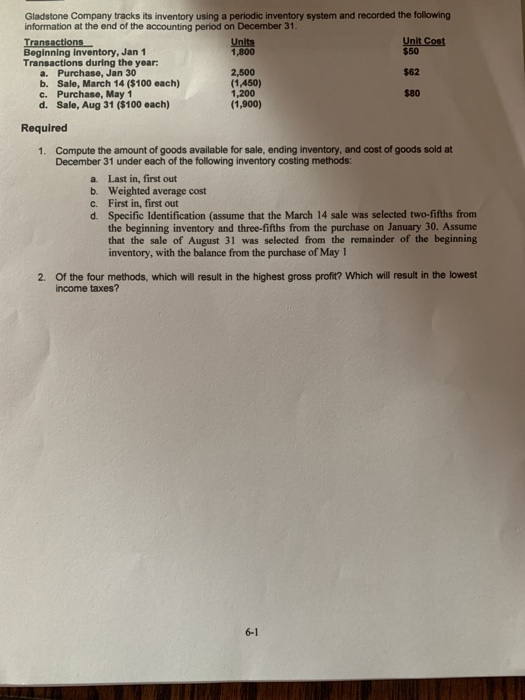

Question: Gladstone Company tracks its inventory using a periodic inventory system and recorded the following information at the end of the accounting period on December 31.

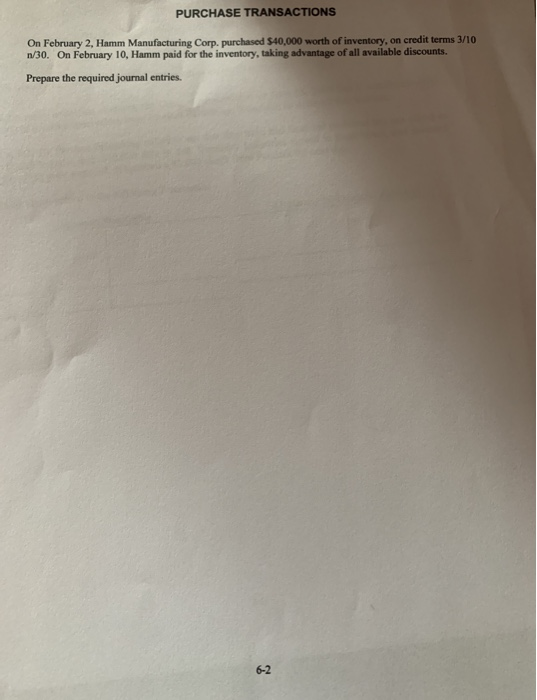

Gladstone Company tracks its inventory using a periodic inventory system and recorded the following information at the end of the accounting period on December 31. Transactions Units Unit Cost Beginning inventory, Jan 1 1,800 $50 Transactions during the year: a. Purchase, Jan 30 2,500 $62 b. Sale, March 14 ($100 each) (1.450) C. Purchase, May 1 1,200 $80 d. Sale, Aug 31 ($100 each) (1,900) Required 1. Compute the amount of goods available for sale, ending inventory, and cost of goods sold at December 31 under each of the following inventory costing methods: Last in, first out b. Weighted average cost c. First in, first out d. Specific Identification (assume that the March 14 sale was selected two-fifths from the beginning inventory and three-fifths from the purchase on January 30. Assume that the sale of August 31 was selected from the remainder of the beginning inventory, with the balance from the purchase of May 1 2. Of the four methods, which will result in the highest gross profit? Which will result in the lowest income taxes? a 6-1 PURCHASE TRANSACTIONS On February 2, Hamm Manufacturing Corp purchased $40,000 worth of inventory, on credit terms 3/10 n/30. On February 10, Hamm paid for the inventory, taking advantage of all available discounts. Prepare the required journal entries. 6-2

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts