Question: Hello, I calculated the deviation in covered interest rate parity between the KRW and the USD from 206 to 2020, but I don't understand the

Hello,

I calculated the deviation in covered interest rate parity between the KRW and the USD from 206 to 2020, but I don't understand the next part of the assignment. The Professor says to do the Durbin Watson test on the deviations, but from what I know, you need to have a linear regression model and some kind of variables to perform the Durbin Watson test, so I am at a loss as to what to do. In addition, in the next question, the Professor wants us to do a linear regression, but I am unsure what variable we are performing a regression on. Any help in interpreting what I am supposed to do next would be much appreciated.

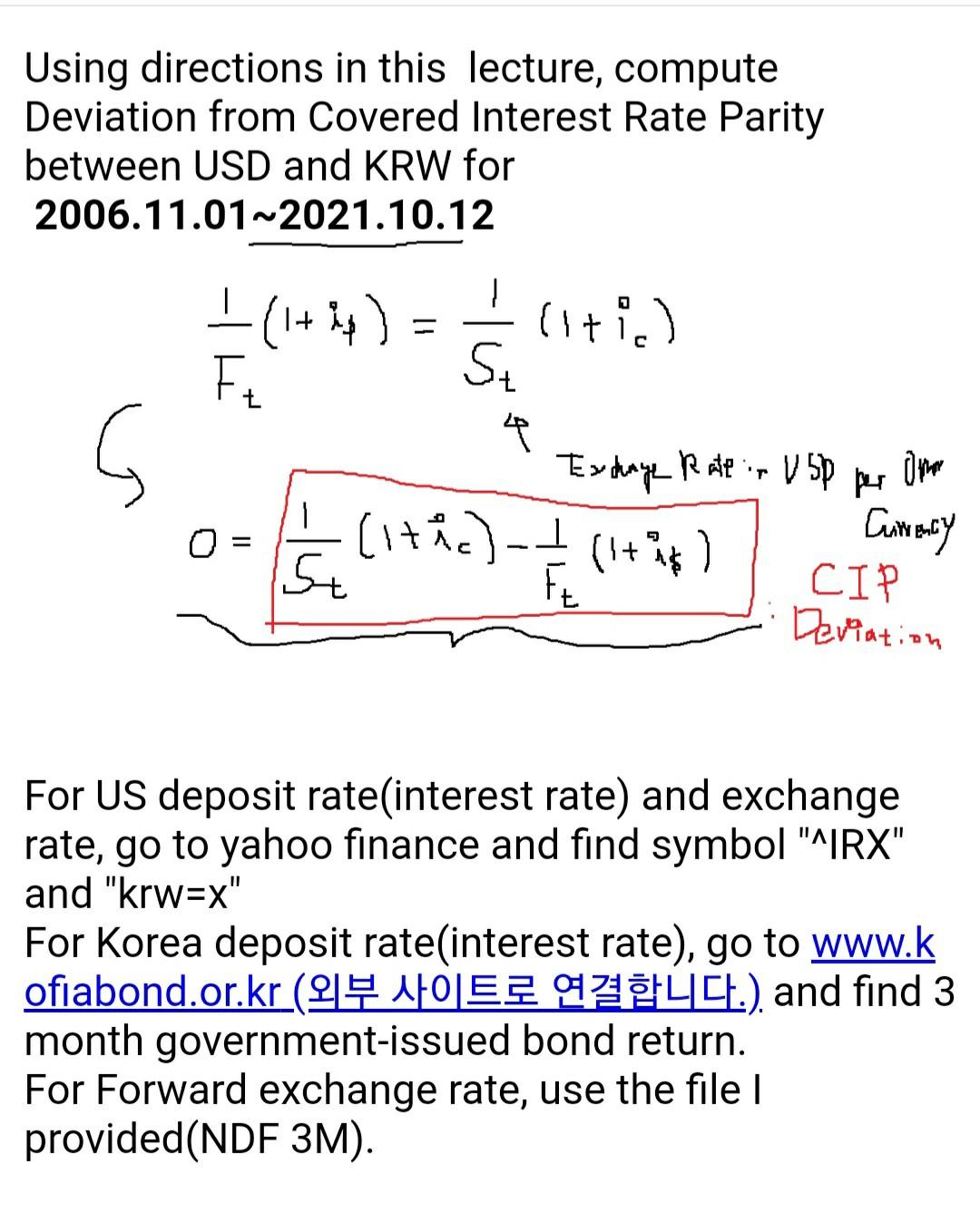

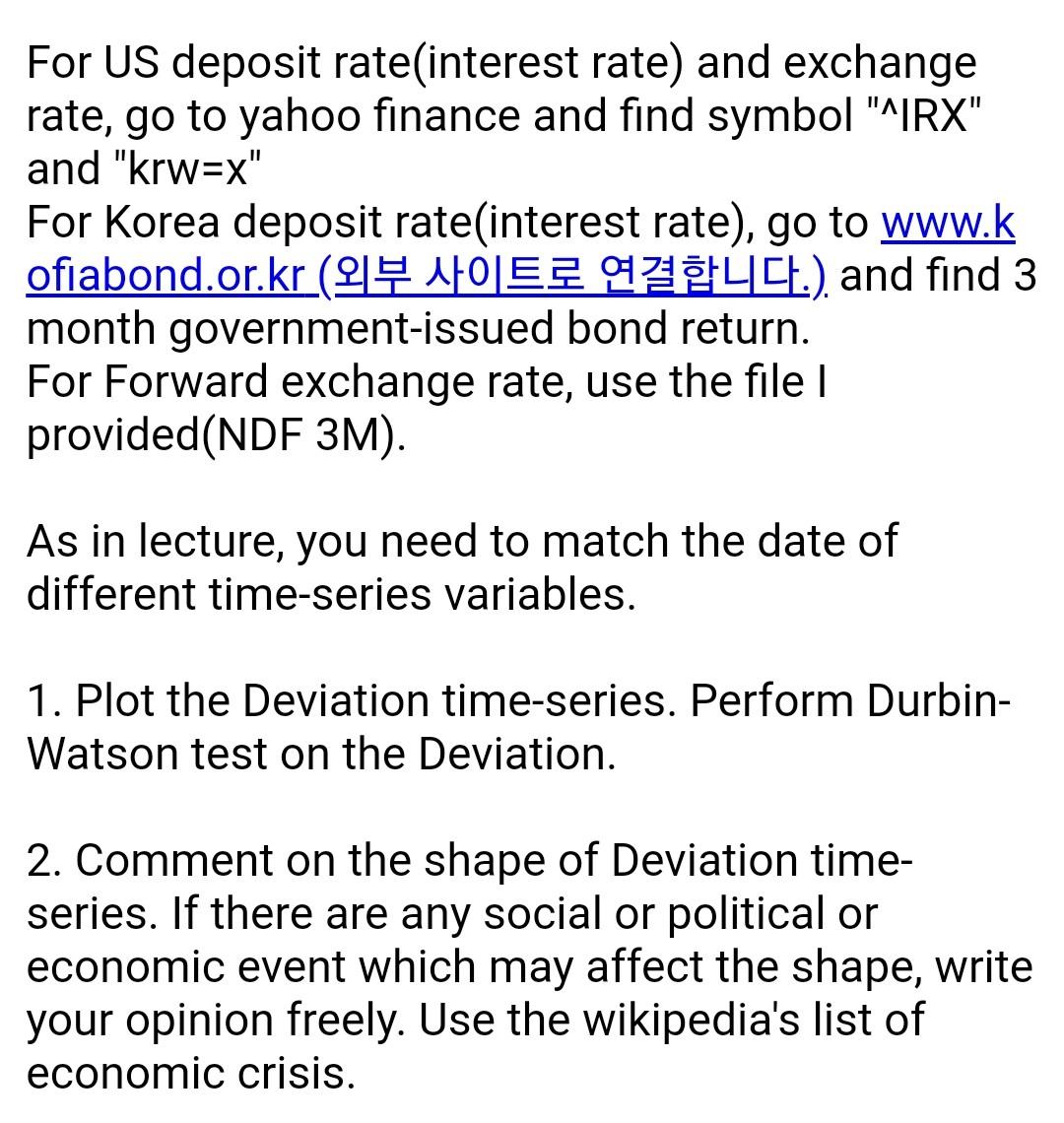

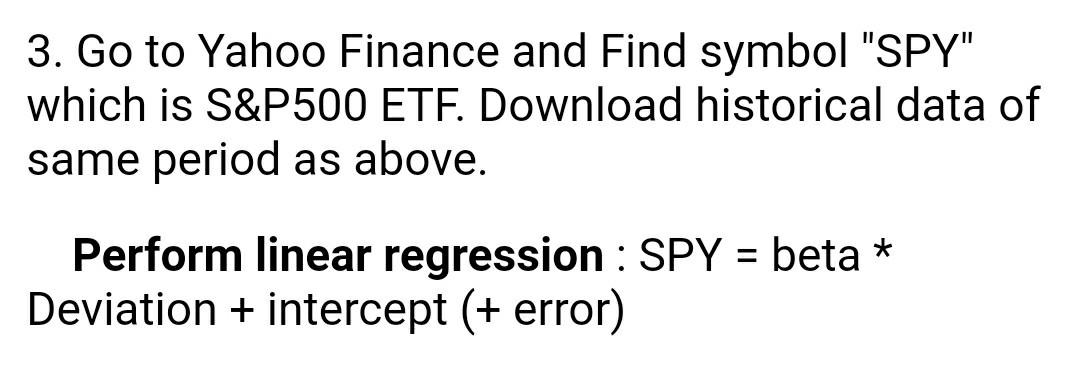

Using directions in this lecture, compute Deviation from Covered Interest Rate Parity between USD and KRW for 2006.11.01~2021.10.12 | (+) = |_{1+ is) El litis) St G Om 1 o (itic) - Exdays Raftin VSP (1+i) FL 16 )-{ Currency CIP Deviation For US deposit rate(interest rate) and exchange rate, go to yahoo finance and find symbol "AIRX" and "krw=x" For Korea deposit rate interest rate), go to www.k ofiabond.or.kr (29 105. 02 LCL) and find 3 month government-issued bond return. For Forward exchange rate, use the file I provided(NDF 3M). For US deposit rate(interest rate) and exchange rate, go to yahoo finance and find symbol "AIRX" and "krw=x" For Korea deposit rate(interest rate), go to www.k ofiabond.or.kr ( 210E9724CL.), and find 3 month government-issued bond return. For Forward exchange rate, use the file I provided(NDF 3M). As in lecture, you need to match the date of different time-series variables. 1. Plot the Deviation time-series. Perform Durbin- Watson test on the Deviation. 2. Comment on the shape of Deviation time- series. If there are any social or political or economic event which may affect the shape, write your opinion freely. Use the wikipedia's list of economic crisis. 3. Go to Yahoo Finance and Find symbol "SPY" which is S&P500 ETF. Download historical data of same period as above. = Perform linear regression : SPY = beta * Deviation + intercept (+ error) Using directions in this lecture, compute Deviation from Covered Interest Rate Parity between USD and KRW for 2006.11.01~2021.10.12 | (+) = |_{1+ is) El litis) St G Om 1 o (itic) - Exdays Raftin VSP (1+i) FL 16 )-{ Currency CIP Deviation For US deposit rate(interest rate) and exchange rate, go to yahoo finance and find symbol "AIRX" and "krw=x" For Korea deposit rate interest rate), go to www.k ofiabond.or.kr (29 105. 02 LCL) and find 3 month government-issued bond return. For Forward exchange rate, use the file I provided(NDF 3M). For US deposit rate(interest rate) and exchange rate, go to yahoo finance and find symbol "AIRX" and "krw=x" For Korea deposit rate(interest rate), go to www.k ofiabond.or.kr ( 210E9724CL.), and find 3 month government-issued bond return. For Forward exchange rate, use the file I provided(NDF 3M). As in lecture, you need to match the date of different time-series variables. 1. Plot the Deviation time-series. Perform Durbin- Watson test on the Deviation. 2. Comment on the shape of Deviation time- series. If there are any social or political or economic event which may affect the shape, write your opinion freely. Use the wikipedia's list of economic crisis. 3. Go to Yahoo Finance and Find symbol "SPY" which is S&P500 ETF. Download historical data of same period as above. = Perform linear regression : SPY = beta * Deviation + intercept (+ error)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts