Question: Grade-Based System In an effort to address this problem, Mr. Abbott suggested that the SBCAS for Jef- ferson be based on grade distinctions. He therefore

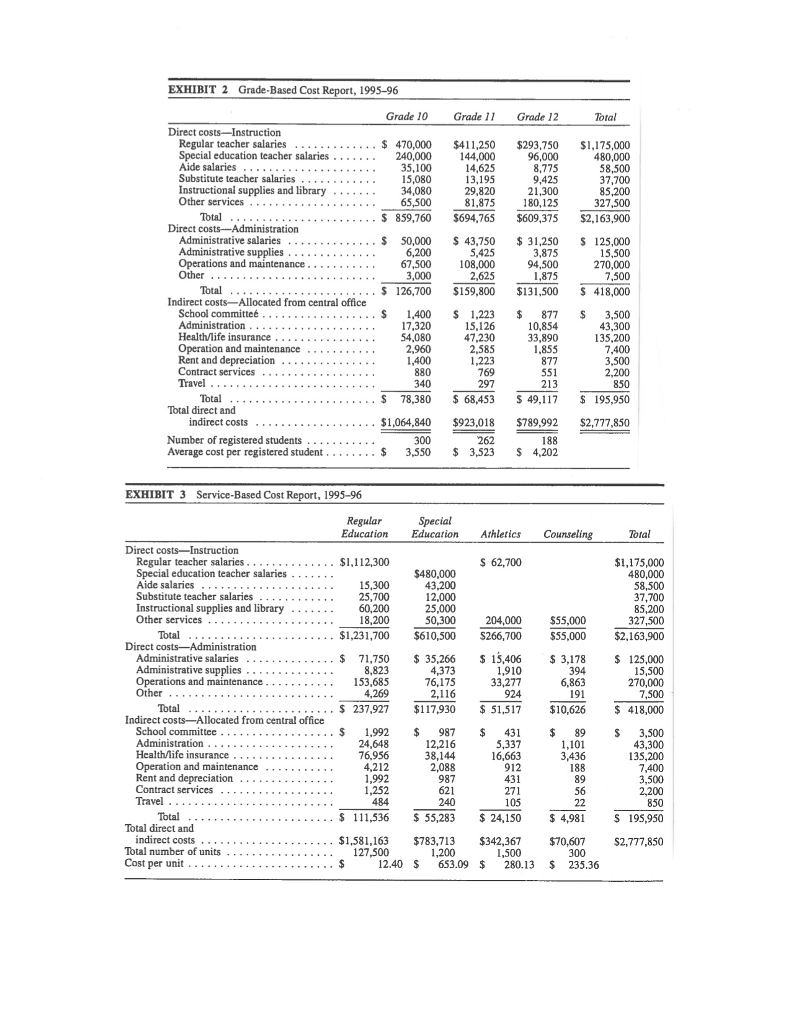

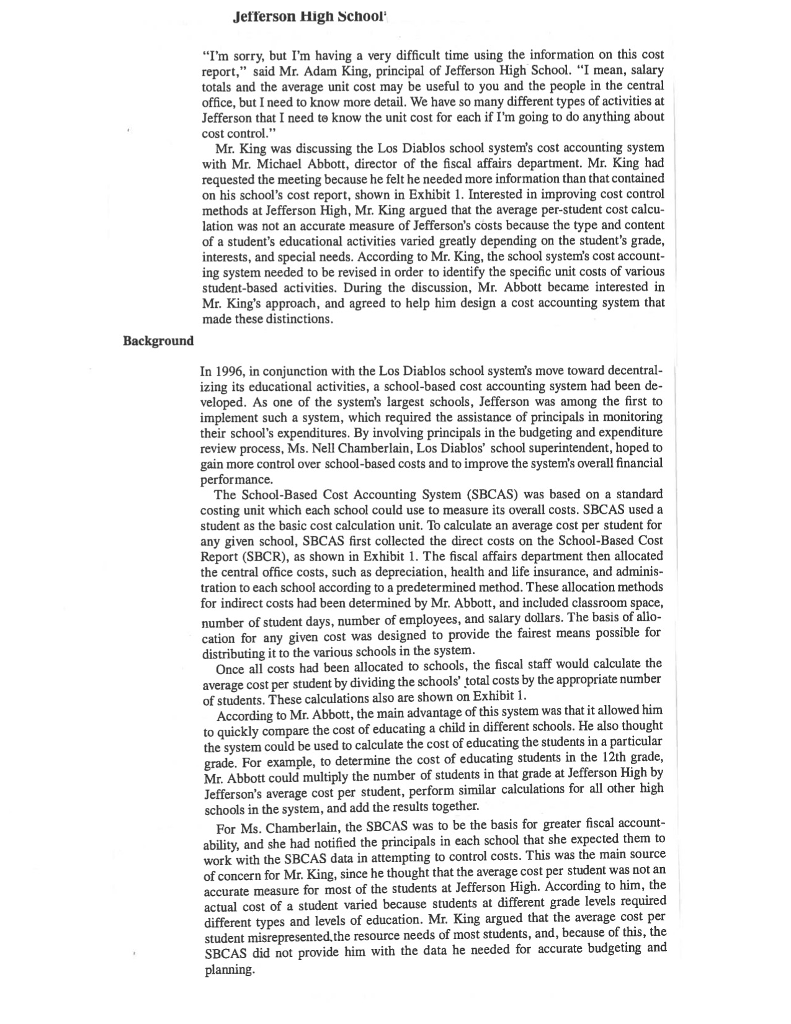

Grade-Based System In an effort to address this problem, Mr. Abbott suggested that the SBCAS for Jef- ferson be based on grade distinctions. He therefore divided the school's students into three categories based on their grade levels-10th, 11th, and 12th-and, with Mr. King's help, calculated personnel and supply estimates for each grade level. For example, he estimated that although there were fewer students in the 12th grade than the 10th or 11th, many students in the 12th grade regularly used the school's career counselor, whereas most students in the 10th and 11th grades did not. From these estimates, Mr. Abbott assigned Jefferson's direct costs to each grade level. Next, Mr. Abbott set about devising a method for allocating the indirect costs. After much discussion with Mr. King and his staff, he decided to allocate all these costs according to the number of students in each grade. His calculations are contained in Exhibit 2 Although the new system maintained a student as the standard costing unit, Mr. Abbott argued that it was a more accurate approach than the system currently in use. Instead of an average cost per student, he now had three average cost figures: one for each grade level. In evaluating the new cost accounting system, Mr. King and Mr. Abbott explored the differences in cost calculations resulting from the two systems. Some quick com- putations by the two pointed out the differences in the cost per student under different accounting procedures. From these findings, Mr. Abbott concluded that his "grade based" system could greatly increase a principal's ability to budget and control costs. As Mr. King reflected on the new system, a few problems continued to bother him Although he agreed that the grade-based costs were more accurate than the school based per-student calculations, he felt there were further distinctions in resource use that the system did not sufficiently address. He was particularly disturbed about the varying intensities of special education, athletics, and counseling received within each grade. Mr. King explained to Mr. Abbott that, according to the new accounting system, it appeared as though all students in the 12th grade received the same amount of educational resources, but from his perspective this clearly was not the case. He pointed out by way of example that a student in varsity athletics received far more athletic resources than one taking only regular physical education classes. Similarly, a student whose behavior resulted in a need to see the school counselor regularly used more counseling resources than one who was well-behaved. These sorts of distinc- tions could be made, he argued, for special education as well. As such, the grade based breakdown was not a sufficiently accurate measure. Service-Based System Unable to convince Mr. Abbott of the importance of this additional refinement Mr. King himself began experimenting with a third cost accounting method-based on levels of educational services received-that he thought might be more accurate As the first step in his calculations, he divided the school's costs according to the type of service provided: regular education, special education, athletics, and counseling He decided that a student's use of the regular education component could be measured most easily and accurately in terms of the number of days of school attendance during the academic year Examining Jefferson's student records, he decided that it was more complicated to measure special education. He consulted with some of the special education teachers and, with them, developed a system based on levels of special education needs. They decided to define special education intensity on three levels: one unit represented occasional assistance only; two units were for a student who received special educa- tion services for one or two days a week; three units represented three or more days a week. Athletics and counseling were measured in a similar fashion. Students who partic- pated in after-school athletic programs but did not play either junior varsity or varsity sports received one unit; two units were given for junior varsity; three units for varsity. Students who used counseling services on an infrequent basis received one unit; those who used them more regularly received two units; those who used them continually received three units. Grade-Based System In an effort to address this problem, Mr. Abbott suggested that the SBCAS for Jef- ferson be based on grade distinctions. He therefore divided the school's students into three categories based on their grade levels-10th, 11th, and 12th-and, with Mr. King's help, calculated personnel and supply estimates for each grade level. For example, he estimated that although there were fewer students in the 12th grade than the 10th or 11th, many students in the 12th grade regularly used the school's career counselor, whereas most students in the 10th and 11th grades did not. From these estimates, Mr. Abbott assigned Jefferson's direct costs to each grade level. Next, Mr. Abbott set about devising a method for allocating the indirect costs. After much discussion with Mr. King and his staff, he decided to allocate all these costs according to the number of students in each grade. His calculations are contained in Exhibit 2 Although the new system maintained a student as the standard costing unit, Mr. Abbott argued that it was a more accurate approach than the system currently in use. Instead of an average cost per student, he now had three average cost figures: one for each grade level. In evaluating the new cost accounting system, Mr. King and Mr. Abbott explored the differences in cost calculations resulting from the two systems. Some quick com- putations by the two pointed out the differences in the cost per student under different accounting procedures. From these findings, Mr. Abbott concluded that his "grade based" system could greatly increase a principal's ability to budget and control costs. As Mr. King reflected on the new system, a few problems continued to bother him Although he agreed that the grade-based costs were more accurate than the school based per-student calculations, he felt there were further distinctions in resource use that the system did not sufficiently address. He was particularly disturbed about the varying intensities of special education, athletics, and counseling received within each grade. Mr. King explained to Mr. Abbott that, according to the new accounting system, it appeared as though all students in the 12th grade received the same amount of educational resources, but from his perspective this clearly was not the case. He pointed out by way of example that a student in varsity athletics received far more athletic resources than one taking only regular physical education classes. Similarly, a student whose behavior resulted in a need to see the school counselor regularly used more counseling resources than one who was well-behaved. These sorts of distinc- tions could be made, he argued, for special education as well. As such, the grade based breakdown was not a sufficiently accurate measure. Service-Based System Unable to convince Mr. Abbott of the importance of this additional refinement Mr. King himself began experimenting with a third cost accounting method-based on levels of educational services received-that he thought might be more accurate As the first step in his calculations, he divided the school's costs according to the type of service provided: regular education, special education, athletics, and counseling He decided that a student's use of the regular education component could be measured most easily and accurately in terms of the number of days of school attendance during the academic year Examining Jefferson's student records, he decided that it was more complicated to measure special education. He consulted with some of the special education teachers and, with them, developed a system based on levels of special education needs. They decided to define special education intensity on three levels: one unit represented occasional assistance only; two units were for a student who received special educa- tion services for one or two days a week; three units represented three or more days a week. Athletics and counseling were measured in a similar fashion. Students who partic- pated in after-school athletic programs but did not play either junior varsity or varsity sports received one unit; two units were given for junior varsity; three units for varsity. Students who used counseling services on an infrequent basis received one unit; those who used them more regularly received two units; those who used them continually received three units

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts