Helderberg Ltd (HelderBerg') is a public company in Pretoria that trades since 1 January 2017 in...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

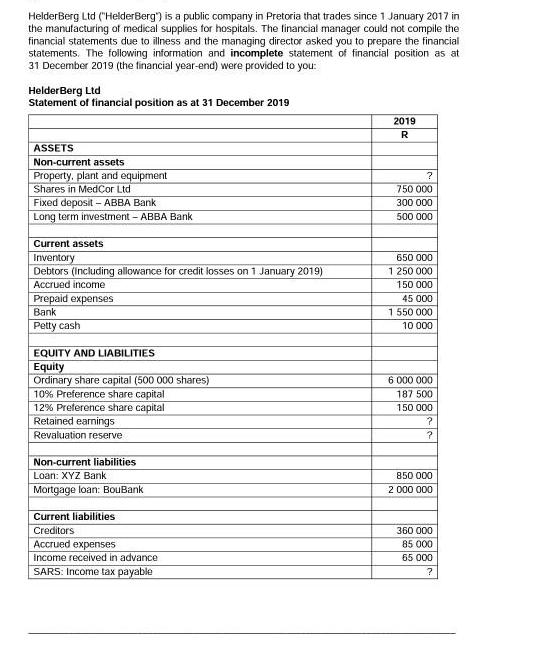

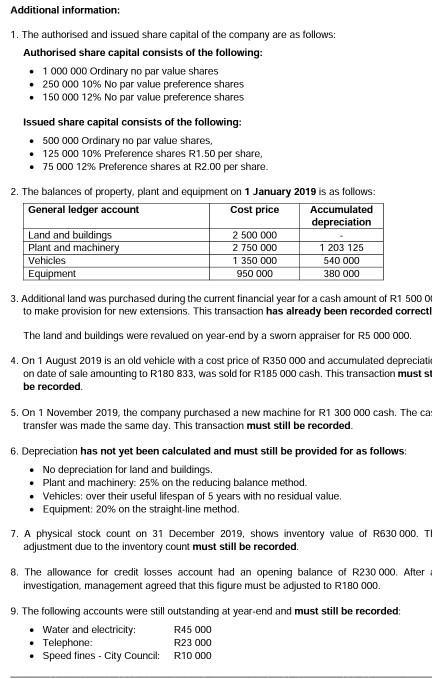

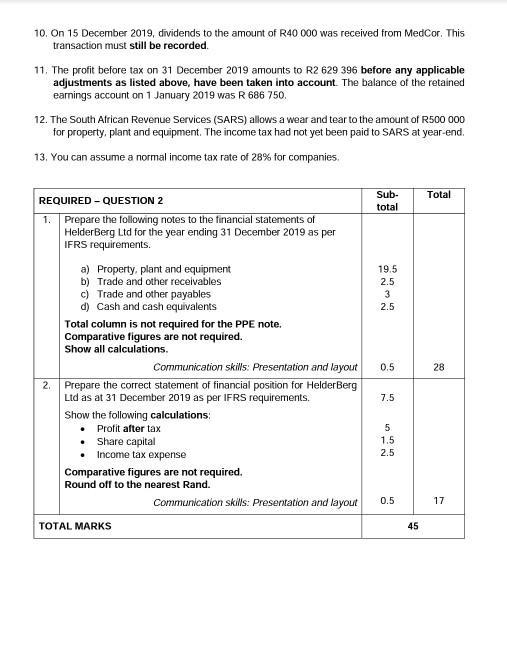

Helderberg Ltd ("HelderBerg') is a public company in Pretoria that trades since 1 January 2017 in the manufacturing of medical supplies for hospitals. The financial manager could not compile the financial statements due to illness and the managing director asked you to prepare the financial statements. The following information and incomplete statement of financial position as at 31 December 2019 (the financial year-end) were provided to you: Helder Berg Ltd Statement of financial position as at 31 December 2019 ASSETS Non-current assets Property, plant and equipment Shares in MedCor Ltd Fixed deposit - ABBA Bank Long term investment - ABBA Bank Current assets Inventory Debtors (including allowance for credit losses on 1 January 2019) Accrued income Prepaid expenses Bank Petty cash EQUITY AND LIABILITIES Equity Ordinary share capital (500 000 shares) 10% Preference share capital 12% Preference share capital Retained earnings Revaluation reserve Non-current liabilities Loan: XYZ Bank Mortgage loan: BouBank Current liabilities Creditors Accrued expenses Income received in advance SARS: Income tax payable 2019 R ? 750 000 300 000 500 000 650 000 1 250 000 150 000 45 000 1 550 000 10 000 6 000 000 187 500 150 000 ? ? 850 000 2 000 000 360 000 85 000 65 000 ? Additional information: 1. The authorised and issued share capital of the company are as follows: Authorised share capital consists of the following: • 1 000 000 Ordinary no par value shares • 250 000 10% No par value preference shares • 150 000 12 % No par value preference shares Issued share capital consists of the following: • 500 000 Ordinary no par value shares, 125 000 10% Preference shares R1.50 per share, • 75 000 12 % Preference shares at R2.00 per share. 2. The balances of property, plant and equipment on 1 January 2019 is as follows: General ledger account Cost price Land and buildings Plant and machinery Vehicles Equipment 2 500 000 2 750 000 1 350 000 950 000 3. Additional land was purchased during the current financial year for a cash amount of R1 500 0 to make provision for new extensions. This transaction has already been recorded correctl The land and buildings were revalued on year-end by a sworn appraiser for R5 000 000. 4. On 1 August 2019 is an old vehicle with a cost price of R350 000 and accumulated depreciatio on date of sale amounting to R180 833, was sold for R185 000 cash. This transaction must st be recorded. Accumulated depreciation 5. On 1 November 2019, the company purchased a new machine for R1 300 000 cash. The cas transfer was made the same day. This transaction must still be recorded. 1 203 125 540 000 380 000 6. Depreciation has not yet been calculated and must still be provided for as follows: No depreciation for land and buildings. • Plant and machinery: 25% on the reducing balance method. • Vehicles: over their useful lifespan of 5 years with no residual value. Equipment: 20% on the straight-line method. • Telephone: 7. A physical stock count on 31 December 2019, shows inventory value of R630 000. T adjustment due to the inventory count must still be recorded. Speed fines - City Council: 8. The allowance for credit losses account had an opening balance of R230 000. After investigation, management agreed that this figure must be adjusted to R180 000. R45 000 R23 000 R10 000 9. The following accounts were still outstanding at year-end and must still be recorded: Water and electricity: 10. On 15 December 2019, dividends to the amount of R40 000 was received from MedCor. This transaction must still be recorded. 11. The profit before tax on 31 December 2019 amounts to R2 629 396 before any applicable adjustments as listed above, have been taken into account. The balance of the retained earnings account on 1 January 2019 was R 686 750. 12. The South African Revenue Services (SARS) allows a wear and tear to the amount of R500 000 for property, plant and equipment. The income tax had not yet been paid to SARS at year-end. 13. You can assume a normal income tax rate of 28% for companies. REQUIRED - QUESTION 2 1. Prepare the following notes to the financial statements of Helderberg Ltd for the year ending 31 December 2019 as per IFRS requirements. a) Property, plant and equipment b) Trade and other receivables c) Trade and other payables d) Cash and cash equivalents Total column is not required for the PPE note. Comparative figures are not required. Show all calculations. Communication skills: Presentation and layout 2. Prepare the correct statement of financial position for Helderberg Ltd as at 31 December 2019 as per IFRS requirements. Show the following calculations: . Profit after tax • Share capital • Income tax expense Comparative figures are not required. Round off to the nearest Rand. TOTAL MARKS Communication skills: Presentation and layout Sub- total 19.5 2.5 3 2.5 0.5 7.5 5 1.5 2.5 0.5 45 Total 28 17 Helderberg Ltd ("HelderBerg') is a public company in Pretoria that trades since 1 January 2017 in the manufacturing of medical supplies for hospitals. The financial manager could not compile the financial statements due to illness and the managing director asked you to prepare the financial statements. The following information and incomplete statement of financial position as at 31 December 2019 (the financial year-end) were provided to you: Helder Berg Ltd Statement of financial position as at 31 December 2019 ASSETS Non-current assets Property, plant and equipment Shares in MedCor Ltd Fixed deposit - ABBA Bank Long term investment - ABBA Bank Current assets Inventory Debtors (including allowance for credit losses on 1 January 2019) Accrued income Prepaid expenses Bank Petty cash EQUITY AND LIABILITIES Equity Ordinary share capital (500 000 shares) 10% Preference share capital 12% Preference share capital Retained earnings Revaluation reserve Non-current liabilities Loan: XYZ Bank Mortgage loan: BouBank Current liabilities Creditors Accrued expenses Income received in advance SARS: Income tax payable 2019 R ? 750 000 300 000 500 000 650 000 1 250 000 150 000 45 000 1 550 000 10 000 6 000 000 187 500 150 000 ? ? 850 000 2 000 000 360 000 85 000 65 000 ? Additional information: 1. The authorised and issued share capital of the company are as follows: Authorised share capital consists of the following: • 1 000 000 Ordinary no par value shares • 250 000 10% No par value preference shares • 150 000 12 % No par value preference shares Issued share capital consists of the following: • 500 000 Ordinary no par value shares, 125 000 10% Preference shares R1.50 per share, • 75 000 12 % Preference shares at R2.00 per share. 2. The balances of property, plant and equipment on 1 January 2019 is as follows: General ledger account Cost price Land and buildings Plant and machinery Vehicles Equipment 2 500 000 2 750 000 1 350 000 950 000 3. Additional land was purchased during the current financial year for a cash amount of R1 500 0 to make provision for new extensions. This transaction has already been recorded correctl The land and buildings were revalued on year-end by a sworn appraiser for R5 000 000. 4. On 1 August 2019 is an old vehicle with a cost price of R350 000 and accumulated depreciatio on date of sale amounting to R180 833, was sold for R185 000 cash. This transaction must st be recorded. Accumulated depreciation 5. On 1 November 2019, the company purchased a new machine for R1 300 000 cash. The cas transfer was made the same day. This transaction must still be recorded. 1 203 125 540 000 380 000 6. Depreciation has not yet been calculated and must still be provided for as follows: No depreciation for land and buildings. • Plant and machinery: 25% on the reducing balance method. • Vehicles: over their useful lifespan of 5 years with no residual value. Equipment: 20% on the straight-line method. • Telephone: 7. A physical stock count on 31 December 2019, shows inventory value of R630 000. T adjustment due to the inventory count must still be recorded. Speed fines - City Council: 8. The allowance for credit losses account had an opening balance of R230 000. After investigation, management agreed that this figure must be adjusted to R180 000. R45 000 R23 000 R10 000 9. The following accounts were still outstanding at year-end and must still be recorded: Water and electricity: 10. On 15 December 2019, dividends to the amount of R40 000 was received from MedCor. This transaction must still be recorded. 11. The profit before tax on 31 December 2019 amounts to R2 629 396 before any applicable adjustments as listed above, have been taken into account. The balance of the retained earnings account on 1 January 2019 was R 686 750. 12. The South African Revenue Services (SARS) allows a wear and tear to the amount of R500 000 for property, plant and equipment. The income tax had not yet been paid to SARS at year-end. 13. You can assume a normal income tax rate of 28% for companies. REQUIRED - QUESTION 2 1. Prepare the following notes to the financial statements of Helderberg Ltd for the year ending 31 December 2019 as per IFRS requirements. a) Property, plant and equipment b) Trade and other receivables c) Trade and other payables d) Cash and cash equivalents Total column is not required for the PPE note. Comparative figures are not required. Show all calculations. Communication skills: Presentation and layout 2. Prepare the correct statement of financial position for Helderberg Ltd as at 31 December 2019 as per IFRS requirements. Show the following calculations: . Profit after tax • Share capital • Income tax expense Comparative figures are not required. Round off to the nearest Rand. TOTAL MARKS Communication skills: Presentation and layout Sub- total 19.5 2.5 3 2.5 0.5 7.5 5 1.5 2.5 0.5 45 Total 28 17

Expert Answer:

Related Book For

Accounting Principles

ISBN: 978-1119048473

7th Canadian Edition Volume 2

Authors: Jerry J. Weygandt, Donald E. Kieso, Paul D. Kimmel, Barbara Trenholm, Valerie Warren, Lori Novak

Posted Date:

Students also viewed these accounting questions

-

The statement of financial position as at 31 December 20X2 of Zoom Products Ltd included: Trade receivables...............................85,360 The financial statements for the year ended 31...

-

The Statement of Financial Position as at 31 December 2019 for Dinar Bhd is presented below. Equipment Less: Accumulated depreciation Accounts Receivable Less: Allowance for doubtful debts Prepaid...

-

To which individuals and/or organizations is a public company audit report ordinarily addressed?

-

A rectangular parking lot with a perimeter of 440 feet is to have an area of at least 8000 square feet. Within what bounds must the length of the rectangle lie?

-

Today's dividend is $10. Next year dividend will Expected rate of return in the market is 15% and the firm's growth rate is 3%. The firm pays out half of its growth in dividends.

-

Mr. Sam Moyer owns the following assets in a business that he wants to incorporate: 1 Cost values for tax purposes used to describe the lowest limit of the elected transfer price range in Exhibit...

-

Figure \(\mathrm{P} 27. 39\) shows five objects, all placed in the same uniform, upward-directed external magnetic field. Rank the objects according to the amount of magnetic flux through them,...

-

Pharmaceutical firms, oil and gas companies, and other ventures inevitably incur costs on unsuccessful investments in new projects (e.g., new drugs or new wells). For oil and gas firms, a debate...

-

(a) NP and Co. has imported goods for US $ 7,00,000. The amount is payable after three months. The company has also exported goods for US $ 4,50,000 and this amount is receivable in two months. For...

-

Consider the following linear programming problem Max 8X + 7Y s.t. 15X + 5Y < 75 10X + 6Y < 60 X + Y < 8 X, Y 0 a. Use a graph to show each constraint and the feasible region. b. Identify the...

-

What are T-tubules? Select one: a. infoldings of the sarcolemma b. infoldings of the sarcoplasmic reticulum c. dense areas of mitochondria d. contractile proteins e. leaky membranes

-

What is the equation for calculating a firms unlevered beta?

-

Why would the WACC based on market values tend to be higher than the one based on book values if the stock price exceeded its book value?

-

How is the financial plan related to the other parts of a firms overall strategic plan?

-

What would be the cost of equity for Firm X at Equity/Capital ratios of 1.0 (no debt) and 0.58 assuming that r RF = 5% and RPM = 4%? Use the Hamada equation to calculate the unlevered beta for Firm X...

-

How does sales stability affect the target capital structure?

-

A company starts the year with 4 bathtubs at a cost of $100 each. They sell three and then buy three more at $120 each. Finally, they sell two of these and then buy two more at $121 each. What is the...

-

Listed below are common types of current liabilities, contingencies, and commitments: a. Accounts payable b. Bank loans and commercial paper c. Notes payable d. Dividends payable e. Sales and excise...

-

On January 1, 2017, McAdam Ltd., a private company reporting under ASPE, purchased 25% of the common shares of Tomecek Corporation for $175,000. Tomecek reported profit of $85,000 for 2017 and paid...

-

Rod and Dall are partners in R&D LLP. The partnership reports profit of $75,000. There is no partner- ship agreement. (a) Prepare the entry to distribute the profit between the partners. (b) Prepare...

-

Strand Corp. purchased $300,000 of five-year, 4% Hydrocor bonds at 99 on June 30, 2017. Strand Corp. purchased the bonds to earn interest. Interest is paid semi-annually each June 30 and December 31....

-

Test for heteroskedasticity using a Goldfeld-Quandt test applied to (a) two subsamples with potentially different variances and (b) a model where the variance is hypothesized to depend on an...

-

Describe how to transform a model to eliminate heteroskedasticity.

-

Compute generalized least squares estimates of the linear probability model.

Study smarter with the SolutionInn App