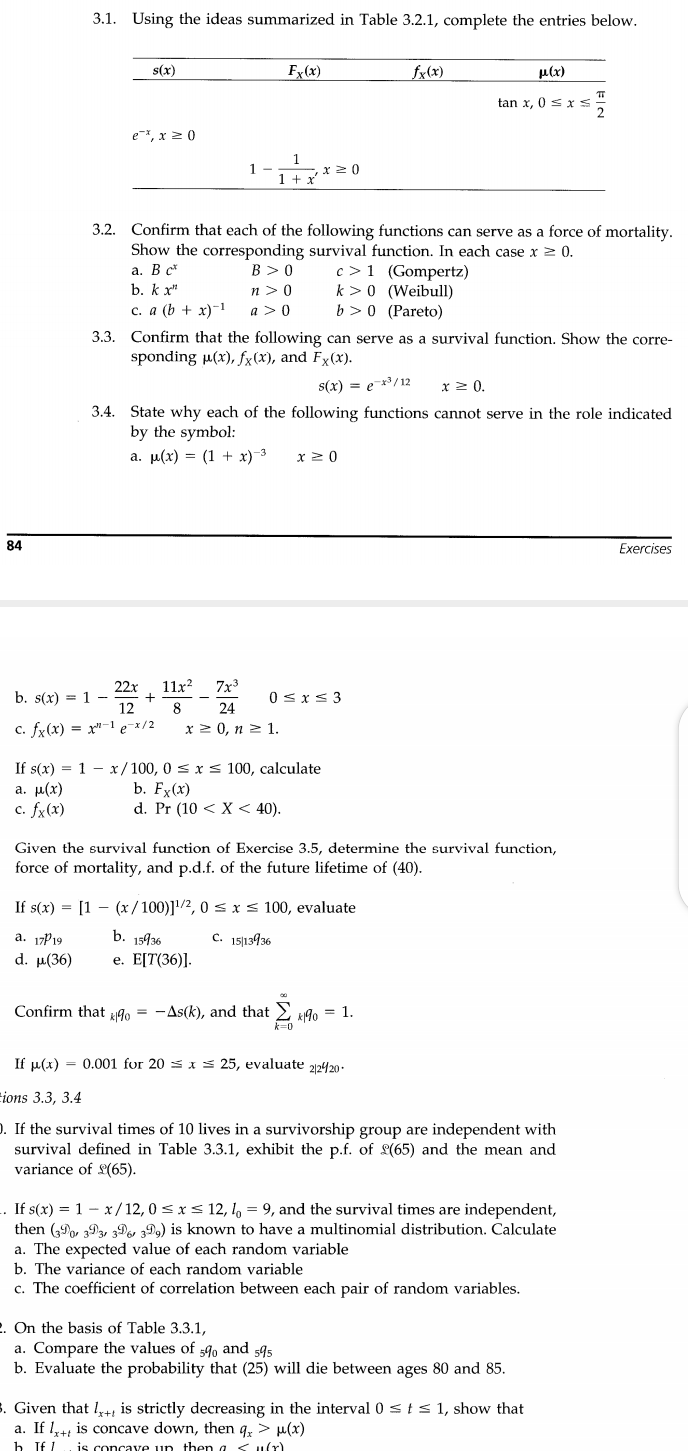

3.1. Using the ideas summarized in Table 3.2.1, complete the entries below. s(x) Fx(x) fx (x) p.(x) tan x, O s x s ed, x20 1 1 - 1 + x' ,x20 3.2. Confirm that each of the following functions can serve as a force of mortality. Show the corresponding survival function. In each case x 2 0. a. BC B >0 c > 1 (Gompertz) b. k x n > 0 k > 0 (Weibull) c. a (b + x) -1 a>0 b > 0 (Pareto) 3.3. Confirm that the following can serve as a survival function. Show the corre- sponding p(x), fx(x), and Fx(x). s(x) = ex/ 12 x 2 0. 3.4. State why each of the following functions cannot serve in the role indicated by the symbol: a. p(x) = (1 + x)-3 x20 84 Exercises b. s(x) = 1 - 22x 11x2 7x3 12 8 24 OSx=3 c. fx(x) = x-le x/2 x 20, n > 1. If s(x) = 1 - x/100, 0 = x = 100, calculate a. p(x) b. Fx(x) c. fx(x) d. Pr (10 u(x)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts