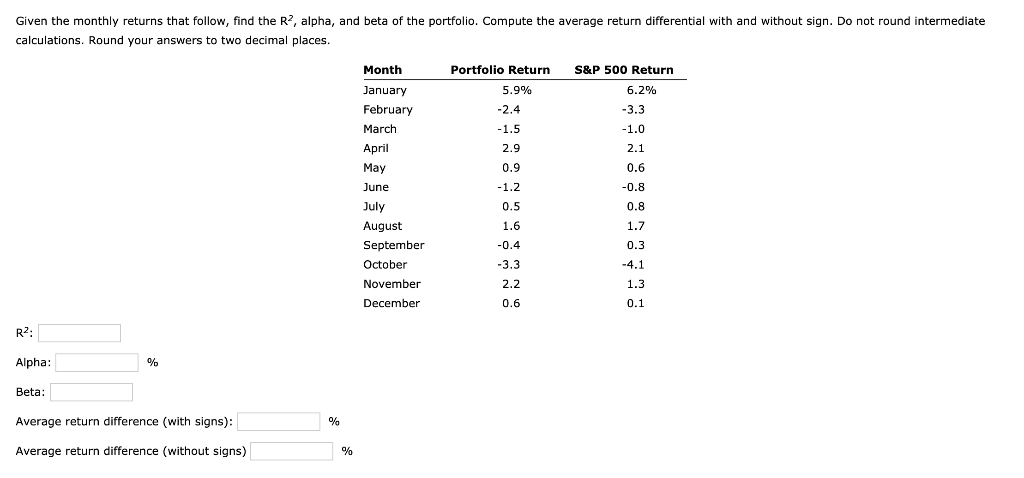

Question: Given the monthly returns that follow, find the R2, alpha, and beta of the portfolio. Compute the average return differential with and without sign. Do

Given the monthly returns that follow, find the R2, alpha, and beta of the portfolio. Compute the average return differential with and without sign. Do not round intermediate calculations. Round your answers to two decimal places. Month S&P 500 Return 6.2% Portfolio Return 5.9% -2.4 -1.5 2.9 -3.3 -1.0 2.1 0.9 0.6 -1.2 -0.8 January February March April May June July August September October November December 0.5 0.8 1.7 1.6 -0.4 0.3 -4.1 -3.3 2.2 1.3 0.1 0.6 R2: Alpha: % Beta: Average return difference (with signs): % Average return difference (without signs) % Given the monthly returns that follow, find the R2, alpha, and beta of the portfolio. Compute the average return differential with and without sign. Do not round intermediate calculations. Round your answers to two decimal places. Month S&P 500 Return 6.2% Portfolio Return 5.9% -2.4 -1.5 2.9 -3.3 -1.0 2.1 0.9 0.6 -1.2 -0.8 January February March April May June July August September October November December 0.5 0.8 1.7 1.6 -0.4 0.3 -4.1 -3.3 2.2 1.3 0.1 0.6 R2: Alpha: % Beta: Average return difference (with signs): % Average return difference (without signs) %

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts