Question: Hello Goodbye Ltd. (HG) is a mobile network provider listed in the telecommunication section of the Johannesburg Stock Exchange (JSE). HG is currently planning

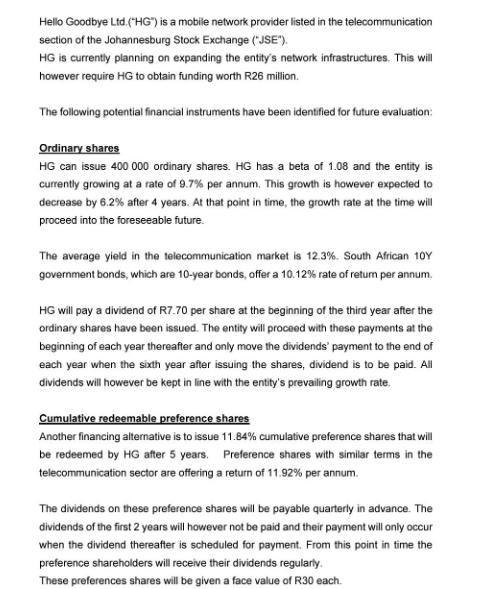

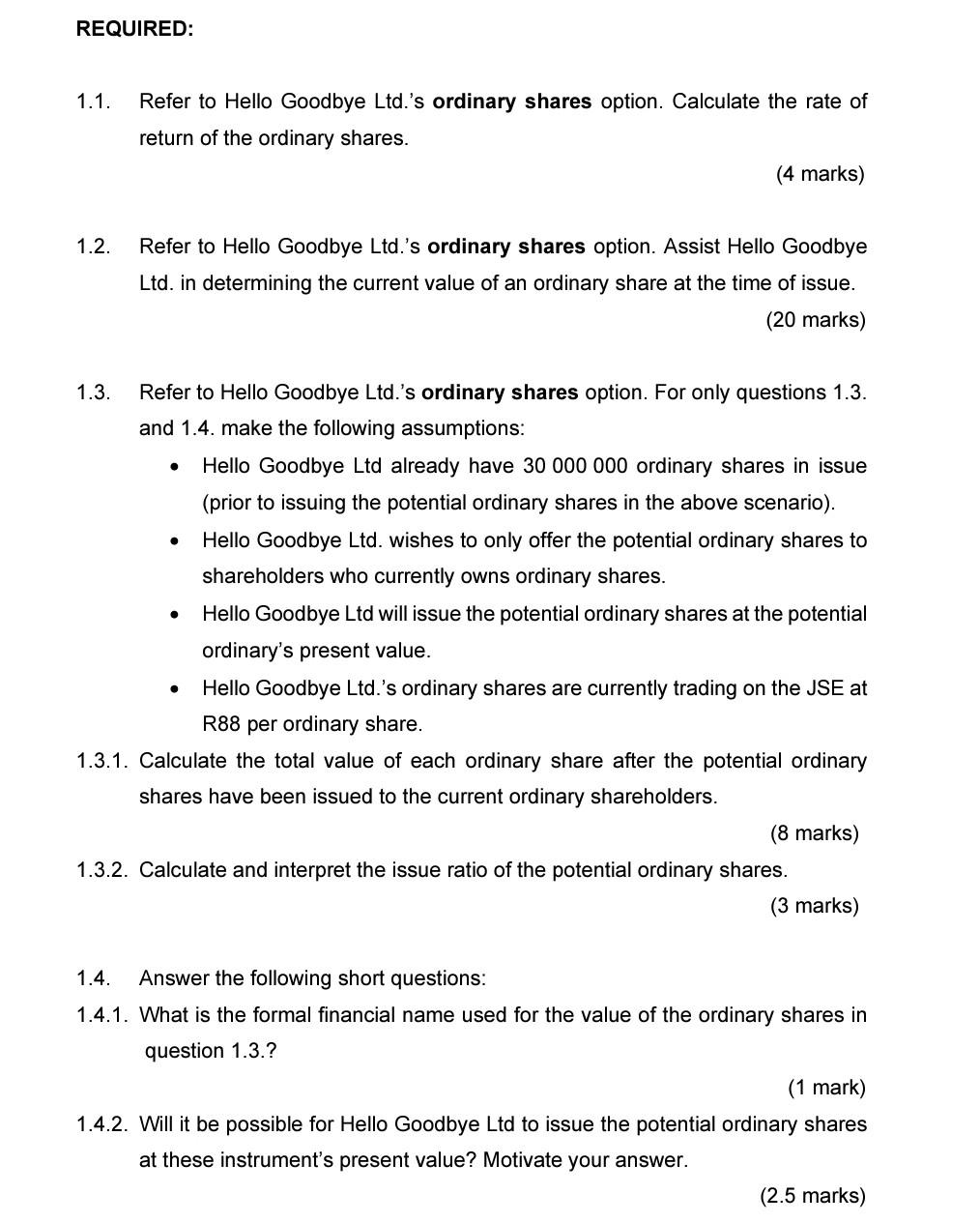

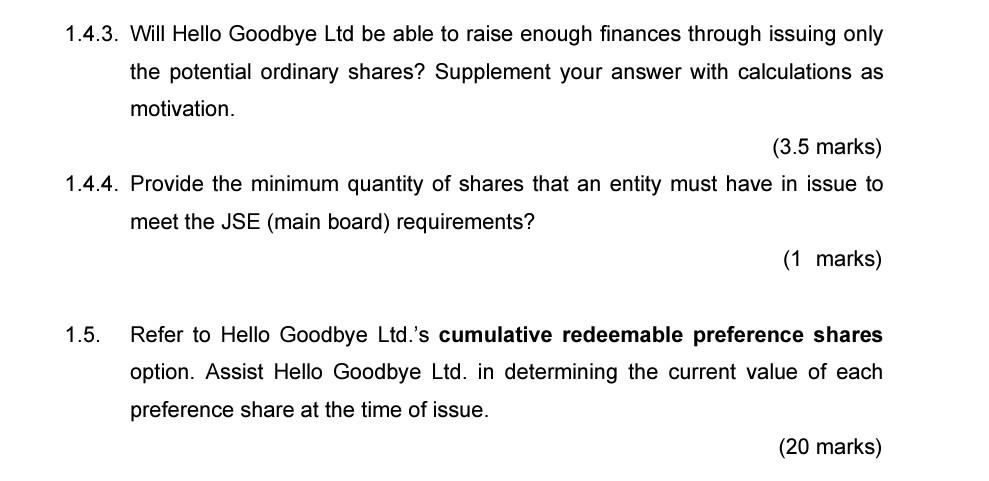

Hello Goodbye Ltd. ("HG") is a mobile network provider listed in the telecommunication section of the Johannesburg Stock Exchange ("JSE"). HG is currently planning on expanding the entity's network infrastructures. This will however require HG to obtain funding worth R26 million. The following potential financial instruments have been identified for future evaluation: Ordinary shares HG can issue 400 000 ordinary shares. HG has a beta of 1.08 and the entity is currently growing at a rate of 9.7% per annum. This growth is however expected to decrease by 6.2% after 4 years. At that point in time, the growth rate at the time will proceed into the foreseeable future. The average yield in the telecommunication market is 12.3%. South African 10Y government bonds, which are 10-year bonds, offer a 10.12% rate of return per annum. HG will pay a dividend of R7.70 per share at the beginning of the third year after the ordinary shares have been issued. The entity will proceed with these payments at the beginning of each year thereafter and only move the dividends' payment to the end of each year when the sixth year after issuing the shares, dividend is to be paid. All dividends will however be kept in line with the entity's prevailing growth rate. Cumulative redeemable preference shares Another financing alternative is to issue 11.84% cumulative preference shares that will be redeemed by HG after 5 years. Preference shares with similar terms in the telecommunication sector are offering a return of 11.92% per annum. The dividends on these preference shares will be payable quarterly in advance. The dividends of the first 2 years will however not be paid and their payment will only occur when the dividend thereafter is scheduled for payment. From this point in time the preference shareholders will receive their dividends regularly. These preferences shares will be given a face value of R30 each. REQUIRED: 1.1. 1.2. 1.3. Refer to Hello Goodbye Ltd.'s ordinary shares option. Calculate the rate of return of the ordinary shares. Refer to Hello Goodbye Ltd.'s ordinary shares option. Assist Hello Goodbye Ltd. in determining the current value of an ordinary share at the time of issue. (20 marks) Refer to Hello Goodbye Ltd.'s ordinary shares option. For only questions 1.3. and 1.4. make the following assumptions: (4 marks) Hello Goodbye Ltd already have 30 000 000 ordinary shares in issue (prior to issuing the potential ordinary shares in the above scenario). Hello Goodbye Ltd. wishes to only offer the potential ordinary shares to shareholders who currently owns ordinary shares. Hello Goodbye Ltd will issue the potential ordinary shares at the potential ordinary's present value. Hello Goodbye Ltd.'s ordinary shares are currently trading on the JSE at R88 per ordinary share. 1.3.1. Calculate the total value of each ordinary share after the potential ordinary shares have been issued to the current ordinary shareholders. (8 marks) 1.3.2. Calculate and interpret the issue ratio of the potential ordinary shares. (3 marks) 1.4. Answer the following short questions: 1.4.1. What is the formal financial name used for the value of the ordinary shares in question 1.3.? (1 mark) 1.4.2. Will it be possible for Hello Goodbye Ltd to issue the potential ordinary shares at these instrument's present value? Motivate your answer. (2.5 marks) 1.4.3. Will Hello Goodbye Ltd be able to raise enough finances through issuing only the potential ordinary shares? Supplement your answer with calculations as motivation. (3.5 marks) 1.4.4. Provide the minimum quantity of shares that an entity must have in issue to meet the JSE (main board) requirements? 1.5. (1 marks) Refer to Hello Goodbye Ltd.'s cumulative redeemable preference shares option. Assist Hello Goodbye Ltd. in determining the current value of each preference share at the time of issue. (20 marks)

Step by Step Solution

3.44 Rating (151 Votes )

There are 3 Steps involved in it

11 Calculate the rate of return of the ordinary shares The rate of return of the ordinary shares can be calculated using the Dividend Discount Model DDM formula considering the growth rate and the req... View full answer

Get step-by-step solutions from verified subject matter experts