Question: Hello, could you help me with this question (WACC =7%). I should find around 40 billion, but i find way more and don't undertsand why

Hello, could you help me with this question (WACC =7%). I should find around 40 billion, but i find way more and don't undertsand why

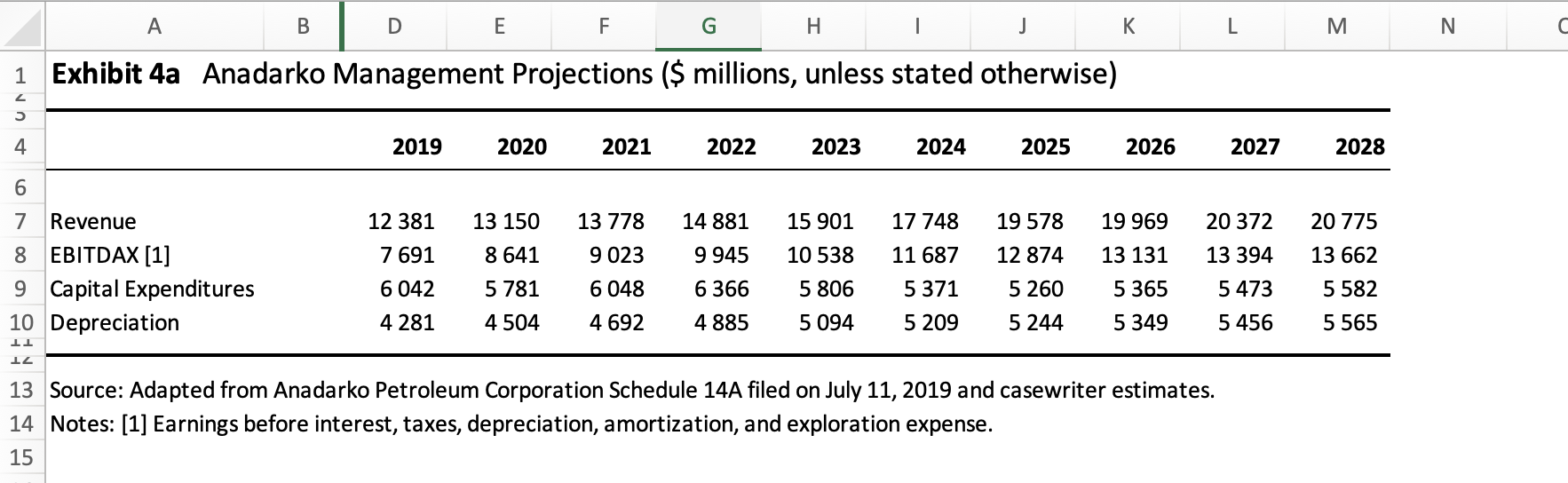

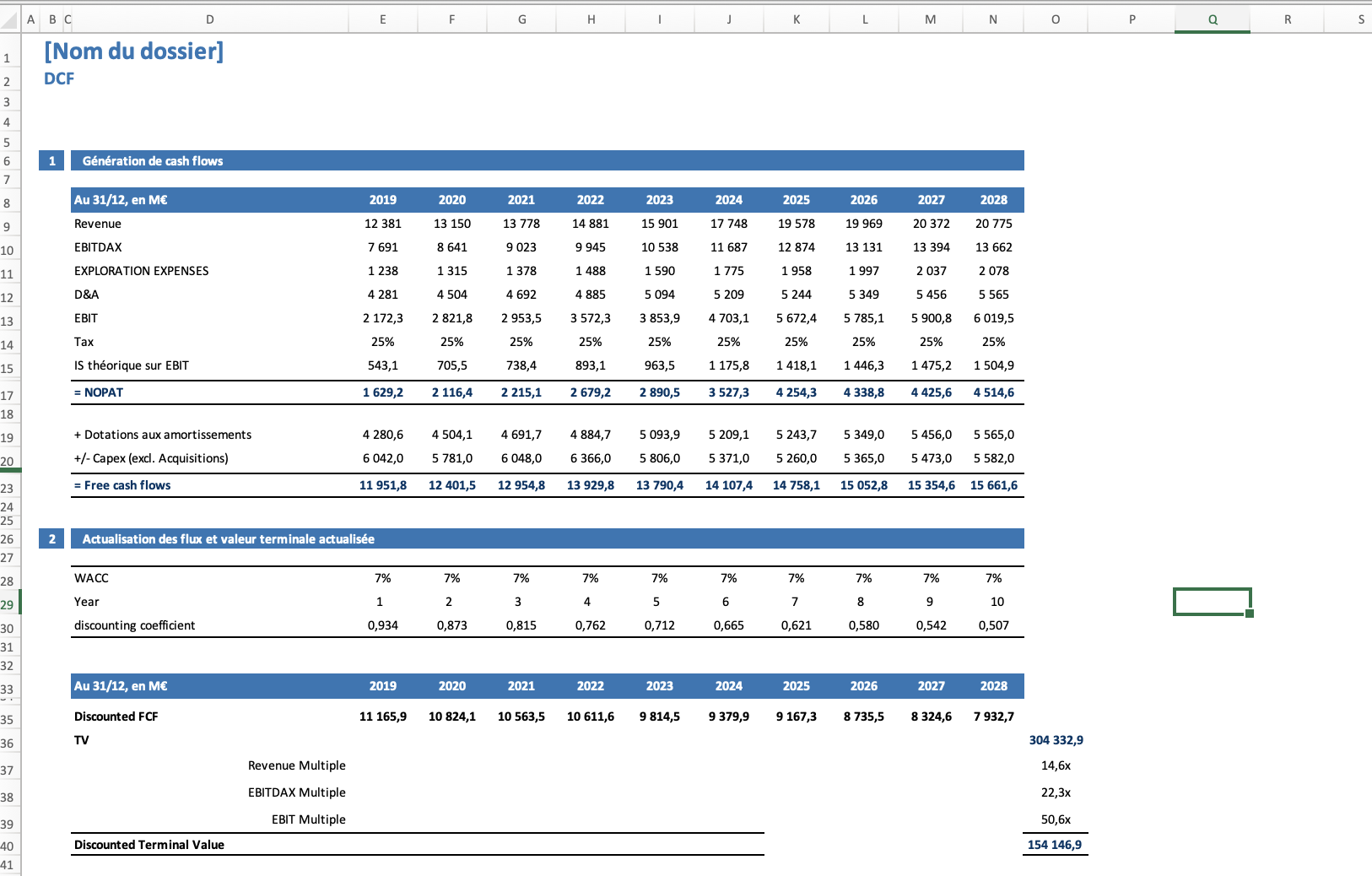

4. a. Please compute the standalone value of Anadarko using DCF. Make the following assumptions: (i) net working capital needs are negligible; (ii) exploration expense is 10% of revenues; (iii) the tax rate is 25%; the cost of debt of Anadarko is 4%. How does your DCF estimate compare with the value of $40 billion in Question 3? b. How much are the synergies worth? c. Please value the deal using transaction multiples

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock