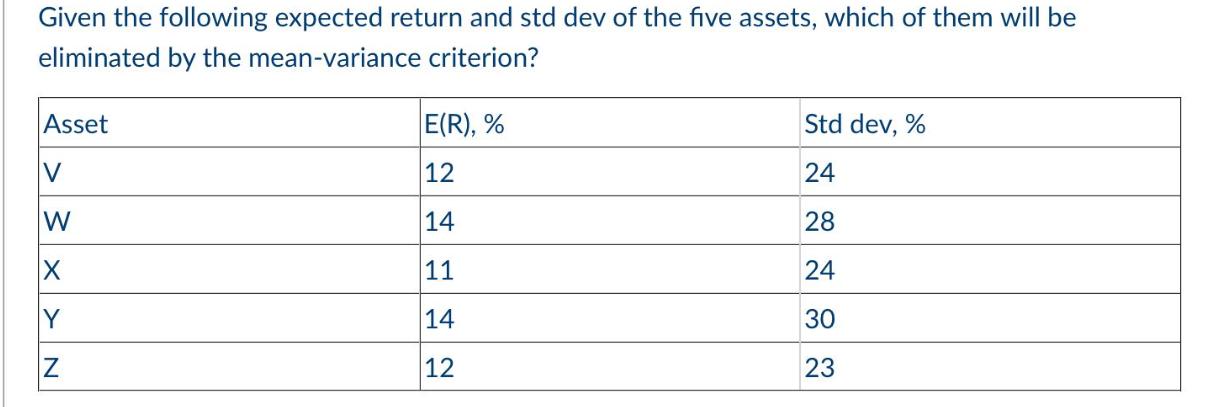

Question: Given the following expected return and std dev of the five assets, which of them will be eliminated by the mean-variance criterion? Asset E(R),

Given the following expected return and std dev of the five assets, which of them will be eliminated by the mean-variance criterion? Asset E(R), % Std dev, % V 12 24 W 14 28 11 24 Y 14 30 Z 12 23

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Based on the meanvariance criterion the asset that would likely be eliminated is W The meanvariance ... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock