Question: Hello I have questions about the Stochastic Calculus. This topic is about the Stochastic deferential equation. STOCHASTIC DIFFERENTIAL EQUATIONS 1. Solve the following SDE: dXt

Hello I have questions about the Stochastic Calculus. This topic is about the Stochastic deferential equation.

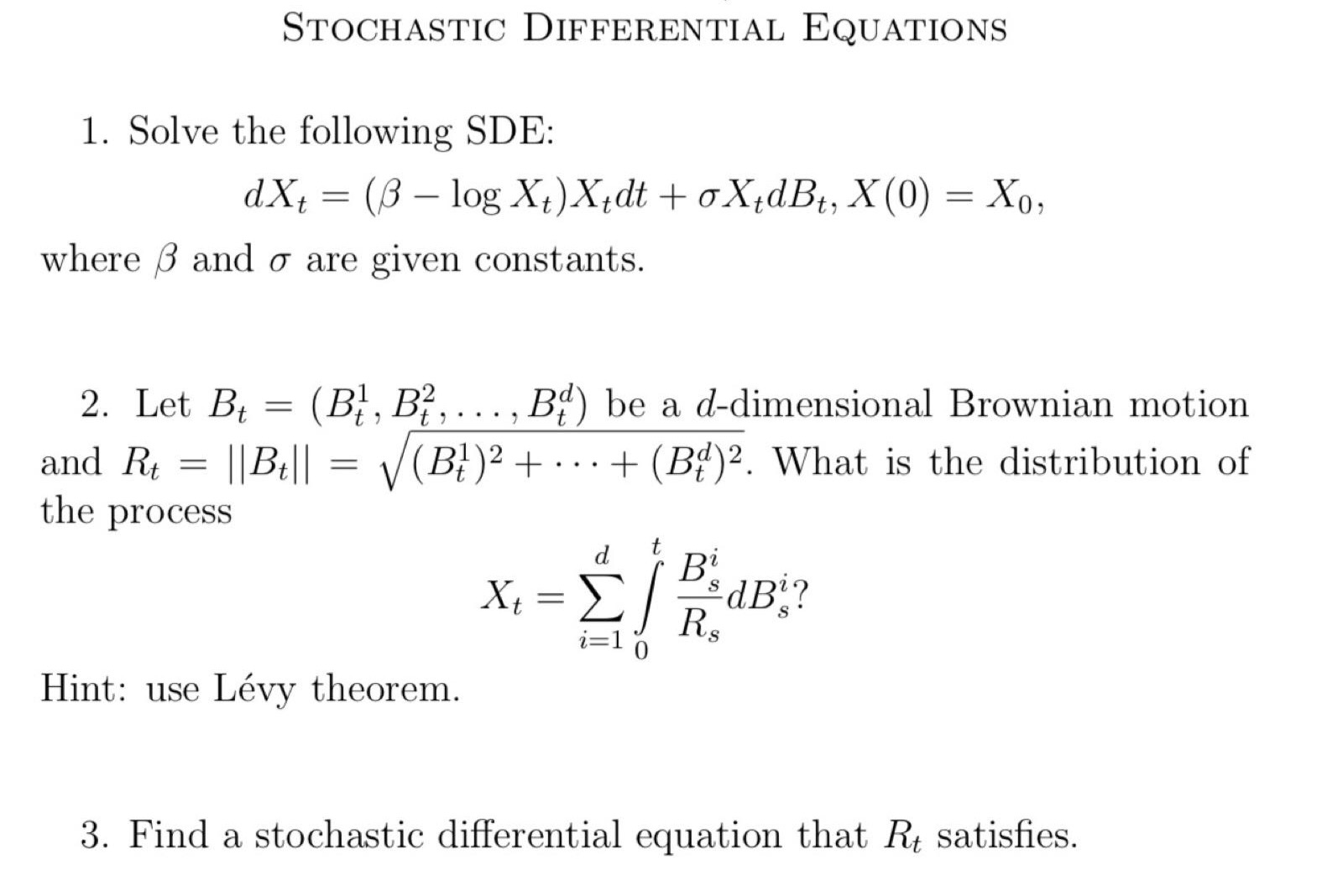

STOCHASTIC DIFFERENTIAL EQUATIONS 1. Solve the following SDE: dXt = (/3 10g Xt)Xtdt + O'XtdBt, X(0) : X0, Where 6 and 0 are given constants. 2. Let Bt = (8151,83, . . . ,Bf) be a ddimensional Brownian motion and Rt 2 ||Bt|| 2 (B3)2 + - ' - + (Bf)? What is the distribution of the process d t big/B _:dBi-? =10 Hint: use Lvy theorem. 3. Find a stochastic differential equation that Rt satises

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock