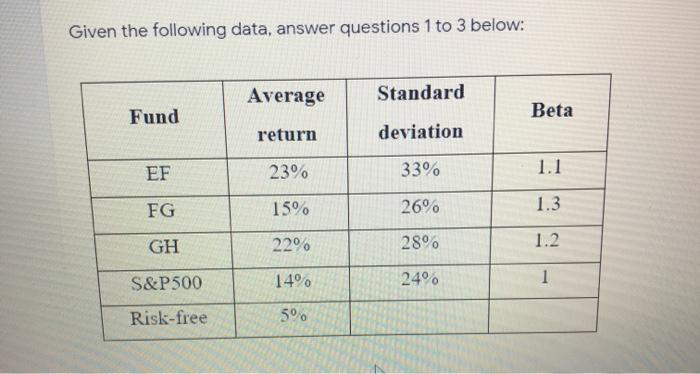

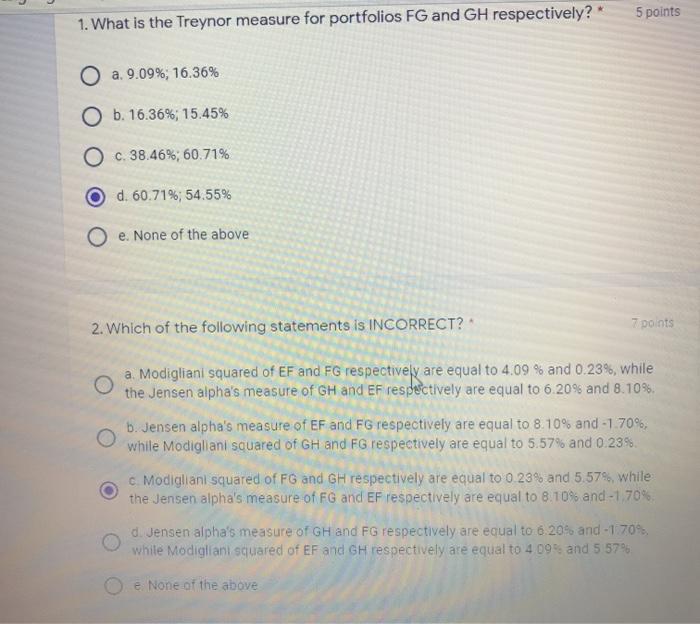

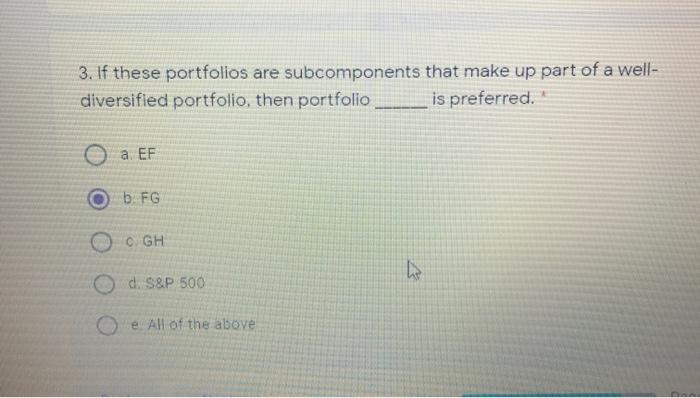

Question: Given the following data, answer questions 1 to 3 below: Average Standard Fund Beta return deviation EF 23% 33% 1.1 FG 15% 26% 1.3 GH

Given the following data, answer questions 1 to 3 below: Average Standard Fund Beta return deviation EF 23% 33% 1.1 FG 15% 26% 1.3 GH 22 28 1.2 S&P500 14% 24% 1 Risk-free 5% 5 points 1. What is the Treynor measure for portfolios FG and GH respectively? O a. 9.09% 16.36% O b. 16.36%; 15.45% O c. 38.46%; 60.71% d. 60.71%; 54.55% Oe. None of the above 2. Which of the following statements is INCORRECT? 7 points a Modigliani squared of EF and FG respectively are equal to 4.09 % and 0.23%, while the Jensen alpha's measure of GH and EF respectively are equal to 6.20% and 8. 10% b. Jensen alpha's measure of EF and FG respectively are equal to 8. 10% and -1.70%, while Modigliani souared of GH and FG respectively are equal to 5.57% and 0.23% c. Modigliani squared of FG and GH respectively are equal to 0 23% and 5.57%, while the Jensen alpha's measure of FG and EF respectively are equal to 8.10% and -1 70% d. Jensen alpha's measure of GH and FG respectively are equal to 6 20% and -1 70% while Modigliani squared of EF and GH respectively are equal to 409 and 5 57% e None of the above 3. If these portfolios are subcomponents that make up part of a well- diversified portfolio, then portfolio is preferred. O a. EF O b. FG C GH O d. S&P 500 e All of the above

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts