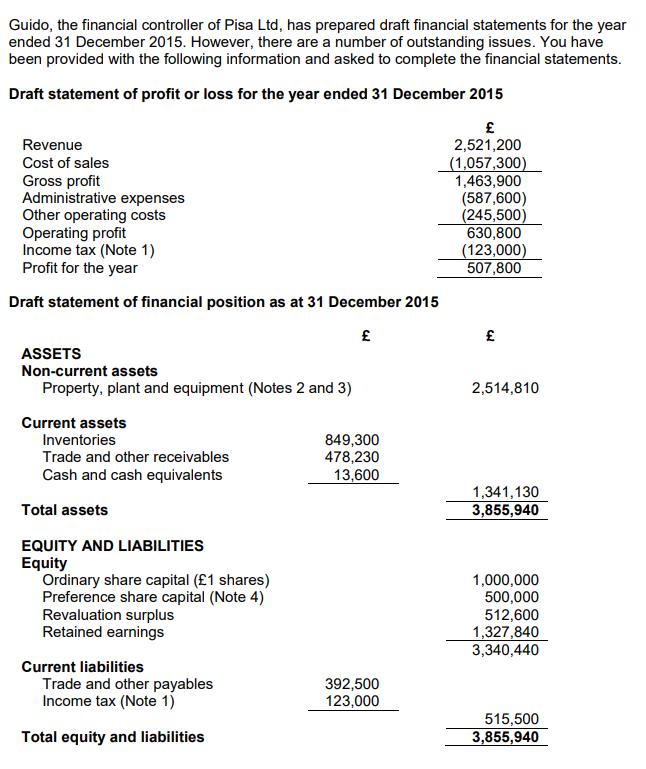

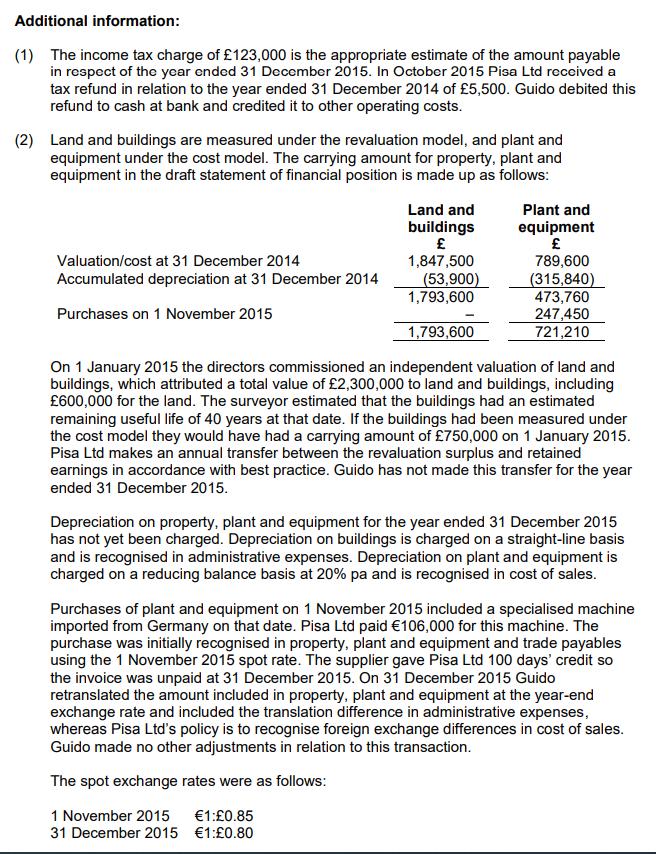

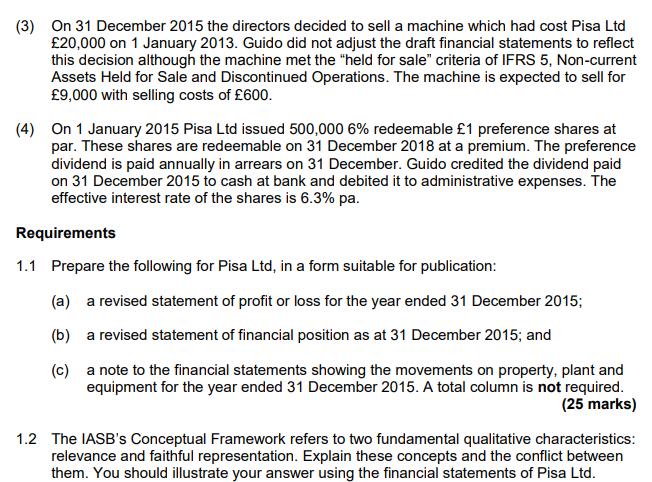

Guido, the financial controller of Pisa Ltd, has prepared draft financial statements for the year ended...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

Guido, the financial controller of Pisa Ltd, has prepared draft financial statements for the year ended 31 December 2015. However, there are a number of outstanding issues. You have been provided with the following information and asked to complete the financial statements. Draft statement of profit or loss for the year ended 31 December 2015 £ 2,521,200 (1,057,300) 1,463,900 Revenue Cost of sales Gross profit Administrative expenses Other operating costs Operating profit Income tax (Note 1) Profit for the year Draft statement of financial position as at 31 December 2015 ASSETS Non-current assets Property, plant and equipment (Notes 2 and 3) Current assets Inventories Trade and other receivables Cash and cash equivalents Total assets EQUITY AND LIABILITIES Equity Ordinary share capital (£1 shares) Preference share capital (Note 4) Revaluation surplus Retained earnings Current liabilities Trade and other payables Income tax (Note 1) Total equity and liabilities W 849,300 478,230 13,600 392,500 123,000 (587,600) (245,500) 630,800 (123,000) 507,800 £ 2,514,810 1,341,130 3,855,940 1,000,000 500,000 512,600 1,327,840 3,340,440 515,500 3,855,940 Additional information: (1) The income tax charge of £123,000 is the appropriate estimate of the amount payable in respect of the year ended 31 December 2015. In October 2015 Pisa Ltd received a tax refund in relation to the year ended 31 December 2014 of £5,500. Guido debited this refund to cash at bank and credited it to other operating costs. (2) Land and buildings are measured under the revaluation model, and plant and equipment under the cost model. The carrying amount for property, plant and equipment in the draft statement of financial position is made up as follows: Valuation/cost at 31 December 2014 Accumulated depreciation at 31 December 2014 Purchases on 1 November 2015 Land and buildings £ 1,847,500 (53,900) 1,793,600 1,793,600 On 1 January 2015 the directors commissioned an independent valuation of land and buildings, which attributed a total value of £2,300,000 to land and buildings, including £600,000 for the land. The surveyor estimated that the buildings had an estimated remaining useful life of 40 years at that date. If the buildings had been measured under the cost model they would have had a carrying amount of £750,000 on 1 January 2015. Pisa Ltd makes an annual transfer between the revaluation surplus and retained earnings in accordance with best practice. Guido has not made this transfer for the year ended 31 December 2015. Plant and equipment £ 789,600 (315,840) 473,760 247,450 721,210 Depreciation on property, plant and equipment for the year ended 31 December 2015 has not yet been charged. Depreciation on buildings is charged on a straight-line basis and is recognised in administrative expenses. Depreciation on plant and equipment is charged on a reducing balance basis at 20% pa and is recognised in cost of sales. 1 November 2015 31 December 2015 Purchases of plant and equipment on 1 November 2015 included a specialised machine imported from Germany on that date. Pisa Ltd paid €106,000 for this machine. The purchase was initially recognised in property, plant and equipment and trade payables using the 1 November 2015 spot rate. The supplier gave Pisa Ltd 100 days' credit so the invoice was unpaid at 31 December 2015. On 31 December 2015 Guido retranslated the amount included in property, plant and equipment at the year-end exchange rate and included the translation difference in administrative expenses, whereas Pisa Ltd's policy is to recognise foreign exchange differences in cost of sales. Guido made no other adjustments in relation to this transaction. The spot exchange rates were as follows: €1:£0.85 €1:£0.80 (3) On 31 December 2015 the directors decided to sell a machine which had cost Pisa Ltd £20,000 on 1 January 2013. Guido did not adjust the draft financial statements to reflect this decision although the machine met the "held for sale" criteria of IFRS 5, Non-current Assets Held for Sale and Discontinued Operations. The machine is expected to sell for £9,000 with selling costs of £600. (4) On 1 January 2015 Pisa Ltd issued 500,000 6% redeemable £1 preference shares at par. These shares are redeemable on 31 December 2018 at a premium. The preference dividend is paid annually in arrears on 31 December. Guido credited the dividend paid on 31 December 2015 to cash at bank and debited it to administrative expenses. The effective interest rate of the shares is 6.3% pa. Requirements 1.1 Prepare the following for Pisa Ltd, in a form suitable for publication: (a) a revised statement of profit or loss for the year ended 31 December 2015; (b) a revised statement of financial position as at 31 December 2015; and (c) a note to the financial statements showing the movements on property, plant and equipment for the year ended 31 December 2015. A total column is not required. (25 marks) 1.2 The IASB's Conceptual Framework refers to two fundamental qualitative characteristics: relevance and faithful representation. Explain these concepts and the conflict between them. You should illustrate your answer using the financial statements of Pisa Ltd. Guido, the financial controller of Pisa Ltd, has prepared draft financial statements for the year ended 31 December 2015. However, there are a number of outstanding issues. You have been provided with the following information and asked to complete the financial statements. Draft statement of profit or loss for the year ended 31 December 2015 £ 2,521,200 (1,057,300) 1,463,900 Revenue Cost of sales Gross profit Administrative expenses Other operating costs Operating profit Income tax (Note 1) Profit for the year Draft statement of financial position as at 31 December 2015 ASSETS Non-current assets Property, plant and equipment (Notes 2 and 3) Current assets Inventories Trade and other receivables Cash and cash equivalents Total assets EQUITY AND LIABILITIES Equity Ordinary share capital (£1 shares) Preference share capital (Note 4) Revaluation surplus Retained earnings Current liabilities Trade and other payables Income tax (Note 1) Total equity and liabilities W 849,300 478,230 13,600 392,500 123,000 (587,600) (245,500) 630,800 (123,000) 507,800 £ 2,514,810 1,341,130 3,855,940 1,000,000 500,000 512,600 1,327,840 3,340,440 515,500 3,855,940 Additional information: (1) The income tax charge of £123,000 is the appropriate estimate of the amount payable in respect of the year ended 31 December 2015. In October 2015 Pisa Ltd received a tax refund in relation to the year ended 31 December 2014 of £5,500. Guido debited this refund to cash at bank and credited it to other operating costs. (2) Land and buildings are measured under the revaluation model, and plant and equipment under the cost model. The carrying amount for property, plant and equipment in the draft statement of financial position is made up as follows: Valuation/cost at 31 December 2014 Accumulated depreciation at 31 December 2014 Purchases on 1 November 2015 Land and buildings £ 1,847,500 (53,900) 1,793,600 1,793,600 On 1 January 2015 the directors commissioned an independent valuation of land and buildings, which attributed a total value of £2,300,000 to land and buildings, including £600,000 for the land. The surveyor estimated that the buildings had an estimated remaining useful life of 40 years at that date. If the buildings had been measured under the cost model they would have had a carrying amount of £750,000 on 1 January 2015. Pisa Ltd makes an annual transfer between the revaluation surplus and retained earnings in accordance with best practice. Guido has not made this transfer for the year ended 31 December 2015. Plant and equipment £ 789,600 (315,840) 473,760 247,450 721,210 Depreciation on property, plant and equipment for the year ended 31 December 2015 has not yet been charged. Depreciation on buildings is charged on a straight-line basis and is recognised in administrative expenses. Depreciation on plant and equipment is charged on a reducing balance basis at 20% pa and is recognised in cost of sales. 1 November 2015 31 December 2015 Purchases of plant and equipment on 1 November 2015 included a specialised machine imported from Germany on that date. Pisa Ltd paid €106,000 for this machine. The purchase was initially recognised in property, plant and equipment and trade payables using the 1 November 2015 spot rate. The supplier gave Pisa Ltd 100 days' credit so the invoice was unpaid at 31 December 2015. On 31 December 2015 Guido retranslated the amount included in property, plant and equipment at the year-end exchange rate and included the translation difference in administrative expenses, whereas Pisa Ltd's policy is to recognise foreign exchange differences in cost of sales. Guido made no other adjustments in relation to this transaction. The spot exchange rates were as follows: €1:£0.85 €1:£0.80 (3) On 31 December 2015 the directors decided to sell a machine which had cost Pisa Ltd £20,000 on 1 January 2013. Guido did not adjust the draft financial statements to reflect this decision although the machine met the "held for sale" criteria of IFRS 5, Non-current Assets Held for Sale and Discontinued Operations. The machine is expected to sell for £9,000 with selling costs of £600. (4) On 1 January 2015 Pisa Ltd issued 500,000 6% redeemable £1 preference shares at par. These shares are redeemable on 31 December 2018 at a premium. The preference dividend is paid annually in arrears on 31 December. Guido credited the dividend paid on 31 December 2015 to cash at bank and debited it to administrative expenses. The effective interest rate of the shares is 6.3% pa. Requirements 1.1 Prepare the following for Pisa Ltd, in a form suitable for publication: (a) a revised statement of profit or loss for the year ended 31 December 2015; (b) a revised statement of financial position as at 31 December 2015; and (c) a note to the financial statements showing the movements on property, plant and equipment for the year ended 31 December 2015. A total column is not required. (25 marks) 1.2 The IASB's Conceptual Framework refers to two fundamental qualitative characteristics: relevance and faithful representation. Explain these concepts and the conflict between them. You should illustrate your answer using the financial statements of Pisa Ltd.

Expert Answer:

Answer rating: 100% (QA)

11a Statement of profit or loss for the year ended 31 December 2015 2521200 Revenue Cost of sales Gr... View the full answer

Posted Date:

Students also viewed these accounting questions

-

You have been provided with the following information about two companies: Required: a. Calculate the current ratio for each company and the amount of working capital each company has. b. Which...

-

You have been provided with the following information about Everell Inc. (Everell). Required: a. Calculate the accounts receivable, inventory, and accounts payable turnover ratios for 2016 through...

-

You have been provided with the following information regarding R-Steel Inc.'s inventory for March, April, and May. Instructions (a) Calculate the cost and net realizable value of R-Steel's inventory...

-

The table represents values of differentiable functions f and g and their first derivatives. Use the table of values to answer the questions that follow. Work all of the parts below the line. X f g...

-

Using the information in Table 15.5, assume that the volatility of oil is 15%. a. Show that a bond that pays one barrel of oil in 1 year sells today for $19.2454. b. Consider a bond that in 1 year...

-

Confidentiality in the workplace Suppose you work in a police station or law firm and signed a confidentiality agreement regarding all their cases at hand,suddenly your friend who was a suspect to a...

-

What is the role of domain analysis in designing a product?

-

Pumping a hydrochloric acid solution (Fig. 7A.2), a dilute HC1 solution of constant density and viscosity ( p = 62.4lb m /ft 3 , = 1 cp) is to be pumped from tank I to tank 2 with no overall change...

-

Many of you have worked for or experienced various types of leaders. Identify one major quality you believe makes a good leader and explain how this quality interrelates to one values? Please explain...

-

We left Lou for a few weeks and despite his best intentions, he has not been staying on top of his bookkeeping. With the new apartment complex account, business is booming. Probably. Maybe? It's hard...

-

Read the case study Velma Sue Bates v. Dura Automotive Systems, Inc. and answer the question: Is there an ethical resolution to this case?

-

You are given the following information about a stock: Calculate the value of the call option if the stock goes up in 3 out of the 5 months. S = $100 X = $101 r = .005 n = 5 u= 1.10 d = .95 Price of...

-

A local bakery found that it was throwing out too many cookies every night, so the manager conducted a study on the sales of cookies and found that on an ordinary day, the sales of cookies follow a...

-

The IQ scores of human beings are scaled to follow a normal distribution with mean 100 and standard deviation 16. If those with IQ scores higher than 154 are regarded as geniuses, how many geniuses...

-

In question 17, the average amount of soda dispensed into the cans is adjustable. If we want to make sure that 99.9 % of the soda cans contain more than 12 oz, to what should we adjust the average?...

-

Suppose that X represents the number of cars arriving at a toll booth in 1 min. Further, suppose that X can assume the values 1, 2, 3, 4, and 5 and has the following distribution: Calculate the...

-

The Hard Rock Mining Company is trying to develop cost formula for utility cost.Two independent variables are being considered: Tons Mined and Direct Labor hours. As the managerial accountant, you...

-

Subprime loans have higher loss rates than many other types of loans. Explain why lenders offer subprime loans. Describe the characteristics of the typical borrower in a subprime consumer loan.

-

Light of a single wavelength is incident on a diffraction grating with \(500 \mathrm{slits} / \mathrm{mm}\). Several bright fringes are observed on a screen behind the grating, including one at...

-

A miniature spectrometer used for chemical analysis has a diffraction grating with 800 slits \(/ \mathrm{mm}\) set \(25.0 \mathrm{~mm}\) in front of the detector "screen." The detector can barely...

-

A laboratory dish, \(20 \mathrm{~cm}\) in diameter, is half filled with V. water. One at a time, \(0.50 \mu \mathrm{L}\) drops of oil from a micropipette are dropped onto the surface of the water,...

Study smarter with the SolutionInn App