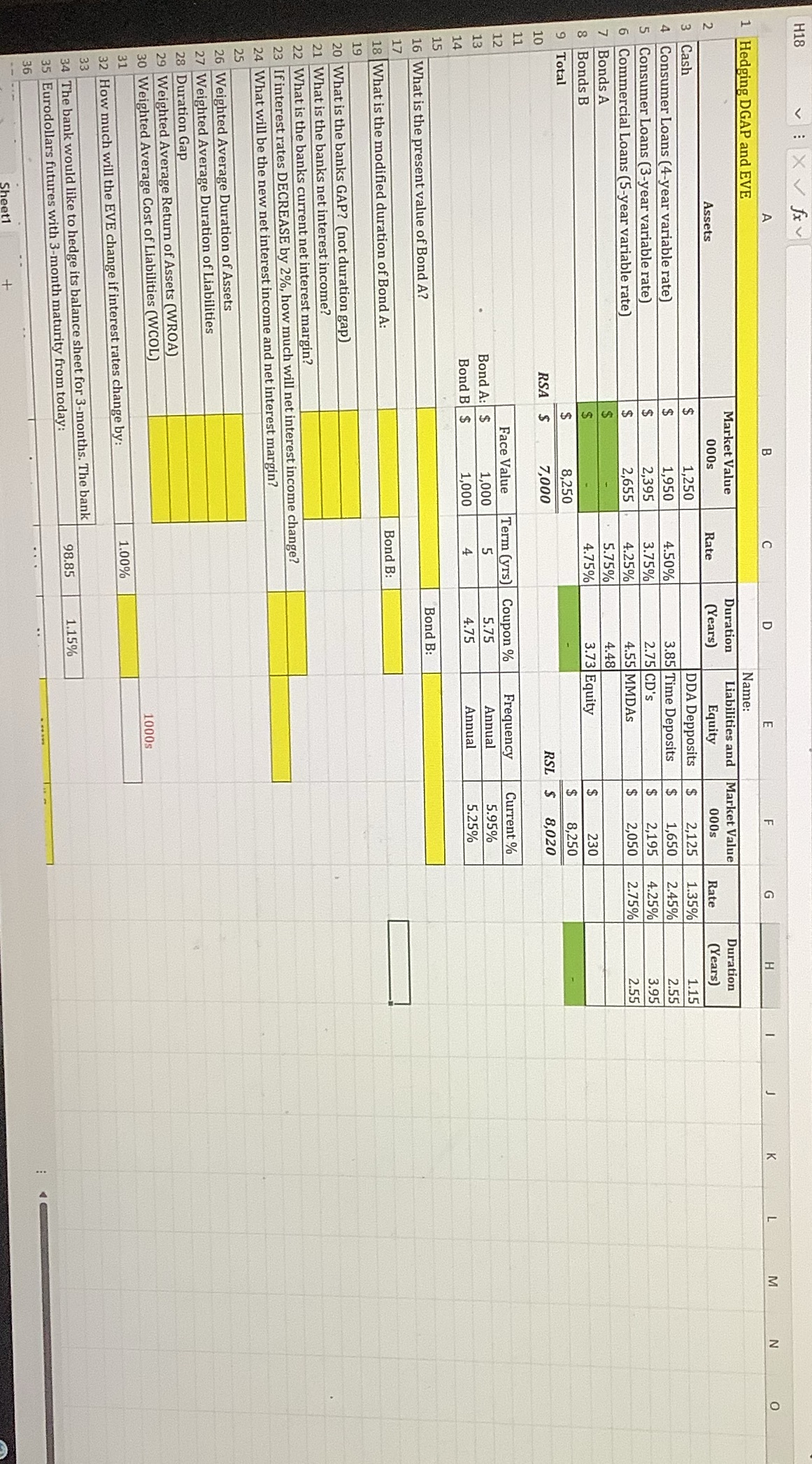

Question: H18 Z O LU G E I 1 Hedging DGAP and EVE Name: Market Value Duration Liabilities and Market Value Duration Assets 000s Rate (Years)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock