Question: Hello, could I please get some help with this question. Thank you. Problem 6-6 Unbiased Expectations Theory (LG6-7) Suppose that the current 1-year rate (1-year

Hello,

could I please get some help with this question. Thank you.

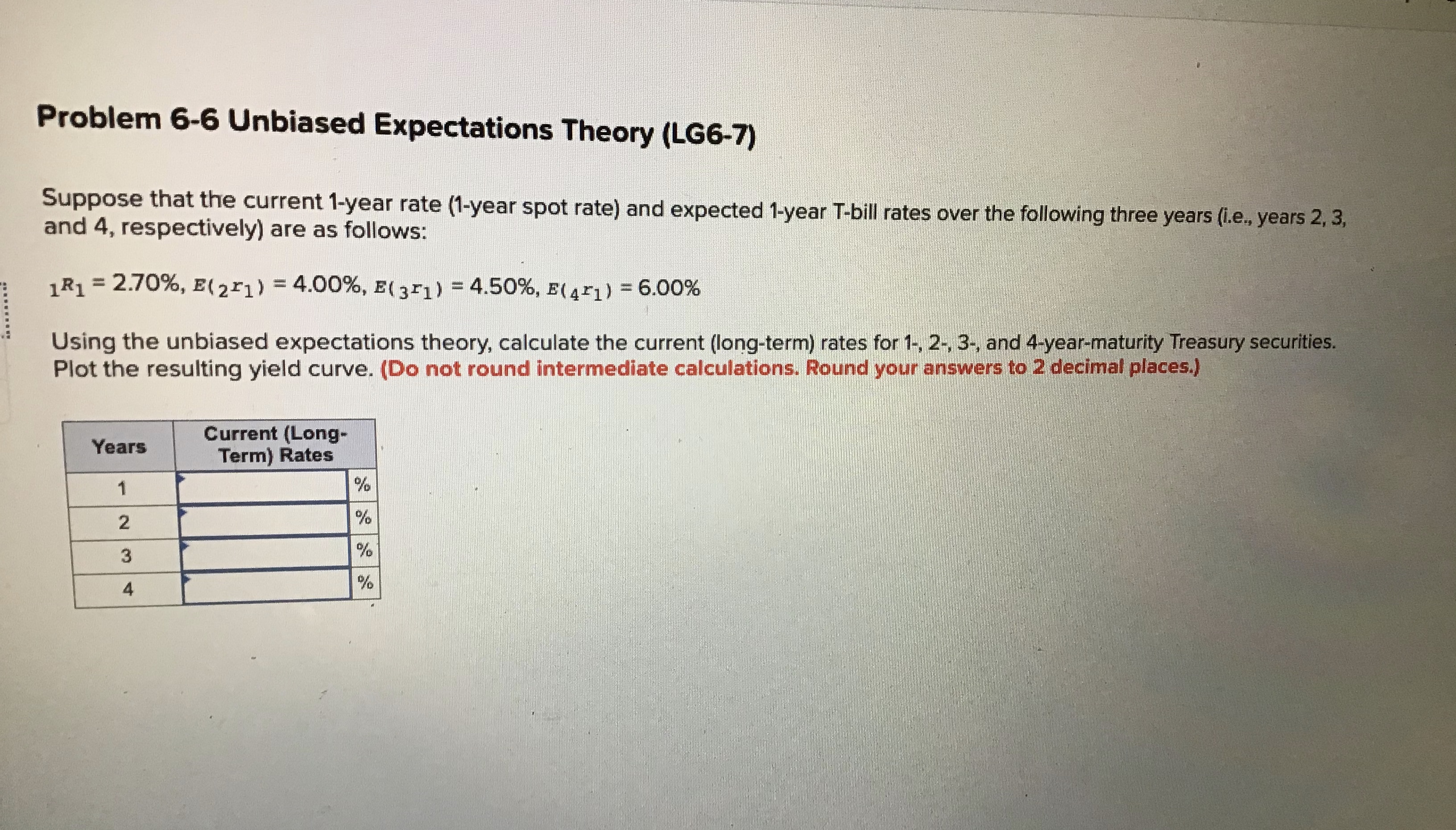

Problem 6-6 Unbiased Expectations Theory (LG6-7) Suppose that the current 1-year rate (1-year spot rate) and expected 1-year T-bill rates over the following three years (i.e., years 2, 3, and 4, respectively) are as follows: 1R1 = 2.70%, E(21 ) = 4.00%, E( 351 ) = 4.50%, E(451) = 6.00% Using the unbiased expectations theory, calculate the current (long-term) rates for 1-, 2-, 3-, and 4-year-maturity Treasury securities. Plot the resulting yield curve. (Do not round intermediate calculations. Round your answers to 2 decimal places.) Years Current (Long- Term) Rates 1 % 2 3 4

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts